GaWC Research Bulletin 414 |

|

|

|

This Research Bulletin has been published in The Geographical Journal, 179 (3), (2013), 198-210. Please refer to the published version when quoting the paper

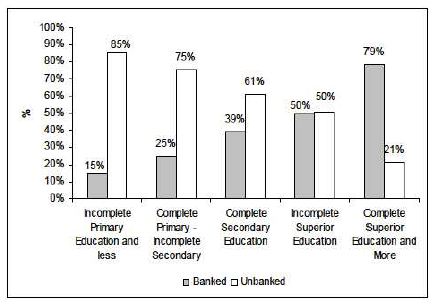

Introduction: Latin American Financial GeographiesOn the eve of the financial crisis in 2007 the authors were involved in a regional consultancy study of the provision of financial services to the urban poor in seven Latin American cities. The research was undertaken over an 18-month period and brought together partners from Argentina, Chile, Brazil, Venezuela, Colombia, Mexico and the UK. This paper draws upon that research but is a broader reflection on ‘bancarización’ in Latin America (a loose term used to denote banking the unbanked) and how low-income families are excluded from (and can be linked into) fuller participation in the formal financial services sector. Despite important disavowals of O’Brien’s (1992) proclamation of the end of the significance of geography for financial processes (see, for example, Martin 1994, Leyshon, 1998 and Dymski, 2009), there remains a lack of significant exploration by geographers of the geographies of finance outside of the major centres of global finance. There have been few studies, for example, of how the current global financial crisis is affecting Latin America, even if only via comparisons to the debt crisis of the 1980s (Pineda et al, 2009). In fact, leaving aside the research conducted on that earlier period (to which we return briefly below), few geographers with specialist interests in financial services, financial globalization or the geography of money have evidenced much interest in Latin America or the countries of the Global South more generally. The irony is that, the (so far) more positive experience of Latin American economies during the current global economic crisis may have important lessons for our longer-term understanding of the geography of global financial markets, financial crises and the differentiated impacts of financial globalization (Herschberg, 2011; Jara et al, 2009; Rojas-Suarez, 2010). At the same time, it is critical to understand how the continuing economic good fortune enjoyed by countries such as Brazil and Chile may be directly affected by their ability to bring about substantial structural and social change where the poor and unbanked are concerned, to take strong steps to link them into, and allow them to benefit from, the formal economy. In part, the scale at which regional financial services geographies have been set can be explained by the way in which Latin America’s financial sector became the focus of intensive study across a range of disciplines in the 1980s (see, for example, Dietz, 1989; Griffith-Jones and Sunkel, 1986; Roddick, 1988; Stallings, 1987), as the epicentre of a series of global systemic crises. The crisis of that period evolved out of the threatened debt defaults of major Latin American economies and their interaction with the economies of the global north, and therefore the quantity of studies of the region’s financial sector with that transnational macro-focus at the time and subsequently is hardly surprising. Research on the nature of the Latin American debt crisis and international responses to it (Thrift and Leyshon, 1988; Corbridge, 1988) at that time acted as a catalyst towards the emergence of a broader interest in money and finance by geographers, as well as the evolution of a broader geographical literature on financial globalization and global geographies of money (Christophers, 2009; Clark and Wojcik, 2007; Corbridge et al, 1994; Dymski, 2009; Leyshon, 1995; Leyshon and Thrift, 1996; Martin, 1999). Critically, this set the macro-scale at which ‘knowing’ Latin American financial services came to be framed. Interestingly, this way of ‘knowing’ financial services is reinforced by the nomenclature used to describe and de-couple successive crises by locating them at a particular regional scale. The increasing number and intensity of crises towards the end of the 20th and in the first decade of the 21st century has continued to be described in this selective linguistics of labelling – hence the Latin America Debt crisis, the Tequila crisis, the East Asian crisis, the Russian Crisis and the current iteration of the ongoing global economic crisis referred to as the Eurozone crisis (see Kelly 2001 on this in relation to the Asian financial crisis). In the landscape formed by post-2007 events, however, an understanding of both local causation and global connectivity as well as a new mindset and language of the geography of these crises is vital. This ‘absence of the local’ has been picked up elsewhere (Lee et al, 2009) in reflections on the remit of financial geography as a result of the current crisis, in the need to pay increased attention to: “particularly the social, network and territorial embeddedness of agents” and finally to more effectively recognise “the situatedness of knowledge” (Lee et al, 2009: 724 - 736). This situatedness of knowledge has become increasingly important in the global lacunae of formal financial services organization - in Sub-Sahel Africa, for instance, where mobile phone networks fill in the vacuum of formal rural banking provision with new electronic topographies; or where zones of exclusion from financial services coverage provide strange new landscapes of heterogeneous services in Latin America. There are of course exceptions to our general observations regarding the lack of attention paid by geographers to the geographies of finance outside of the major centres of global finance. Amongst these in relation to Latin America are: Christof Parnreiter’s work on the role of Latin American cities in the network of global cities (Parnreiter, 2010), Biles’ (2005) studies on the impacts of the globalization of financial services within individual Latin American economies, work on offshore banking in the region and its dynamics (Warf, 2002) and analyses connecting capital account liberalization, economic performance and social crises (Biles, 2010). Some general works on financial globalization and ‘the developing world’ also refer to Latin America or to individual countries (Coleman, 2002; Sarre, 2007; van Hulten and Webber, 2010; Wojcik and Burger, 2010). This work though still tends to act through a focus on macro-processes rather than detailed considerations of the dynamics and differential impacts for individuals, households and communities (with the exception of James Biles’ research on Mexico). The limited body of work on Latin American financial geographies has tended to look at the formal financial sector and its impacts on the ‘formal’ economy, rather than deconstructing what is implied by financial markets and institutions and how they interact with the urban poor and broader, diverse national socio-economic policy contexts. A vast mass of economic activity in the region has, therefore, been left out of such analyses, not least because of the difficulty of mapping the ‘informal’ economy and corresponding informal financial services. A much more detailed and grounded analysis of