GaWC Research Bulletin 314 |

|

|

|

This Research Bulletin has been published in Journal of Economic Geography, 11 (1), (2011), 87-117. Please refer to the published version when quoting the paper.

IntroductionIt was ten years ago, just after the Asian financial crisis, that Time magazine (February 15, 1999) placed Federal Reserve Chairman Alan Greenspan, US Treasury Secretary Robert Rubin, and his deputy Larry Summers on its cover. They were labelled “The Three Marketeers” (Ramo, 1999) who ostensibly saved the world economy by masterminding International Monetary Fund (IMF) rescue packages for the failing Asian banks and financial systems. The irony is palpable given the failures of the US banking system as witnessed since September 2008. America’s financial leadership has been shaken not only due to the failures of its key financial institutions but also for a rescue package that contradicts the fiscal austerity it stipulated through the IMF during the 1997 Asian financial crisis (Stiglitz, 2008). This turn of events have even prompted some Chinese commentators to quip that the US is displaying “socialism with American characteristics” (The Atlantic Online, December 2008). At the same time, China’s growing financial clout with its huge foreign reserves, its continued funding of American debt, and its prominence at the G20 summit in London to tackle the global financial crisis have fed expectations of a shift in the geopolitical landscape to one that is less obviously centred on US leadership (The Economist, 8 April 2009). These changing relations are not only due to China’s growing economic strengths as an industrial powerhouse and consumer market; China is also developing its financial markets and systems in ways that are increasingly connected to global financial flows and practices. The instability of modern markets as seen in both financial crises would come as no surprise to Karl Polanyi ([1944] 2001), who has long challenged the idea that there is anything ‘natural’ or universal about markets and emphasises their cultural and political underpinnings. For Polanyi, the market, and the economy more broadly, is an “instituted process” (Polanyi, [1957] 2001) that is anchored in other social institutions and practices. Written after the Great Depression in the 1930s, The Great Transformation exposes the myth of the self-sustaining and perpetuating market and highlights its complex nature and chaotic tendencies. Now, in the dramatic months following the collapse of numerous American and European banks, the unprecedented intervention of their respective governments, and economic stimulus to avoid another Great Depression, these events seem to affirm the validity and continued relevance of Polanyi’s approach to the understanding of market, society and institutions. The current financial crisis is perhaps a timely reminder of the need to deconstruct essentialist or naturalised notions of markets and to critically reflect on the nature of capitalist accumulation over the past few decades. If the current financial crisis has raised important questions regarding the nature of markets, the geographical flows of different market knowledge, and the contingency of market structures and practices, the on-going reconfiguration of China’s banking markets presents an opportunity to examine those questions. In this paper, I examine how financial markets in China are being constructed and reconfigured through heterogeneous knowledge networks. In the context of developing new banking regulations and financial services in China, market ideas and practices are circulated through knowledge networks amongst regulators, banks, professional organisations and individual actors across national and sectoral boundaries. These networks are heterogeneous in that the exchange and circulation of knowledge is mediated through different market participants who hold different interpretations and agendas about possible forms of markets. This process of negotiation and conflict resolution between diverse actors form the main focus of my empirical enquiry in China, in demonstrating how markets are ontologically unstable and constantly reconfigured through the entangling and disentangling of multiscalar knowledge networks. My objective is not just to provide an empirical study of the Chinese banking industry, although that is undoubtedly an important aim for a rapidly evolving sector of increasing global significance. Conceptually, I want to argue against a simplistic reading of market construction, ideas and practices, that might lead one to read the Chinese case as another example of ‘opening up’ a banking sector to foreign investors, the top down transfer of ‘best practices’ from global centres of authority, and another victim to the bulldozer of neoliberal market logic. Instead, I demonstrate how market ideas and practices are actively constructed and reconfigured within networks of knowledge and learning that circulate across boundaries and scales, such that new forms of knowledge are created in conjectural spaces of negotiations. I argue that it is by analysing the process of interaction and negotiation between diverse market actors that the richness and temporality of market meanings and practices are revealed and new forms of market knowledges are produced. The rest of this paper develops these arguments in six sections. In section 2, I problematise ‘essentialist’ notions of markets and highlight the importance of deconstructing markets by examining its actors, structures and practices. In section 3, I present the framework of knowledge networks as used in this paper to examine the process of marketisation and describe my methodological approach. Section 4 outlines recent changes in China’s banking sector, focusing on the changing roles of Chinese and foreign banks. In section 5, I examine the processes through which knowledge networks are established in developing ‘best practices’ for China’s banking markets. These networks stretch across spatial scales and national boundaries and demonstrate the heterogeneity of knowledge flows and market actors (including firms, institutions and individual actors) that interact in the marketisation of China’s banking sector. This is followed by a case study of China’s World Trade Organisation (WTO) membership and commitment to banking reforms in section 6. While the liberalisation of its banking sector could be seen as the adoption of a certain model of market capitalism as embodied by the WTO, actual interpretation and implementation on the ground reveals the tangled and messy character of markets as regulators, foreign banks and domestic banks negotiate different interpretations of ‘fair competition’ in the reconfiguration of China’s banking sector. The paper concludes by evaluating the significance of these findings for the theoretical relevance of and future research on markets. Problematising the ‘essentialist’ marketWhether as an idea(l), a system or as economic practice, markets lie at the heart of capitalist societies but they remain one of the most elusive concepts within social sciences. While economic geographers and other social scientists have been criticised for being slow in engaging with contemporary capitalism though the theoretical lens of the market (Sayer, 2001), an emerging literature in the social sciences has begun to engage with the nature, construction and (re)production of markets. Although they do not always refer directly to Polanyi, a key feature of this literature is the insistence that markets, like other institutions involved in economic practices, are not ontologically stable, unified, straightforward or entirely predictable (Gibson-Graham, 1996, 2006; O’Neill, 2001; Slater, 2002; Larner, 2003; Metcalfe and Warde, 2003; MacKenzie, 2005; Peck, 2005; Peck and Theodore, 2007); they are riddled with contradictions, they can take on multiple forms and may have unexpected outcomes as various actors (be they states, firms, institutions or individuals) interact in the active production of markets (ideas, practices, regulations) (French, 2000, 2002; Krippner, 2001; Knorr Cetina and Preda, 2005; MacKenzie, 2006; Hall, 2007). Why is it important to clarify our conceptual treatment of markets as unstable, as an instituted process and as embedded in socioeconomic relations? The rise of globalised neoliberal capitalism in the late 20th century has increasingly established a hegemonic conception of markets as the most effective and progressive mechanism for delivering economic growth and prosperity. This discourse is legitimised by essentialist propositions of so-called ‘market virtues’ (Table 1), which treats market exchange as the atomic structure of all economic processes and as the default form of economic coordination. This is problematic as other forms of organisation become marginalised or treated as suboptimal exceptions (Sayer, 2003). The essentialist treatment of markets is reflected in the prevalence of neoliberal dogmatism and fatalism, which are driving a particular model of economic development as the only workable model (see also Peck and Tickell, 2002). The assumed progression of market practices in socialist economies is one such example, in which the proposals meant to effect a transition from planned to market economy forecloses considerations of alternative forms of exchange relations and structures and the institutional contexts of these markets that vary across Eastern Europe and China (Lie, 1997; Murphy, 2003; Gibson-Graham, 2006; Swain, 2006). These problematics point to the need for unpacking the ‘essentialist’ and ‘virtuous’ market and to scrutinise its inner workings through its microstructures, institutions and constituent actors. This is my objective in examining the construction and reconfiguration of China’s banking markets through knowledge networks. Table 1: Propositions of the ‘market virtues’

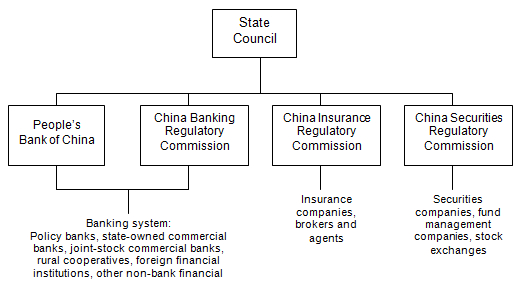

Reconfiguring markets through knowledge networks: framework and methodologyTo examine how financial markets in China are being constructed and reconfigured, I draw upon the literature on geographies of knowledge and learning for my framework of analysis. The dynamic role of knowledge in the capitalist space economy has long held the interest of geographers, especially with regards to creating and sustaining the competitiveness of localised groups of firms in national and regional innovation systems, industrial districts and clusters, and neo-Marshallian nodes (Amin and Thrift, 1992; Asheim, 1996; Malmberg, 1997; Maskell and Malmberg, 1999; Malecki, 2000; MacKinnon et al., 2002). While a key contribution to this field has been the role of tacit (rather than codified or explicit) knowledge in sustaining regional competitiveness (e.g. Gertler, 1995, 2003; Morgan, 1997; Storper, 1997), economic geographers are increasingly moving beyond this regional approach to explore diverse means of knowledge creation and transfer through territorially unbounded networks (see, for example, critiques by Malmberg, 2003; Williams, 2006; Hughes, 2007; Vallance, 2007). Studies on the global organisation of transnational corporations (TNCs) (Amin and Cohendet, 1999, 2004; Beaverstock, 2004; Faulconbridge, 2006; Wrigley et al., 2005), cross-firm project collaborations (Grahber, 2002, 2004; Girard and Stark, 2002), global networks of business knowledge systems (Thrift, 1999; French, 2000; Leyshon and Pollard, 2000; Thrift and Olds, 2005; Hall, 2009) and the roles of transnational migrants (Bunnell and Coe, 2001; Coe and Bunnell, 2003; Williams, 2006) suggest that circuits for the production and dissemination of knowledge are forming on an increasingly global scale, which marks a departure from the conception of knowledge as being fixed in localised sets of relations and institutions. In developing banking regulation, and introducing new financial products and services, China is actively learning and importing market ideas and practices on a global scale, although this flow of knowledge is far from straight forward, as I will show later in the paper. My approach in this paper is to analyse the network processes in the creation and reconfiguration of financial knowledge and expertise in China, by recognising these networks as i) multi-scalar and heterogeneous and ii) contested and unstable. By acknowledging networks as multi-scalar and heterogenous, I concur with Allen’s (2000: 28) argument that “[t]here is no one spatial template through which associational understanding or active comprehension takes place. Rather, knowledge translation involves mobile, distanciated forms of information as much as it does proximate relationships” (see also Allen, 2002). The concepts of knowledge networks and communities of practice are particularly salient in understanding the flows and creation of market ideas and practices. The metaphor of the network captures the webs of interconnected actors through which economic knowledge is produced, exchanged and circulated (Coe and Bunnell, 2003; Amin and Cohendet, 2004; Faulconbridge, 2006). The notion of ‘communities of practice’ (Wenger, 1998) permits understanding of learning that extends beyond the firm to include external agents (such as state institutions, other firms and individual actors) and highlights the heterogeneity of networks through which knowledge is circulated (Amin, 2002; Amin and Cohendet, 2004; Grahber and Ibert, 2006). In this paper, I examine the socioeconomic practices of market knowledge in China by mapping the networks between regulators, banks, professional organisations and individual actors as they stretch across national boundaries and spatial scales. This network perspective of knowledge and learning enables us to focus on the flows and circulation of people/knowledge between various sites, to reveal important transnational connections in the creation of market knowledge and practices as embedded in different national territories. Such an approach also highlights the role of transnational migrants in knowledge networks within a literature that has largely focused on TNCs and firm level analysis. In recognition of the heterogeneity of these networks, I emphasise the ways in which the exchange and circulation of knowledge is mediated through different market participants with different interests, interpretations and agendas, which renders them inherently unstable and open to contestations. Networks do not necessarily fuse the self-interest of different actors into a harmonious and egalitarian whole but may be characterised by inequalities of power, strategic coalitions, dissembling and opportunistic collaboration.1 In this paper, I adopt a relational approach centred on tracing the practices of socioeconomic actors who are embedded in “relational geometries”; these networks of power and relationality are not fixed or stable but are dynamic and open ended (Yeung H, 2005; see also Yeung H, 2003; Jones, 2008; Bathelt and Glücker, 2003). Rather than harmonious cooperation ensured by the invisible hand or the coercive power of the state, distinct social groups construct ‘markets’ through processes of negotiation and conflict resolution against other groups and other possible forms of markets. This process of negotiation and conflict resolution between diverse actors forms the main focus of my empirical enquiry in China, in demonstrating how markets are ontologically unstable and constantly reconfigured through the entangling and disentangling of knowledge networks. The empirical analysis in this paper is based on field research conducted in Shanghai (with some