those interactions in different settings is needed. As Lee et al assert, “(W)hile much financial geography has traditionally been focused on financial centres and institutions and, in essence, the ‘supply’ architectures of financial geographies…… this latest bout of financialisation is interesting in part because it surely forces analytical attention to some different – and much more difficult to research – financialised sites and agents, including a wide range of intermediaries, firm managers, households and consumers” (2009:735). Whilst the financial geographies literature has tended to pass over financial localism, by way of contrast, work focusing on social conditions in Latin America with a ‘development’ geography orientation has shown little interest in how the dynamics of financial globalization has affected the poor. The body of critical geographical work on globalization and neoliberalism in Latin America that incorporates discussion of financial globalization has tended to be relatively general, with relationships between the massive transformations in global financial markets and the more marginalized sectors of Latin American societies assumed, rather than explored in detail. Social geographies of poverty frequently include considerations of access to credit and other financial services but few connect these analyses to discussions of changes wrought in the structure of financial markets, although some recent work has begun to reflect on the complexities of the relationship between financial globalization, financial inclusion/exclusion and poverty in Northern contexts (Bernard et al, 2008; Dymski, 2009; Fuller and Mellor, 2008)2. In the discussion which follows, therefore, we set out a series of reflections on what a more nuanced Latin American financial geography connecting the financial lives of the poor to changes in regional financial services architecture might look like. ‘Bancarizacion’ and the demand for financial servicesThe low levels of access to formal financial services reported across Latin America, indeed across the global south, have been a constant in research over the last three decades (although the difficulty in effectively measuring access continues to constitute a major obstacle for research, in this field). In many countries, despite advances in banking technology and lending practices, levels of ‘bancarizacion’ remain low. In 2009 as many as 62% of all adults in Asia, Africa, Latin America and the Middle East had no access to banking services, albeit with big regional differences - as much as 80% of the population of Sub-Sahel Africa are ‘unbanked,’ whilst 51% are ‘banked’ in Latin America (CAF, 2010) the figure for OECD countries is only 8% (Chaia et al, 2009). Even in regions like Latin America with a higher average, individual country figures vary; in 2005 the World Bank reported that in Mexico, 70% of the population over the age of 18 had no access to basic financial services and by 2010 in Peru and Bolivia only 38.7% and 34.9% of the population respectively had access (CAF, 2010). Continuing restriction in access to financial services must also be seen in the context of economic growth in the region. After 2002 Latin America enjoyed strong growth in employment which lasted until the third quarter of 2008 when the effects of the global economic crisis began to be felt in the region (ILO, 2008). Levels of poverty decreased from 44.4% of the region’s population in 1992, to 41.5% in 2003 and 29.6% in 20093 and urban unemployment in particular showed a marked decline – between 2002 and 2010 the regional rate of open urban unemployment dropped from 11.2% to 7.3% (ECLAC, 2011: 65). The decline in poverty was matched by a sharp decrease in income inequality between 2002 and 2010 which eliminated a substantial part of the increase in inequality that had occurred during the liberalization period from the late 1970s to the end of the 1990s (Cornia, 2012). Despite this strong economic growth accompanied by declines in unemployment, poverty and inequality, however, access to formal financial services remained restricted. As a caveat, figures for levels of access to financial services in individual countries and city regions have still tended to vary over time, depending particularly on how they are measured. To give some idea of regional variations Table One gives comparative formal financial service access figures for a selection of Latin American countries to 2010. Table 1: An Estimate of the Percentage of Adult Population with Access to Financial Services Barriers to financial services access – ‘push and ‘pull’ factorsA range of explanations for low financial services participation rates have been put forward by researchers and institutions, with a great degree of variation depending on what exactly is being measured; some of the indicators seem to be only indirectly related to income and levels of poverty. In terms of ownership of deposit accounts and loan penetration, Kendall et al (2010: 4) in a survey of financial regulators in 139 countries found that “the best predictors…. are measures of the development of physical infrastructure including electricity consumption and phone line density.” Using econometric analysis however is ineffective at picking up other more subtle socio-cultural barriers to accessing formal financial services. In Latin America, other explanations have included attributes of the banking system itself (ineffective pricing policies involving maintenance costs, commissions, collateral, guarantees and interest rates), the lack of distribution networks and appropriate risk assessment policies (for example, appropriate kinds of insurance for low-income households/micro-businesses) and more generally poor regulatory environments and public distrust of the formal banking sector (see Taylor et al, 2008). These attributes are nonetheless a foreground to a far more complex hinterland of technical and non-technical barriers to access revolving around the incidence of poverty and income inequality. Recognition of this has already begun to fuel research in economics; the proposal by Beck and de la Torre (2006) of an Access Possibilities Frontier which includes voluntary self-exclusion is one example of this - a range of research in other disciplines from Latin America furthermore has begun to investigate individual national environments. For one example of a more specific causal mechanism, research conducted in Colombia indicates that an important socio-cultural barrier determining whether an individual either has or is able seek access to financial services is the level of education possessed by that individual (see Figure One). This factor, what Lopez and Perry (2008: 14) refer to as “low educational mobility,” has also been identified as an important factor in determining high income inequality. In Venezuela meanwhile Ackerman (2007) observes that there is a close, inverse relationship between levels of inflation and levels of bancarizacion, because of the vulnerability of the poor in particular to relatively high levels of inflation. Figure 1: Correlation between educational level and the use of formal financial services in Bogotá, Colombia Access to financial services is also gendered – a range of studies indicate that men are more likely to access financial services from the formal financial sector than women. Tejerina and Westley (2007) indicate that men are nearly five times more likely to access the formal financial services sector than women - a phenomenon apparently unchanged by the fact that according to ILO estimates (2008), of the substantial employment growth experienced by Latin America between 1991 and 2007, over 50% was female employment. There are obviously complex and interconnected factors at work in producing regionally low levels of ‘bancarizacion’ and the complexities of access within individual countries which go beyond dominant discussions of the attributes of the financial services sector itself – this paper argues in particular that the agency of the individual has been left out of previous meta-analyses, particularly those of economists. An effective understanding of financial services access requires a combined approach, including investigating the attributes of the financial sector within individual countries, how national systems connect to global and regional financial circuits and, of critical importance, the interplay of formal/informal financial systems in the everyday lives of communities, households and individuals. The ability to access financial services can be seen as a signifier of the degree of citizenship itself possessed by each individual; the socio-cultural environment must be analysed therefore in combination with the vital element of individual choice. Economic research indicates that income inequality, levels of poverty and the degree of bancarizacion are connected (Beck et al, 2009), but we propose that it is the socio-cultural factors that ensure that this connectivity does not always occur in the same ways or in the most obvious ways. Factors that have previously been read as phenomena affected by economic circularity (and as therefore amenable to technical fixes) are conditioned by social phenomena affected by and which affect a host of other complex socio-economic factors. These socio-economic factors are contingent on other micro- and macro-economic causal mechanisms which are themselves not well-understood; a range of research suggests for instance that higher inequality leads to higher poverty levels (see Prowse, 2007 and Wagle 2010 for discussion of this complex issue) and also that higher inequality itself acts as a barrier to reducing poverty - countries with higher income inequality apparently grow less and at a slower rate (Lopez and Perry, 2008: 2). At the same time there is another body of research indicating a strong positive correlation between the growth of financial intermediation and development, measured by factors such as growth in GDP, per capita income, investment and aggregate productivity (King and Levine, 1993; Beck et al, 2000). Much of the literature on financial services provision in Latin America, then, in concentrating on orthodox micro- and macro-economic factors and the behaviour and development of the financial services sector itself ignores the way in which the differential spread of access to various types of financial services amongst the poor derives from the complex lives of low-income households and micro-businesses. There has been little work done (for instance) on the preference for cash as a way of avoiding the frequently onerous national tax systems of the region, perhaps another reason why electronic payment systems not linked to bank accounts are increasingly popular in the region, and why substantial quantities of micro-businesses lack basic accounting systems and registered accounts (Fontes and Cossio, 2007). Pronounced income-inequality and varying national taxation structures and mechanisms have socio-cultural roots and implications as well as economic ones, a phenomenological synthesis that the discipline of economics in particular ignores. These themes emerged strongly from the project we carried out on access to financial services within the seven Latin American cities described in the introduction (an overview of findings can be found in Taylor et al, 2008); combined with a further more recent review of materials, this analysis produced a table of ‘push’ and ‘pull’ factors affecting levels of bancarización. ‘Push’ factors are institutional factors located in the bank, legal system, culture or government which constitute a barrier to the unbanked individual accessing financial services, whilst ‘pull’ factors are factors determined by the agency of the individual, located in the perception/experience of the unbanked in terms of financial services access, systemic, governmental, institutional and those personal to the unbanked (see Table Two). Table 2: Push and pull factors affecting access to financial services

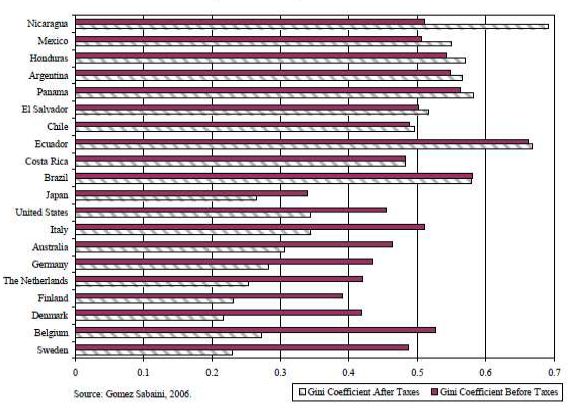

It should first be emphasized that occasionally the divide between ‘push’ and ‘pull’ factors is a spurious one – racial/ethnic/caste prejudices, for instance, can be both practiced by a financial services institution and inform the agency of the individual. Nevertheless, in exploring access to finance in this way the agency of the unbanked can be brought back into the picture, in particular the consideration that the decision to remain unbanked can often be a logical one in a hostile governmental, institutional and social environment. It should also be noted that the list thus presented is intended as a stimulus to debate and is not intended to be exhaustive. Plainly the list of factors will vary according to differing national financial services environments, although there is likely to be a core set of factors that is universally applicable. The reasons for the unbanked to be unable to/unwilling to access each individual type of financial service will also vary – if the most desired facility was a savings account (for example Solo, 2011), the reasons for being unable/unwilling to access such a facility are obviously quite distinct from the reasons for being unable/unwilling to access, say, consumer credit. Above all, the range of factors identified in Table two accentuates the substantial methodological challenges involved in analyses of the unbanked. As regards the household, in Latin America substantial numbers are complex micro-business worlds by themselves, overwhelmingly in the low-income sector. Using sectoral definitions, product typologies, descriptions and analyses suited to a developed market economy as a way of looking at the dynamics of the financial needs of the poor is therefore not only inadequate it is misleading. The micro-business sector: households, instability and taxationBearing in mind the previous point about the complex inter-meshing of household and ‘business’ finance, we now turn the dynamics of the small business (SME) sector. The micro, small and medium business sector in Latin America is by far the largest business sector in terms of employment in the region4; understanding the complex mesh of networks in which the dual micro-business/household entity exists and operates is vital to