supplementary data from London) between August 2005 and February 2007. Shanghai is currently the most developed financial centre on mainland China with the highest concentration of foreign banks and broad representation of Chinese financial institutions along with professional organisations. It is therefore a prime location for studying knowledge networks and market practices given the density and richness of economic interaction amongst its diverse range of market participants. Fifty-one interviews were conducted with foreign and Chinese financial institutions (banks and some securities companies), Chinese regulators and officials, and foreign chambers of commerce. Interviews were conducted in a mix of English and Mandarin and were complemented by secondary data sources that provided contextual information as well as a means of triangulating interview data. These include research conducted by Chinese scholars and analysts on China’s financial markets and regulatory changes, statistical yearbooks, government reports, articles from local newspapers (e.g. China Daily and Shanghai Daily) and business magazines (e.g. BizShanghai), and announcements and press releases from banks and regulators. I also kept a field journal to record observations made outside of formal interviews and events in local and national politics, particularly those relating to changes in the finance industry or being circulated in the industry grapevine. Changes in China’s financial marketsWhen the People’s Republic of China was declared in 1949, the mono-banking system of the Soviet Union was adopted as a model. The People’s Bank of China (PBOC) had the main responsibility for cash, credit and settlement. State-owned banks such as Bank of China (BOC), Bank of Communications (BOCOM) and Agricultural Bank of China (ABC) mostly functioned as extensions of the PBOC in providing operating capital to state-owned enterprises (SOEs) with no incentives to compete with one another. As part of its economic reforms under the Open Door policy in 1978, China has been restructuring its banking sector from a mono-banking system to an increasingly open commercial banking system that offers a diversified range of financial products and services. In the early 1980s, state-owned commercial banks – BOC, ABC, BOCOM, China Construction Bank (CCB) and Industrial and Commercial Bank of China (ICBC) – were established to take over the commercial lending and branch networks of the PBOC (Leung and Mok, 2000).2 The PBOC subsequently assumed the role of a central bank with responsibilities for monetary policies, financial regulation and as the government’s banker. New banks also entered the market as joint-stock commercial banks partly owned by local governments and SOEs. They include CITIC Industrial Banks, Everbright Banks of China, Shenzhen Development Bank, China Merchants Bank, Shanghai Pudong Development Bank and China Bohai Bank.3 The diversification and restructuring of the banking system became even more prominent in the 1990s with the active promotion of tertiary sector investments in finance, trade and advanced producer services by the central government. Shanghai was appointed as the ‘dragonhead’ in this endeavour – to be a new flagship city connecting China to the global economy (MacPherson, 1994; Yatsko, 2001; Yusuf and Wu, 2002; Wu, 2003). One of the most important reforms is the opening up of the Chinese banking sector to foreign banks who would bring in foreign capital and introduce new banking products and practices from abroad (CBRC, 2007b; Berger et al., 2009). As of 2006, there were more than 70 foreign banks with representative or branch offices in China, of which 30 has purchased stakes in 21 Chinese commercial banks through strategic investment schemes (CBRC, 2007a). While they were initially only allowed to engage in foreign currency business under restricted banking licenses and in selected Special Economic Zones, these geographical and business restrictions have been gradually lifted such that foreign banks can now offer Renminbi (RMB) banking services. The range of products and services offered within the Chinese banking system has also expanded, particularly in the case of previously underdeveloped market segments such as loans to small and medium enterprises (SMEs), trade financing and syndicated loans. The range and complexity of financial products has also increased with the establishment of the stock exchanges in Shanghai and Shenzhen in 1990, commodity exchange in Dalian in 1993 and futures exchange in Shanghai in 1999. Three regulatory bodies were created as spin-offs from the PBOC to supervise these new and evolving financial markets (Walter and Howie, 2001). The China Securities Regulatory Commission (CSRC) was established in 1992 as China experimented with stock markets in Shanghai and Shenzhen; the China Insurance Regulatory Commission (CIRC) was established in 1998 to regulate the insurance industry; and the China Banking Regulatory Commission (CBRC) was the latest to be set up in 2003 to implement banking reforms and open up the banking sector to foreign competition under WTO commitments (Figure 1). This allowed the central bank to focus on monetary policy and financial system stability while the three regulatory bodies focus on securities, insurance and banking regulation and restructuring. The establishment of these regulatory bodies, with their specific areas of responsibility and mandates, were widely seen as indicative of China’s commitment to reforming its financial sector along market principles and opening up to foreign investors and competition (People’s Daily, 23 April 2003). Figure 1: Structure of China’s financial system (Source: Yeung G, 2008)