understanding deficits in financial services provision. This is particularly critical in the light of the ratio of what are referred to as the formal and informal economies of the region (Biles, 2008). For the majority of the regional population, the informal economy is the majority economy (Pozuelo-Monfort, 2009) and what is referred to as the formal economy is peripheral to their daily lives – nevertheless, the effects of the formal economy on their well-being can be dramatic. Regionally Latin America experienced a substantial growth in informal sector employment and a corresponding deterioration in the quality of employment overall between 1990-2002, followed by a sudden boom in formal sector employment created by the demand for commodities on world markets in 2003-2008, for instance (Ocampo and Vallejo, 2012). The informal economy and the labour created within it is therefore vulnerable to trends within the formal economy through transmission mechanisms over which it has no control, such as import/export prices, interest rate and inflation fluctuations, banking failures, trade agreements and so forth, but the important support role that the informal economy plays for the formal economy brings it little recognition in return - for the majority of citizens of Latin America alive now and yet to be born, however, the informal economy and the micro-business is all they will know. Despite its marginalization, the ILO calculates that the informal economy in Latin America accounted for as much as 58.6% of all employment in five countries surveyed in 2007 (ILO, 2009) and a range of literature (see Thomas, 2002 and Valenzuela, 2005 for examples) has pointed out the growing informalization of the Latin American economy and its increasing openness to economic intervention from outside the region from the late 1980s onwards. The majority of micro- and small businesses in the region, however, despite the supposed benefits of financial sector liberalization remain unable to access the kinds of financial services that they need, especially in terms of business credit and loans – this despite the empirical research indicating the importance of the close link between SME development and economic growth (Ardic et al, 2011). In essence, the micro-/small business sector, despite its massive importance to the economic well-being of so many families, operates under precarious conditions, continuing to be dependent on the same types of credit used by households that are for the most part indistinguishable from the businesses they host (Taylor et al, 2008). The importance of the MSME (Micro, Small and Medium Enterprise) sector in Latin America stands in stark contrast to the range, availability and quantity of accessible credits, loans and accounts - part of the reason for this restricted access comes from the location of the vast majority of these businesses in the informal economy, but another body of evidence suggests that the same foreign bank ownership favoured by IFI liberalization and privatization initiatives is correlated with decreased lending to SMEs (Clarke et al, 2005), a phenomenon discussed in more detail in the following section. The socio-economic consequences of failing to link the micro and small businesses of the informal sector to adequate financial services are enormous. According to the Inter-American Development Bank, in 2006 nearly 92% of businesses, 76% of rural properties and 65% of the dwellings in 12 Latin American countries studied were in the informal or “extralegal” economy (IADB, 2006). These assets and businesses in the informal economy were estimated to have had a net worth of more than $1.2 trillion, resources referred to by the IADB as “dead capital.”5 Add to this the detrimental effects of lack of coverage more generally to households and SMEs alike to the local economy and the resultant ‘access inertia’ is substantial – to mere lack of access can be added the costs of travel for those with access where coverage is inadequate, transactional costs implied in using distant formal access/informal substitutes, reduced ability to purchase locally and lost working hours in pursuit of informal/remote finance (Diniz et al, 2011: 7). The concept of ‘dead capital’ is of course problematic (not to mention the accuracy of such statistics and how they are produced) - it runs parallel to a lengthy literature on the informal economy that began with work such as Hart’s innovative (1971) piece6. What is inaccurately described as ‘dead’ is in fact far from it, it is vivid and alive and supports the vast majority of the world’s population; the term itself represents in many ways a neoliberalized rejection of the socio-economic realities of the lived environment of the majority of the world’s population. It implies that all capital, businesses, money flows, exchanges of goods and services that are not located and active in the formal economy are effectively lifeless, awaiting the ‘prince’s kiss’ of linkage into the ‘proper’ formal economy. Such concerns however do not permit us to reject either the concept, or the seriousness with which the ILD, the IADB, the ILO and the World Bank take the idea, out of hand. What these estimates and this concept do (and why we must therefore treat them with caution) is to construct an official representation of hitherto statistically ‘invisibilized’ life support processes in a way that invites ‘acceptable’ discussion and critique. Another way of visualizing and working with the informal, unbanked economy in an acceptable fashion has been the rapid development of the conceptual framework of microfinance7, which in its more orthodox throes envisages the poor as microentrpreneurs who lack access to appropriate financial services to develop. Part of the gap between formal sector financial services supply and household and SME demand is increasingly being filled by microfinance lending institutions. According to the IADB microfinance clients numbered over 8 million in 2007, up from under 2 million in 2001, at which time it was argued that “the potential demand is immense and still largely unsatisfied” (IADB, 2008). By 2011 the number of clients had grown to 12.5 million (IADB, 2011), up 2 million on the 2010 figure which had experienced a dip during the onset of the global economic crisis. Correlating these figures with the varied national figures for the unbanked in Latin America and the growth in the economically active population (by 2050 the Latin American population is projected to stabilize at around 800 million people, overwhelmingly young and 75-80% urban: World Bank, 2011) still leaves a substantial unfulfilled potential. The alternatives to microfinance are self-organized credit unions and a wide variety of forms of unofficial/illegal credit; the inability of the formal financial services industry and the microfinance sector to meet the needs of small businesses and marginalized households therefore remains a major impediment to development in the region. The CAF survey of urban Latin American households (2010) serves to further underline the unmet demand; 63% of the households surveyed had savings of some kind, but less than 40% had them in any kind of a formal institution - over 80% of the households surveyed indicated using alternative, informal instruments. As well as issues of access, use of formal financial services by low-income groups has to be seen in the context of regressive national tax systems. Tax burdens across the region vary from about 10% of GDP in the more resource-rich countries like Mexico and Venezuela to upwards of 36% of GDP in Brazil (Alier and Clements, 2007); the problem is not so much the actual tax burden, however, as the incidence. As Gomez Sabaini (2006) points out, a heavy reliance on indirect taxation and in particular payroll systems in most Latin American economies means that the incidence of taxation falls disproportionately on the lower-income sectors of the population and has a negative effect on resource allocation and regional competitiveness. Looking at a comparison of the change in Gini coefficients before and after taxes are added for a range of Latin American and OECD countries is instructive (see Figure Two). Figure 2: Impact of the Tax System on Income Distribution

Problems associated with tax systems are not restricted to those related to indirect taxes and formal waged labour, however. Rojas-Suarez (2007) asserts that taxes on financial transactions have a disproportionate effect on low-income households and their accompanying micro-businesses because they are likely to be involved in multiple small transactions on a daily basis. In Latin America there are, as a consequence, a variety of reasons for being cautious about accessing financial services - the need for accounts, credit and loans may have to be balanced by the need to maintain as low an ‘official profile’ as possible. The low-income household/micro-business operates in a hostile financial services environment; the caution required to negotiate the tax system is also duplicated by the caution required in negotiating the formal financial services system. There have been recurrent, substantial losses to savers and investors over the last three decades as a result of regional financial/banking crises, for instance in Nicaragua where, between 1990 and 2002, eleven Nicaraguan banks went bankrupt (Brown and Cloke, 2005; Rocha et al 2011). The effects of foreign control of the Latin American financial services sectorUnder the urging of the International Financial Institutions (IFIs), the onset of liberalization in Latin America led to a substantial penetration of regional economies by transnational concerns, particularly in the agriculture, retail, mineral and hydrocarbon sectors as well as financial services (see Bebbington, 2009; Wilkinson, 2009 and Sagebien et al, 2008). Corporations such as Cargill, Citibank, HSBC, BBVA, Telefonica, Repsol and Banco Santander form a complex mesh of control mechanisms through which commodity exports and financial services are run to serve the operations of financial corporations outside the region (Phillips, 2009). To facilitate this, the formal financial service sector has been developed structurally to serve the requirements of local elite allies. Regionally, penetration and ownership by foreign financial services has been substantial – in Mexico (for instance) between the ‘Tequila Crisis’ of 1995 and 2001, foreign ownership of the banking sector increased from 2% to almost 82%. Research on the implications of this process in Latin America indicates that take-over by foreign owners is frequently followed by changes in lending and operating practices, such as a decline in the numbers of deposit and loan accounts and an increased focus of operations on wealthier urban areas (Beck and Peria, 2008). Research from elsewhere in the world is ambivalent on whether increasing foreign ownership/participation contributes to greater participation and financial systems stability (see a range of views in Detragiache et al, 2008; De Haas and van Lelyveld, 2006; Stiglitz, 2005), but foreign banks in Latin America appear to have been at least more cautious in the evaluation of and management of risk, further affecting access to financial services for low-income sectors in the region. Moguillansky et al (2004) report a variety of behavioural changes following increased foreign bank ownership, including greater caution in the evaluation and management of risk and a concomitant caution when extending credit. More recent work from Mexico (Beck and Peria, 2010) indicates a persistent decline in bank outreach over time, particularly in terms of a decline in deposit and loan accounts; takeovers and acquisitions in that country also came accompanied by a distinct concentration of bank branches within wealthier, urban zones. Other writers have been more forthright in their condemnation of the overall effects of IFI-mandated financial services liberalization and privatization:

The relationship between foreign ownership of the financial services sector and decreased financial services access does not appear to be strictly linear, however. Beck et al (2003, cited in Rojas, 2007) constructed an indicator of “obstacles to business financing” in which the relationship between concentration of banking and obstacles to business financing is examined; they argue that it is the degree of concentration in the sector that is of most significance, whether that ownership be foreign or not. There is therefore a clear relationship between poor institutional quality and obstacles to financial access; there is also interplay between institutional quality, ownership concentration and the degree of foreign ownership in terms of their relative effects on ease of access to financial services for individuals and businesses alike. The importance of analysing these phenomena, particularly so far as Latin America is concerned, is underlined by the global concentration in the financial services sector and the knock-on effect each crisis/set of crises has had in further exposing the region to foreign take-over and ownership. The way forward: financial services for all?Thirty years ago, the Latin American debt crisis ushered in a profound transformation in the nature of the region’s economies, by the end of the decade long-standing economic development models had been upturned, massive social and political upheavels had occurred and the relationship between the region and global financial markets and institutions dramatically recast. As argued in the introduction to the paper, explorations of these transformations at the time played a major role in instilling an interest in money, finance and power within the economic geography academic community. Unfortunately, whilst that initial interest has fostered an explosion of writing on these themes over the intervening years, precious little of it has been expended in understanding the implications of the dramatic transformations in global financial markets for questions of financial exclusion and marginality in regions of the Global South. This paper has attempted to provide a first step in addressing this gap for the Latin American region. There is, however, an urgent need for further research that teases out in more detail the important differences