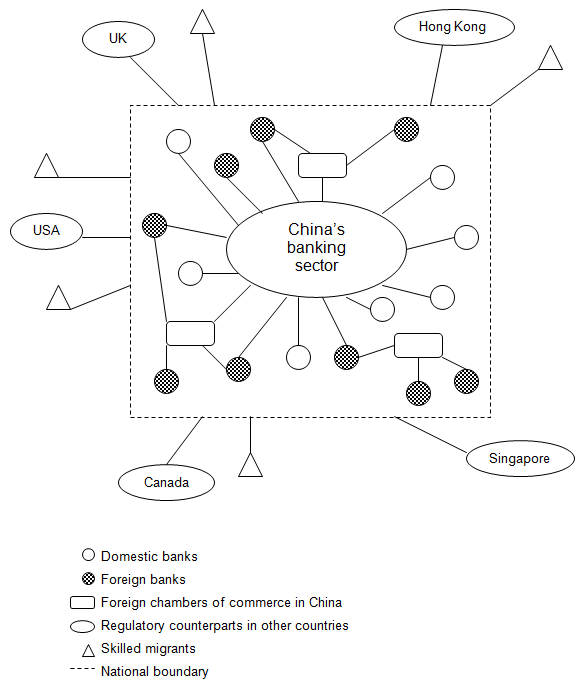

In keeping with these changes, Chinese regulators and domestic banks have sought to improve their standards of business practices, corporate management and banking regulation, for example in areas of credit rating and risk assessment. While the existing literature provides a comprehensive review of the banking reforms in China (for example, Huang, 2001; Saez, 2004; Cousin, 2007; Roland, 2007), there has been little discussion of the roles of diverse market actors and global knowledge networks in the process of reconfiguring market ideas and practices. In the rest of this paper, I will show that the process of learning and developing frameworks and expertise is fraught with contradictions and tensions between different market actors, such that it is not simply a transition or adoption of models from elsewhere but an active reconfiguration of market ideas and practices. By analysing these networks and processes, ‘markets’ are shown to be unstable assemblages of heterogeneous networks constituted by actors with different interpretations, agendas and power to influence the process of market formation. ‘Best practices’ and knowledge translationAt the launch of the CBRC in 2003, Chairman Liu Mingkang declared that “China’s financial sector has been opened up further to the outside world, while the financial supervisory regime has been brought closer to the international best practices” (quoted in EuroBiz Magazine, July 2003). While China sought to learn “international best practices” from abroad, the process was not simply a unidirectional transfer of financial expertise from selected institutions or actors. The range of knowledge networks was broad, the actors were diverse and the relevance of particular models or practices also changed over time. Figure 2 shows how different forms of market knowledges and practices were drawn from a range of learning networks stretching across national boundaries and spatial scales. At the regulatory level, formal networks were established with counterparts in other financial centres to learn from different models of regulation and banking practices. At the individual level, knowledgeable experts were targeted through recruitment strategies. Within the Chinese banking industry, foreign and domestic banks, and interest groups such as foreign chambers of commerce constituted another layer of knowledge networks that actively construct and reconfigure changing conditions of the Chinese banking sector through advice and lobbying on new banking products and standards. The next three sections will examine each of these layers of knowledge networks in turn and discuss how they interact in the transformation of China’s banking sector. Figure 2: Multi-scalar knowledge networks in reconfiguring China’s banking market

Regulatory Learning PartnersSpecific channels of knowledge and skills transfer were set up by Chinese regulators to connect with sources of expertise abroad. The CBRC has signed bilateral Regulatory Cooperation Memorandum of Understanding (jianguan hezuo beiwanglu) with 22 overseas counterparts ranging from the US, UK, Canada, and Australia to South Korea, Hong Kong and Singapore (CBRC, 2007b). These memorandums of understanding (MOUs) provided frameworks for cooperation and communication channels for exchanging regulatory and technical information. Through these international channels, Chinese regulators acquired technical support and accessed different conceptual understandings of banking and finance restructuring and management, learning from different regulatory models and experience. These knowledge flows were facilitated by specially organised conferences and workshops held in China or other countries, fact-finding trips to different financial centres, and training and internship programmes with learning partners. The Monetary Authority of Singapore, the Federal Reserve of the USA, the IMF, World Bank and Asian Development Bank regularly hosted officials from the CBRC, CSRC, and PBOC on training workshops or attachment programmes in their respective country offices and also sent representatives to China every year on training visits and exchange programmes (interview data, 2006). According to a planning official in Shanghai (#19, April 2006), the idea was to “stand on the shoulders of giants”:

Using a “global view” does not mean simply measuring China against a particular standard set by some global financial authority and then making local changes to meet those standards. The objective of establishing these networks of learning and cooperation is to learn from the regulatory models and methods of different countries and assess how best to implement particular aspects of those in China. These networks are not just conduits for knowledge transfer and adoption; instead, they constitute a pool of expertise from which particular aspects of banking regulation or product knowledge could be selected and adapted to suit China’s institutional and political history and economic aspirations. As such, these forms of knowledge and learning are better thought of as translations. This notion of translation takes us beyond simplistic ideas of transferring immutable knowledge and leads to consideration of knowledge expansion, modification and creation in the marketisation of China’s banking sector. This is illustrated by how, within these formalised networks of knowledge and learning, some regulatory models or practices were deemed more attractive or suitable than others with respect to China’s political and economic context. While Hong Kong’s proximity and success as an international financial centre and close economic ties with China might render it a ‘natural’ role model for mainland China’s financial sector reforms, its particular economic history and different governance system (under the one-country-two-system model) made it problematic for transferring regulatory principles and frameworks. A Chinese respondent also pointed out possible political sensitivities and the issue of ‘face’ on the part of the Chinese central government in their reluctance to ‘learn’ (i.e. acknowledge ignorance) from a city or province, however successful. In examining the experience of other developing economies, Singapore’s more conservative regulatory style and success based on a managed market-economy was deemed closer to China’s experience and had been highlighted as a valued learning partner (Shanghai government official: #28, April 2006). Amongst developed economies, the UK has been a preferred learning partner and was often consulted on various aspects of financial reforms. Special committees consisting of industry experts, economists and regulators from the City of London have advised the Chinese on areas such as interest rates deregulation and bankruptcy laws. While this could be due to London’s reputation as one of the most successful and important financial centres in the world, more personal social connections also played a significant role in such knowledge networks. Liu Mingkang, the chairman of CBRC, obtained his postgraduate degree in the UK and was familiar with the regulatory system of British banking and finance. He was reputedly very good friends with Howard Davies, former chairman of the Financial Services Authority (FSA) and often fielded the possibility of modelling the Chinese financial regulatory system on the FSA. While this personal connection may seem serendipitous, other networks of knowledge and learning were evident in the working groups from the CBRC that visited the FSA on regular learning missions, as well as the steady stream of Chinese interns working within the FSA. These networks were important not only for the learning of ideas and techniques but also to establish important contacts that were maintained upon their return to China (interview data, 2006). While some models and expertise were deemed more suitable than others, the relevance and desirability of different models also changed over time. The UK model had been influential as reflected in the strength of knowledge networks established between the CBRC and the FSA, but the recent financial crisis has changed perceptions of what constitutes ‘best practices’ for China. The collapse, bail out and nationalisation (in effect if not in principle) of numerous British, American and European banks since September 2008 have altered Chinese confidence in the robustness and suitability of their financial systems as models for China. Instead, the relative resilience of Canada’s banks and financial system has captured the interest of Chinese regulators seeking different models and forms of expertise. In February 2009, the first Canada-China Symposium on Securities was held in Hainan, China, as a special invitation for Canadian banks, securities firms and regulators to share their knowledge and experience with Chinese counterparts. Canadian financial institutions have been much less aggressive than their European and American counterparts in overseas investment and expansion into newly opened markets in China’s finance sector. While this has resulted in a much smaller Canadian presence in China, a relatively more conservative approach has also rendered the Canadian financial system more resilient to the current financial crisis and has placed Canada in the spotlight for developing best practices and risk management programmes (CNW Group, 25 February 2009; Mavin, 2009). Therefore, instead of drawing from some fixed global standard, the concept of ‘best practices’ for developing China’s banking markets has been rather elastic. On one level, these knowledge networks combined insights from different regulatory models with regards to Chinese’s political and economic contexts; in addition, the relevance and appeal of different forms of market knowledge has also shifted with wider changes in the global economy. Recruiting Individual ExpertsIn addition to establishing networks of learning and knowledge with regulatory counterparts overseas, individual experts also play an important role in the circulation and translation of knowledge. Other than localised circulation of embodied, tacit knowledge within a knowledge community, which has been well documented within economic geography, exchanges of knowledge also takes place beyond firm networks and particularly through the migratory patterns of mobile individuals. A well-documented example of this is the transnational communities of foreign-born engineers, entrepreneurs and managers that have formed between Silicon Valley and home countries of India, China, Taiwan and Israel (Saxenian, 1999, 2006; Hsu and Saxenian, 2000). The key agency of these returnee migrants is not so much in directly transferring technical know-how back to their home countries, but in helping to transform domestic institutions by advising governments on legal, regulatory and capital market reforms, improving infrastructure, universities, research and training institutions, and creating forums for information exchange among firms and institutions (Saxenian, 2006). This parallels the role played by the Chinese ‘hai gui pai’, or faction of returnees, in China’s financial reforms. A key strategy in reforming China’s financial system had been to attract overseas Chinese to return to China.4 They were largely educated in the USA, Europe and Australia and their recruitment was meant to tap into their knowledge, experience and contacts from working in centres of global finance such as Wall Street, the City of London or Hong Kong. Two of the most prominent ‘hai gui pai’ were Gao Xiqing and Laura Cha (commonly known as Shi Meilun on the mainland), both of whom were vice-chairman of the CSRC. Gao Xiqing had degrees in law from the University of International Business in Beijing and Duke University. He spent a number of years working at a Wall Street law firm where he gained experience and insights into the operations of the New York Stock Exchange and the Securities and Exchange Commission. In 1988, he returned to China to a series of top-level positions in regulatory bodies and state owned financial institutions. He served as general counsel and director of public offerings of the CSRC between 1992 and 1995 and as deputy chief executive at the Hong Kong-Macao regional office of the Bank of China from 1997 to 1999. He then went on to become vice-chairman of the CSRC from 1999 to 2003, vice-chairman for the National Council for Social Security Fund from 2003 to 2007 and is currently the president of China Investment Corporation since 2008. Laura Cha obtained her bachelor and law degrees in the USA. She practiced law in San Francisco and Hong Kong, and was formerly vice-chairman of the Hong Kong Securities and Futures Commission. From 2001 to 2004, she served as vice-chairman of the CSRC as part of an initiative by then premier Zhu Rongji to hire world-class talent into China to implement financial reforms. She continues to hold positions of influence in Hong Kong and China in regulatory, government and business circles, currently acting as non-official member of the Executive Council of Hong Kong Government, non-executive chairman of HSBC Investments Holdings, vice-chairman of the Panel of International Consultants for CSRC, and is on the board of directors of Baoshan Iron & Steel. The examples of Gao Xiqing and Laura Cha highlight the role of transnational migrants in knowledge networks within a literature that has largely focused on TNCs and firm level analysis (see Bunnell and Coe 2001; Coe and Bunnell 2003; Williams 