in the dynamics and impacts of the issues explored in this paper in concrete national (and local) settings, reflecting such issues as: the complex geographies of the interactions between the formal and informal (and illicit) financial sectors, the levels of penetration by global capital and levels of concentration of ownership in national finance sectors, the sharply divergent cultures of financial consumption emerging in different urban and rural settings across the region and the spatially-specific evolution of non-traditional suppliers of finance such as supermarkets, mobile phone companies etc. in specific national contexts. Returning to the general argument advanced in this paper, however, it is clear that Latin America’s economies remain encumbered by a profound disjoint between the needs of the massive low-income households/business economy and access to effective financial services. We have largely explored this in the context of the positive economic growth trajectories of the 1990s and early 2000s. The external environment of course changed profoundly as the first decade of the new century wore on, as a result between 2007 and 2009 regional GDP growth declined by an average of 7.5%, regional unemployment rose from 7.4 to 8.3% and remittances to the major recipient countries, Mexico, Ecuador and Colombia shrank by 15%, 13% and 18% respectively (Oxfam, 2010). Towards the end of 2008, the Institute for International Finance estimated that private capital flows to emerging markets had declined to half their record 2007 level; three quarters of this decline was down to the collapse of commercial bank lending although flows have recovered markedly since, by some 40-50% in 2010-2011 (UN, 2011). A substantial quantity of this recovery however has been due to ‘hot’ money seeking safe havens as a result of market instability in the US and Europe, particularly in national economies such as Brazil and Chile which are beginning to experience inflation as a result. As these unstable and inflationary capital flows dictate regional economic advance or decline, research into the small businesses of the informal sector suggest that the economic potential of below-average-income households is enormous. In just one country, Mexico, the Banco Azteca calculated that 70% of the population has the capacity to use, and requires access to, financial services, whilst a USAID assessment of the potential market for microfinance alone in Mexico (Bourns, 2006) put the figure at between 12 and 40 million people. The informal sector in Latin America represents a vast resource with the potential to completely transform domestic and regional economies, city-regions and intra-regional markets. Elsewhere technological innovations are being directed at the lack of financial services networks, for instance in the rapid spread in Africa of mobile phone networks, not only as a means by which remittances and money transfers may be effected but as conduits for credit applications and small-scale loans (Aker and Mbiti, 2010; Hinson, 2011). In Latin America the most durable barriers are non-technical and socio-cultural, but even the rapid growth of microfinance in the region (Olsen, 2010) is doing relatively little to challenge the inertia of an unwilling and unready formal financial services system dominated by transnationally-linked elite concerns and groupings. This paper has shown the role of a range of different factors in the reproduction of the marginalization that characterizes access to financial services in Latin America within an attempt to present a more holistic picture of the technical and non-technical barriers to transforming the situation. In truth, the defects of the system have been obvious for decades and yet limited access to financial services continues to act as a superstructure for the performance and reproduction of poverty. The increasing concentration and subordination of financial services in the hands of multinationals and regional elites in Latin America makes it difficult to avoid the conclusions of Mohammed Yunus, the founder of the Grameen Bank, in asserting that financial institutions are practising forms of financial apartheid (Yunus, quoted in Sarno, 1998:2). The continuing exclusion of low-income and small business sectors over time suggests that the status quo is not left unchanged out of mere disinterest but because the way that it is structured, operated and maintained as an oligopoly better serves the interests of foreign corporations and their elite allies. As Hernando de Soto suggests regarding the reform of property issues for the poor in Latin America, the formal financial services sector continues in the hands: “of conservative legal establishments uninterested in changing the status quo” (Pozuelo-Monfort, 2009). REFERENCESAckerman B 2007 Caracas and surrounding areas: population, income distribution and purchasing power. Unpublished document. Aker J and Mbiti I 2010 Mobile Phones and Economic Development in Africa The Journal of Economic Perspectives 24 (3) 207-232. Alier M and Clements B 2007 Comments on “Fiscal Policy Reform in Latin America” by Miguel Braun. Paper prepared on behalf of the International Monetary Fund for the Copenhagen Consensus for Latin America and the Caribbean—Consulta de San José, Costa Rica, October 20-25, 2007 (http://idbdocs.iadb.org/wsdocs/getdocument.aspx?docnum=1186210) Accessed 1 October 2011. Ardic O, Mylenko N and Saltane V 2011 Small and Medium Enterprises: A Cross-Country Analysis with a New Data Set World Bank Policy Research Working Paper 5538 Financial and Private Sector Development Consultative Group to Assist the Poor, Washington: World Bank. Bebbington A 2009 Latin America: Contesting extraction, producing geographies Singapore Journal of Tropical Geography 30 7–12. Beck T and De la Torre A 2006 The Basic Analytics of Access to Financial Services World Bank Policy Research Working Paper No. 4026 Washington: World Bank. Beck T, Demirgüç-Kunt A and Honohan P 2009 Access to Financial Services: Measurement, Impact, and Policies World Bank Research Observer 24 (1) Washington: World Bank. Beck T, Levine R and Loayza N 2000 Finance and the Sources of Growth Journal of Financial Economics 58(1-2), 261-300. Beck T and Peria M 2008 Foreign Bank Acquisitions and Outreach: Evidence from Mexico Policy Research Working Paper Development Research Group, The World Bank, Washington DC. Beck T and Peria M 2010 Foreign bank participation and outreach: Evidence from Mexico Journal of Financial Intermediation 19 52–73. Biles J 2005 Globalization of Banking and Local Access to Financial Resources: A Case Study from Southeastern Mexico The Industrial Geographer 2 (2) 159-173. Biles J 2008 Informal Work in Latin America: Competing Perspectives and Recent Debates Geography Compass 3 (1), 214–236. Biles J (2010) Chronicle of a debt foretold: Mexico's FOBAPROA debacle and lessons for the U.S. financial crisis Progress in Development Studies 10 (3) 261–66. Bourns N 2006 Indicadores de un Mercado en transición: Finanzas Populares en Brown E and Cloke J 2005 Neoliberal reform, governance and corruption in Central America: Exploring