2006). Such an approach emphasises the translation, rather than transfer or transmission of ideas and practices, as skilled migrants often encounter different perspectives and contexts that could present barriers to knowledge transfer. Although these ‘hai gui pai’ wielded considerable influence, they were sometimes criticised for promoting policies perceived to be ill-suited to China, such as the pace and style of reform being too quick or inappropriate for the local financial and regulatory system (interview data, 2006). Gao, for instance, had been a consistent advocate of a mandatory disclosure system similar to that of the US. He had been critical of the Chinese government’s insistence on approving all listed stocks as it gave an apparent signal to investors that those were good investments.5 The number of listed companies had grown dramatically as a result but in his opinion only less than 10 percent of those companies offer good value. The Chinese government, on the other hand, was more concerned about bolstering investor confidence as they embarked on the stock market experiment and was more comfortable with the familiar government’s-stamp-of-approval method, regardless of the market signals that it conveyed. Laura Cha faced similar criticism during her tenure at the CSRC from those who subscribed to the school of thought that it was the job of the regulators to boost the market. In contrast Cha thought regulators should regulate impartially to build a transparent market for the long term and not be too concerned with short-term index fluctuations. Therefore, although the high profile recruitment of Gao and Cha was a strategic move by top-level government officials to bring in financial expertise and market experience from abroad, their market ideas and practices were not always accepted. Their recommendations were often selectively adopted or rejected either within the regulatory institutions or by the State Council (higher level governing body as seen in Figure 1) on the grounds of being unsuitable for China’s economic and institutional context. Chinese returnees are often referred to as ‘sea turtles’ in a joking or slightly derogatory manner. It is a pun (homonym) on the word ‘hai gui’ which sounds the same for ‘returnees’ or ‘sea turtles’. While the label draws from how turtles return to the same beaches to lay eggs (just as these migrants return to their place of birth), it can also be read as a metaphor for the circulatory nature of expertise and experience embodied by these mobile individuals. Knowledge about financial products, systems and regulation is not simply imported from elsewhere but is evaluated with regards to the Chinese context. This circulatory nature refers to how market ideas and practices are constantly adapted and reconfigured as they circulate and encounter different interpretations and agendas and it is through these conjunctural relations that new forms of market knowledge is being constructed and negotiated in China’s financial markets. This contested process of market-making becomes clearer when we examine the knowledge networks of different market actors within the Chinese banking industry. Market Actors within the Chinese Banking IndustryWithin the Chinese banking industry, the market actors engaged in developing banking systems and financial products range from foreign and domestic financial institutions to industry associations and foreign chambers of commerce. Foreign banks play a particularly important and officially sanctioned role in “aligning the Chinese banking industry with the latest developments in global banking market” (CBRC, 2007b) and bringing financial product knowledge and expertise to local banks. One such example was SME lending, which had traditionally been neglected as Chinese state-owned banks focused on their mandate of financing SOEs (Yeung G, 2009). This historical legacy of state-directed lending meant that these banks had little experience with assessing company accounts that were often loosely kept in small or family-run companies. When the CBRC was seeking to encourage more business lending to SMEs, it consulted specific foreign banks that were successful in this loan sector to learn from their experience. Following discussions with a number of foreign banks such as Standard Chartered and HSBC, new guidelines were developed to guide and encourage Chinese state-owned banks in lending to the SME sector (interview data, 2006). However, this did not mean that the ideas and practices of foreign banks were always prioritised as local banks were also involved in regular consultations. Be fore the launch or approval of new financial products, the PBOC, CBRC or CSRC would hold rounds of consultation with banks and individual specialists to troubleshoot and identify potential problems. Prior to the passing of new regulation, draft copies would be sent out to all banks to assess market reaction and garner responses. The banks would often bring the draft regulations to their respective banking groups or associations and the groups would submit written official response if necessary. In Shanghai, the CBRC and the SMG regularly consulted both foreign and domestic financial institutions to understand their perspectives on particular issues, problems that they were facing and suggestions for improvement. Through these consultations, foreign banks put forward their interpretations of whether current policies and systems would constitute ‘best practices’ according to their experience elsewhere, while domestic banks could voice their concerns regarding how those changes might impact their business and potential problems with adapting to new ideas and practices. More often than not, foreign and domestic banks would hold conflicting views on new products or regulation or the pace of liberalisation, which required regulators to maintain a balancing act between these different interests. This is a point that I will return to later. Apart from consultative meetings on with regulators, foreign banks were also key actors in the marketisation process through their institutional affiliations with foreign chambers of commerce. In terms of recommendations and lobbying on behalf of the business interest of members, the British, European Union (EU), American and Japanese chambers of commerce were amongst the most active in China. The EU Chamber of Commerce (EUCC) in China, for example, published an annual Position Paper representing an overall view of European companies doing business in China.6 It detailed the key concerns and recommendations from each of its 30 Working Groups regarding issues such as WTO implementation, trade, regulatory concerns and broader policy-related issues. These Position Papers were presented to the Chinese government each year with the aim of improving the investment climate in China and were often used as a basis for negotiations between the EU and China for visiting delegations. As such, these chambers of commerce, the documents that they produce and their business and trade related activities also play a significant role in China’s marketisation process. The heterogeneity of actors invariably means that ideas and perspectives differ regarding the suitability of banking practices and the pace of reform. But rather than having one set of knowledge network superseding others, the reconfiguration of China’s banking sector is made up of a complex layering of different networks such that the state of market reforms at any one time is the temporary result of a balance of different forms of expertise and perspectives. The density and strength of different knowledge networks, and the influence wielded by different actors, varied depending on the relative performance of foreign and domestic financial institutions and the broader objectives of government and regulatory bodies. While the expertise of foreign banks was sought after, they were not always fully implemented if the interests of domestic banks and the stability of the Chinese banking system were endangered. The top five issues or recommendations highlighted in the EUCC Banking Working Group Position Paper, for example, had remained the same over the past five years despite repeated efforts to push for further banking reforms. While the Chinese regulators were often well aware of the concerns of foreign banks (usually with regards to easing restrictions on business licensing and financial products), reforms were not always carried through due to other political and economic considerations. The Chinese government and its regulatory bodies had to be careful about a local impression of granting too many incentives to foreign financial institutions instead of helping Chinese banks. The pace and structure of reforms deemed appropriate and desirable by foreign banks were not always compatible with the Chinese government’s objective of building a banking sector anchored by strong local banks. While foreign banks played a vital role in knowledge transfer and the development of local knowledge and expertise, they must also not be too successful to the detriment of domestic banks. The f oreign head representative of a foreign bank (#41: 27 October 2006) explained that:

Political considerations therefore play an important mediating role in the networks of knowledge and learning within the Chinese banking industry. If foreign banks were seen to be too effective in competing with domestic banks, their recommendations and expertise might not be particularly influential or valued. On the other hand, if foreign banks were too restricted in their business activities, they might lose patience with the Chinese market, at which point their recommendations would have more weight or bargaining power. As such, the reconfiguration of China’s banking markets was not borne out of a unidirectional flow of market ideas and practices from foreign financial institutions, nor were the interests of domestic banks always prioritised. Instead, new banking practices and regulation were the result of a process of negotiation between different market actors. In the above analysis, I have demonstrated how the reconfiguration of China’s banking sector can be understood through a framework of heterogeneous knowledge networks, in that the exchange and circulation of knowledge is mediated through different market participants with different interpretations and agendas about possible forms of markets. While it is important to note that market ideas and practices are contested in demonstrating the richness and diversity of market meanings, I extend the argument by highlighting that it is through this very process of contestation and negotiation that new forms of markets knowledge and practices are produced. In China’s case, market knowledge and practices were drawn from diverse sets of actors, ranging from regulatory bodies and financial firms, to chambers of commerce and knowledgeable transmigrants. There was active reconfiguration within these networks of knowledge and learning, with some being deemed more appropriate or desirable than others at different points in time. In terms of regulatory networks, the Canadian model had received greater attention as a result of the current financial crisis and the relative resilience of Canadian banks and financial system compared to the US and UK models. At the individual level, the expertise of the ‘hai gui pai’, while initially sought after, had been criticised for being ill suited to China’s economic environment. At the industry level, the influence of industry actors in terms of their advice and recommendations for new banking products and practices had also been limited at times depending on the development priorities of the government. Such networks are therefore dynamic and unstable, changing according to economic and political circumstances. They reflect the tangled, temporary and messy characteristics of market and also present opportunities for the creation of new forms of knowledge and practices. These contesting visions of China’s banking market is brought to the fore during the final stages of WTO accession at the end of 2006, which is the focus of the next section. WTO: Reconfiguring the banking sectorIn December 2001, China joined the WTO as its 143rd member and committed itself to further opening up its domestic industries to foreign imports and investment. The WTO agreement was expected to transform the existing socialist market system in China into a ‘real’ market system, and to establish Chinese global trade and production systems that comply with the global ‘rules of the game’ (Zhao et al., 2002). Accession to the WTO was also seen as China’s public recognition of marketisation and internationalisation as the primary sources of its rapid growth since the 1980s (Lu, 2006). Part of the WTO agreements involved opening up its banking sector to foreign banks with regards to the types of business (foreign or local currency banking), types of customers (corporate or retail) and by geography (cities and regions open to foreign banks). These restrictions were to be lifted according to a schedule with the result of removing all such restrictions within five years after accession (Tables 2 and 3). In other words, by the end of 2006, foreign banks in China were to receive ‘national treatment’, i.e. be treated the same as domestic Chinese banks in banking regulation (People's Daily, 12 June 2001; WTO, 2001). By end of 2006, 115 foreign banks have gained permission to provide RMB services in China. Their assets amounted to US$103.3 billion, equivalent to 1.8 percent of total banking assets in China (CBRC, 2007b). Table 2: Business sector and customer groups open to foreign banks under WTO, as agreed in 2001