the Nicaraguan case Political Geography 24 (5) 601-630. Brown E and Cloke J 2007 Shadow Europe: Alternative European Financial Geographies Growth and Change 382 304-327. Brown E and Cloke J 2009 Corporate Responsibility in Higher Education ACME: An International E-Journal for Critical Geographies 8 (3) 474-83. CAF 2010 Encuesta CAF Caracas: CAF Chaia A Dalal A Goland T Gonzalez M Morduch J and Schiff R 2009 Half the World is Unbanked Financial Access Initiative Framing Note October 2009 Financial Access Initiative ( http://mmublog.org/wp-content/files_mf/110109halfunbanked_0_4.pdf) Accessed 1 October 2011. Christophers B 2009 Complexity, finance and progress in human geography Progress in Human Geography 33 (6) 807-824 Clark G and Wojcik D 2007 The geography of finance: corporate governance in the global marketplace Oxford University Press, Oxford. Clarke G, Cull R, Peria, M and Sanchez S 2005 Bank Lending to Small Businesses in Latin America: Does Bank Origin Matter? Journal of Money, Credit and Banking 37 (1) 83–118. Coleman M 2002 Thinking about the World Bank’s “accordion” geography of financial globalization Political Geography 21 (4) 495-524. Corbridge S 1988 The Debt Crisis and the Crisis of Global Regulation Geoforum 19 (1) 109-130. Corbridge S Thrift N and Martin R eds 1994 Money, power and space Blackwell, Oxford. Cornia A 2012 Inequality Trends and their Determinants Latin America over 1990-2010 UNU-WIDER Working Paper No. 2012/09. Demirguc-Kunt A and Klapper L 2012 Measuring Financial Inclusion: The Global Findex Database World Bank Policy Research Working Paper 6025 Finance and Private Sector Development Team, Development Research Group, World Bank. De Soto H. 1989 The other path: the invisible revolution in the Third World I. B. Tauris, London. De Soto H 2000 The Mystery of Capital: Why Capitalism Triumphs in the West and Fails Everywhere Else Basic Books, New York. De Soto H 2006 An Approach to Extralegality and Dead Capital in 12 Countries of the Region Inter-American Development Bank, Washington DC. Detragiache E Tressel T and Gupta P 2008 Foreign Banks in Poor Countries: Theory and Evidence Journal of Finance LXIII (5) 2123-2159. Dietz J 1989 The Debt Cycle and Restructuring in Latin America Latin American Perspectives 16 (1) 13-30. Diniz E Birochi R and Pozzebon M 2011 (in press) Triggers and barriers to financial inclusion: The use of ICT-based branchless banking in an Amazon county Electronic Commerce and Research Applications (2011). Dymski G 2009 The global financial customer and the spatiality of exclusion after the ‘end of geography’ Cambridge Journal of Regions Economy and Society 2 (2) 267-285. ECLAC (UN Economic Commission for Latin America and the Caribbean) 2011 Economic Survey of Latin America and the Caribbean, Economic Development Division Briefing Paper (http://www.eclac.org/publicaciones/xml/2/43992/2011-286-EEI-Regional_overview-web.pdf) Accessed 13 August 2011. Fuller D and Mellor M 2008 Banking for the Poor: Addressing the needs of financially excluded communities in Newcastle upon Tyne Urban Studies 45 (7) 1505-1524. Galindo A and Leiderman L 2005 Living with Dollarization and the Route to Dedollarization Inter-American Development Bank Research Department Working Paper 526. Gërxhani K 2004 The Informal Sector in Developed and Less Developed Countries: A Literature Survey Public Choice 120 (3-4), 267-300. Gomez Sabaini J 2006 Evolución y Situación Tributaria en América Latina: Una Serie de Temas para la Discusión in Cetrángolo O and Gomez Sabaini J eds Tributación en América Latina: En Busca de una Nueva Agenda de Reformas ECLAC, Santiago 39-130. Griffith-Jones S and Sunkel O 1986 Debt and development crises in Latin America: The end of an illusion. Clarendon Press: Oxford. Hart K 1971 Informal income opportunities and Urban Employment in Ghana, paper delivered to Conference on Urban Unemployment in Africa, Institute of Development Studies, University of Sussex, 12-16 September, 1971. Hinson R 2011 Banking the poor: The role of mobiles Journal of Financial Services Marketing 15 ( 4), 320-333. IADB (Interamerican Development Bank) 2006 “Dead capital” in 12 Latin American countries worth $1.2 trillion, according to report IADB News Release June 12 2006. IADB 2008 Microfinance in Latin America and the Caribbean - 2008 Data Update, April 5, 2008 (http://idbdocs.iadb.org/wsdocs/getdocument.aspx?docnum=1384010) Accessed 29 June 2009. IADB 2011 Microfinance lending in Latin America and the Caribbean rose 23 percent in 2010 IADB news release October 12 2011 (http://www.iadb.org/en/news/news-releases/2011-10-12/2010-latin-america-microfinance-data,9591.html) Accessed 2 June 13 September 2012. IARIW 2009 Special Conference on Measuring the Informal Economy in Developing Countries Review of Income and Wealth 55 (2) June 2009, 399–402. ILO (International Labour Organization) 2007 The Informal Economy: enabling transition to formalization Working Paper ISIE/2007/1, ILO, Geneva ILO (International Labour Organization) 2008 World of Work 2008: Income Inequalities in the Age of Financial Globalization International Institute for Labour Studies, International Labour Organization, Geneva. ILO 2009 2008 Labour Overview – Latin America and the Caribbean ILO Regional Office for Latin America and the Caribbean, Lima, Peru. Jara A Moreno R and Tovar C 2009 The global crisis and Latin America: financial impact and policy responses BIS Quarterly Review June 2009, 53-68. Joshi H 1980 The Informal Urban Economy and Its Boundaries, Economic and Political Weekly Vol 15 (13), 638-644. Kelly P 2001 Metaphors of meltdown: political representations of economic space in the Asian financial crisis Environment and Planning D: Society and Space 19(6) 719 – 742. Kendall J Mylenko N and Ponce A 2010 Measuring Financial Access around the World World Bank Policy Research Working Paper 5253, Financial and Private Sector Development, World Bank, Washington. King R and Levine R 1993 Finance and growth: Schumpeter might be right. Quarterly Journal of Economics 108(3), 717-737. Lee R Clark G Pollard J and Leyshon A 2009 The remit of financial geography – before and after the crisis Journal of Economic Geography 9 (5) 723-747. Leyshon A 1995 Geographies of Money and Finance I Progress in Human Geography 19 (4) 531-543. Leyshon A 1998 Geographies of Money and Finance III Progress in Human Geography 22 (3) 433-466. Leyshon A and Thrift N 1996 Money/Space: Geographies of Monetary Transformation Routledge, London. Lopez J and Perry G 2008 Inequality in Latin America: Determinants and Consequences Policy Research Working Paper 4504 Office of the Regional Chief Economist - Latin America and the Caribbean Region, The World Bank, Washington DC. Martin R 1994 Stateless monies, global financial integration and national economic autonomy: the end of Geography? in Corbridge S Martin R and Thrift N eds Money, Power and Space Blackwell, Oxford 253-278. Martin R 1999 The new economic geography of money in Martin R ed Money and the Space Economy Wiley, Chichester 3-27. Moguillansky G Studart R and Vergara S 2004 Foreign Banks in Latin America: A Paradoxical Result CEPAL Review 82 19-35. Morduch J 2000 The Microfinance Schism World Development 28 (4) April 2000, 617–629. O’Brien R 1992 Global Financial Integration: The End of Geography Royal Institute of International Affairs/Pinter Publishers, London. Ocampo J 2009 Latin America and the Global Financial Crisis Cambridge Journal of Economics, 33 (4) 703-724. Ocampo J and Vallejo J 2012 Economic Growth, Equity and Olsen T 2010 New Actors in Microfinance Lending: The Role of Regulation and Competition in Latin America Perspectives on Global Development and Technology 9 (3-4) 500-519. Oxfam (2010) The Global Economic Crisis and Developing Countries: Impact and Response, Oxfam Research Report, (http://www.oxfam.org.uk/resources/policy/economic_crisis/downloads/rr_gec_and_developing_countries_full_en_260510.pdf) Accessed 13 August 2011. Parnreiter C 2010 Global cities in Global Commodity Chains: exploring the role of Mexico City in the geography of global economic governance Global Networks 10 (1) 35-53. Phillips T 2009 A New Financial Architecture for Latin America Parts 1 & 2, Americas Program Report May – June 2009 (http://www.alternative-regionalisms.org/?p=2289) Accessed 2 October 2011. Pozuelo-Monfort J 2009 Hernando's Mystery EconoMonitor June 30, 2009, (http://www.economonitor.com/blog/2009/06/hernandos-mystery/) Accessed 2 October 2011. Prowse M 2007 The poverty and inequality debate in the UK ODI Background Note March 2007 (http://www.odi.org.uk/resources/download/4.pdf) Accessed 13 August 2011. RED 2011 Financial services for development: promoting access in Latin America: Report on Economics and Development Series Corporación Andina de Fomento (CAF). Rocha J Brown E and Cloke J (2011) Of legitimate and illegitimate corruption: bankruptcies in Nicaragua Critical Perspectives on International Business 7 (2) 159-176. Roddick J 1988 The Dance of the Millions: Latin America and the Debt Crisis Latin America Bureau, London. Rojas-Suarez L 2007 The Provision of Banking Services In Latin America: Obstacles and Recommendations Centre for Global Development Working Paper Number 124. Rojas-Suarez R 2010 The International Financial Crisis: Eight Lessons for and from Latin America Centre for Global Development Working Paper Number 202. Roman E 2003 Acceso al crédito bancario de las microempresas chilenas: lecciones de la década de los noventa Financiamiento del desarrollo series No. 138 Unidad de Estudios Especiales, CEPAL, Santiago de Chile. Sagebien J Lindsay N Campbell P Cameron R and Smith N 2008 The corporate social responsibility of Canadian mining companies in Latin America: A systems perspective Canadian Foreign Policy Journal 14 (3) 103-128. Sarre P 2007 Understanding the Geography of International Finance Geography Compass 1 (5) 1076-1096. Solo T 2011 Why Latin America urgently needs CRA, and why CRA won't work for Latin America Community Development Investment Review 2011 134-140. Stallings B 1987 Banker to the Third World: U.S. portfolio investment in Latin America, 1900-1986 University of California Press, Berkelely. Stein H 2010 Financial liberalisation, institutional transformation and credit allocation in developing countries: the World Bank and the internationalisation of banking Camb. J. Econ. (2010) 34(2) 257-273. Stiglitz J 2005 Finance for Development in Ayogu M Ross D eds Development Dilemmas: The Methods and Political Ethics of Growth Policy Routledge, London 15-29. Taylor P Cloke J and Brown E 2008 Mass market credit in seven leading Latin American cities Mastercard Insights Series (http://www.mastercard.com/us/company/en/insights/pdfs/2008/LACmassmarkets.pdf) Accessed 4 July 2011. Tejerina L and Westley G 2007 Financial Services for the Poor: Household Survey Sources and Gaps in Borrowing and Saving Sustainable Development Department Technical Papers Series Inter-American Development Bank, Thomas J 2002 Decent work in the informal sector: Latin America International Labour Organization, Geneva. Thrift N and Leyshon A 1988 ‘The gambling propensity’: Banks, developing country debt exposures and the new international financial system Geoforum 19 (1) 55-69. United Nations 2011 IV: Regional Developments and Outlook, World Economic Situation and Prospects (http://www.un.org/en/development/desa/policy/wesp/index.shtml) Accessed 13 August 2011. Tokman V 2007 The informal economy, insecurity and social cohesion in Latin America International Labour Review 146 (1-2) March–June 2007, 81–107. Valenzuela M 2005 Informality and Gender in Latin America Policy Integration Department, Working Paper No 60 International Labour Office, Geneva. Van Hulten A and Webber M 2010 Do developing countries need ‘good’ institutions and policies and deep financial markets to benefit from capital account liberalization? Journal of Economic Geography, 10 (2) 283-319. Wagle U 2010 Does Low Inequality Cause Low Poverty? Evidence from High-Income and Developing Countries Poverty & Public Policy 2 (3) Article 4. Warf B 2002 Tailored for Panama: Offshore Banking at the Crossroads of the Americas Geografiska Annaler, 84 B(1) 33–47. Wilkinson J 2009 Globalization of Agribusiness and Developing World Food Systems Monthly Review 61 (4). Wojcik D and Burger C 2010 Listing BRICS: Stock issuers from Brazil, Russia, India and China in New York, London and Luxembourg Economic Geography 86 (3) 275-296. World Bank 2011 Latin America's population growth slows but region's services still insufficient World Bank October 21st 2011 (http://go.worldbank.org/I6VGAJX960 ) Accessed 13 September 2012.

NOTES* Ed Brown, Department of Geography, Loughborough University, UK, email: E.D.Brown@lboro.ac.uk ** Francisco Castañeda, Faculty of Economics and Business Administration, Universidad de Santiago de Chile ** Jon Cloke, Department of Geography, Loughborough University, UK ** Peter J. Taylor, School of Built and Natural Environment, Northumbria University, Newcastle upon Tyne, UK 1. A good example of this approach is the ‘FINDEX’, the global financial inclusion index developed by Demirguc-Kunt and Klapper (2012). 2. An important sub-set of this literature is of course that surrounding the sub-prime mortgage lending boom in the US and its relationship to the global financial crisis. 3. Socio-Economic Database for Latin America and the Caribbean (SEDLAC) poverty statistics, available at http://sedlac.econo.unlp.edu.ar/eng/statistics-detalle.php?idE=34, accessed 13/8/11. 4. In 2000, for instance, micro-businesses constituted 82.51% of businesses in Chile but only 38.2% had access to credit by 2003 (Roman 2003). 5. However, due to using several languages, some data might have been lost in translation, or simply we might have not accessed the relevant sources. 6. An exploration of the substantial empirical and theoretical work on the informal sector is plainly outside the remit of this piece. A range of useful and very different overviews can be found in De Soto, 1989; Gërxhani, 2004; ILO, 2007; Joshi, 1980 and IARIW, 2009. 7. See Morduch, 2000 for a good account of the struggle over the ‘soul’ of microfinance.

Note: This Research Bulletin has been published in The Geographical Journal, 179 (3), (2013), 198-210 |

|||||||||||||