Table 3: Cities and regions open to foreign banks under WTO, as agreed in 2001

The WTO schedule was a nation-state level agreement that set broad conditions to be met by various deadlines, according to a particular vision of ‘market’ espoused by the WTO. However, the reconfiguration of market ideas and practices on the ground proved to be more complex and unstable and not simply a transfer or adoption of external rules and ideas. As pillars of global financial order, the WTO along with the IMF and World Bank, have become standard-bearers for the neoliberal ideology favoured by the ‘Washington-Wall Street Alliance’ or the ‘Wall Street-Treasury-IMF complex’ (Peet, 2003; Bhagwati, 2000; Wade and Veneroso, 1998; Stiglitz, 2002). While their imposed regimen of free trade, government austerity, export-led development, deregulation and privatization had arguably disastrous consequences for many developing economies (ibid.), one should also not assume that those particular forms of neoliberal market discourses and practices always travel in some immutable forms or directions. Instead, they are better theorised as unstable assemblages that emerge and come together in often disjunctive and unexpected ways (Larner, 2003, 2009). China’s WTO accession presents a valuable opportunity to examine how different market meanings and practices interact as actors with diverse interpretations and interests negotiate their visions/versions of markets. While the objective of the WTO agreement was to bring about a level playing field for both foreign and domestic banks under the ‘national treatment’ clause, different market actors within the Chinese banking sector had different concepts of what constitutes ‘level playing field’ and ‘fair competition’, which in turn influenced the process and character of banking reforms. One example of this reconfiguration was the changing of rules regarding foreign banks’ participation in RMB currency banking services. Foreign banks had been offering foreign currency services to both corporate and retail customers since 2001 and RMB services to corporate clients since 2003. But the ‘big fish’ that foreign banks had been angling for was RMB retail banking with what was expected to be a large and expanding Chinese middle-class population. While the opening up of this banking sector might seem straight forward and unproblematic from the schedule set out in Table 2, the process of implementing these changes revealed the complexity of negotiating different ideas about the Chinese banking market. In September 2006, a draft amendment on Regulations on Administration of Foreign Banks was circulated by the CBRC to the foreign banks for their comments, relating to the opening up of RMB retail banking to foreign banks. Despite “moans and disagreements” (foreign bank: #29, October 2006) from the international banking community, the amendment was subsequently passed with little changes just before the WTO deadline of December 2006. The amended regulation stated that foreign banks that had prior approval to conduct RMB corporate business with Chinese enterprises would not be automatically permitted to conduct RMB retail business; instead, they would have to reapply and fulfil specific conditions as summarised in Table 4. The new conditions effectively restricted the expansion and activities of foreign banks in China, particularly smaller banks that were not able or willing to commit the large sum of registered capital. The deposit-to-loan ratio also restricted foreign banks’ lending strategies as they would have difficulty accumulating a substantial amount of RMB deposits within a short period of time, compared to Chinese banks with their extensive branch networks. The move had been criticised as China giving with one hand and taking with the other (Areddy, 2006; Shao and Lou, 2006). Some described the capitalisation requirements as an example of China perverting its WTO commitments as the bar for foreign banks had been set much higher than many have anticipated (Low, 2003). While the lifting of geographical and business restrictions was in keeping with the WTO timeline as listed in Tables 2 and 3, the high capitalisation requirements and other conditions made it commercially unviable or unattractive for many foreign banks. Table 4: Conditions for foreign banks to offer RMB retail banking services

The reactions of foreign and domestic banks to the amendment further revealed the multiplicity of market ideas and marketisastion as a contested process. For foreign banks, the amendment was means of controlling on their expansion as they had been deemed too successful in the Chinese banking market. There was a sense that the Chinese government might have given away too much under WTO agreements with such a tight deadline and that the local banks were in danger of being left behind. There were serious doubts amongst local respondents about the abilities of Chinese banks to catch up to international standards of management, risk control, compliance, reporting and many other areas that required a longer period of time for new concepts and methods to be learned and instituted. While the CBRC officially recognised foreign banks as being “an integral part of the Chinese banking sector” and their role in “rais[ing] the quality of banking services” with their international expertise (CBRC, 2007b), Chinese banks often viewed foreign banking strategies as treating the Chinese market like a mine, digging up what was valuable by buying up domestic banks, poaching talented employees, and depriving the locals of opportunities and wealth (interview data, 2006). The concepts of ‘level playing field’ and ‘fair competition’ were viewed rather differently by foreign and domestic banks. To foreign banks, the amended regulation gave unfair protection to local banks and did not constitute a truly level playing field. Although conditions such as having to be locally incorporated fell within the ‘national treatment’ clause of the WTO agreement (to be treated the same as locally incorporated domestic banks), the financial costs was still a significant hurdle:

On the other hand, the Chinese banks deemed it unfair if foreign investors were to be given free rein in business activities and all segments of the market before local financial institutions were fully prepared and mature as they could not actually compete effectively:

Against this background of different visions and expectations for China’s banking reforms, regulators were faced with the delicate task of juggling WTO commitments with local consideration and national politics and agendas. The nationally sanctioned goal set by the central government was for China to have a developed banking and finance sector anchored by strong domestic financial institutions. However, this broad agenda had to be worked out on the ground with diverse market actors involved in the active reconfiguration of China’s banking sector: