GaWC Research Bulletin 293 |

|

|

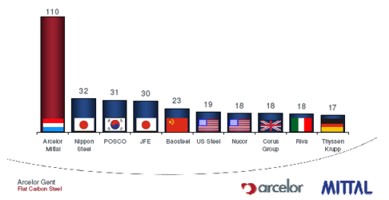

INTRODUCTIONEconomic GlobalisationFor a few years already the worldwide steel industry has been liable to a consolidation wave. This is the consequence of increasing economic globalisation and the fast industrialisation of countries like China, India and Brazil. Economic globalisation develops very fast and is a consequence of the decrease of economic borders in the world. Internationalization of economic activities involves transnational networks within different companies. The main consequences of economic globalisation in business are a worldwide free market, increasing competition, scaling-up and permanent restructuring. Thanks to the continuous inventing of new internet applications, this trend will further develop in the future. The steel industry doesn’t stay behind in this trend and in this industry the competition too is continuously intensified. Scaling-up and mergers are the most important consequences of the economic globalisation for the steel industry. The European Steel Industry in the Eighties and NinetiesIn the eighties and nineties of the 20th c. the European steel industry was characterized by losses and overcapacities year after year. A lot of steel companies had to shut down, but thanks to government support some steel companies could survive. This was also the case for the Belgian steel industry, where government support was provided for both the Walloon and the Flemish steel companies. Nevertheless the European steel companies realised they had to react to the existing situation and from this the first mergers and takeovers arouse. The Luxembourg group Arbed took over the German Klöckner Stahl and in Germany Thyssen Stahl, Hoesch Stahl and Krupp Stahl merged (1 September of 1997) to TKS. The British steel group British Steel merged (6 Oktober of 1999) with the Dutch Hoogovens to Corus. The Merger of ArcelorIn the year 2002 there was the first big merger between European steel companies. The big steel group Arcelor was created as a combine of the Luxembourg group Arbed, the French Usinor and the Spanish Aceralia. At that moment, the biggest deal of the Belgian steel companies became part of a great steel group, including Sidmar (ArcelorMittal Ghent), Cockerill-Sambre (Arcelor Liège) and ALZ (Ugine & ALZ Belgium). Origin of ArcelorMittal, the Greatest Steel Group in the WorldAt the beginning of the year 2006 the Indian steel baron Lakshmi Mittal (Mittal Steel) surprised everyone with a take-over bid on the group Arcelor, at that time the greatest steel group in the world. After a months-long take-over battle Mittal succeeded and at one go it got hold of ten percent of the worldwide steel production. Since then most Belgian steel companies integrated in the biggest steel group in the world, ArcelorMittal. The group has a lot to offer to become and to remain the strongest steel group (figure 1) in the world. Figure1. The major steel producers in the world in 2005 (in MT crude steel)

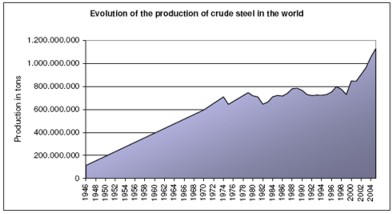

Source: Arcelor-Mittal Ghent, 2007 THE BELGIAN STEEL INDUSTRYThe consequences of these developments are substantial, also for the Belgian steel companies of ArcelorMittal. For the steel companies, a lot of factors are influenced by the globalisation and mergers in the industry and the companies have to do their best in the tough competition worldwide. The most important Belgian steel companies which are part of the group ArcelorMittal are ArcelorMittal Ghent (Sidmar) and Arcelor Liège (Cockerill-Sambre) in the sector flat carbon steel and Ugine & ALZ Belgium NV in the sector stainless steel, which consists of Ugine & ALZ Belgium in Genk (ALZ) and newcomer Ugine & ALZ Carinox in Charleroi, which started up in 2005. In this context it is interesting to analyse the evolution of two core topics of the steel industry, production and employment. ProductionThe evolution of the steel production is dependent on the economic situation in the world. This is not only the fact for the individual steel companies but also for the Belgian steel production in general and the production on a worldwide scale. In 2006 the worldwide steel production (figure 2) increased to 1,240,000,000 tons. This increase is partly due to the large rise of the production in NIC of Asia and South-America. During the past years, there were major capacity expansions in these countries and the role of the involved steel companies in the world economy is growing continuously. In particular, the major role of steel producers in China has to be mentioned. The last few years these companies show spectacular growth figures until 20% a year. Also the Indian steel industry, with a growth of about 10% a year and the Turkish with a 11%, has to be mentioned. Figure 2. Evolution of the production of crude steel in the world (1946-2005)

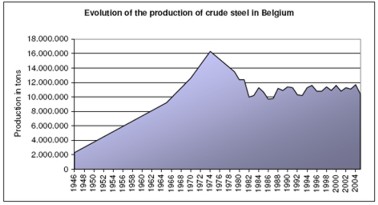

Source: De Groote, 2004; Belgian steel federation, 2000-2006; Sidmar 1990-2005; ArcelorMittal Ghent, 2006 Concerning the evolution of the Belgian steel production (figure 3), one can see the same trend is comparable to the worldwide level. For six consecutive years since 2000, we can see clearly that production also depends on the economic situation. Thanks to an advantageous situation in 2000 production rose to 11,600,000 tons, a rise of 700,000 tons compared to the production in 1999. Then the level of production showed a decrease in 2001 to 10,800,000 tons a year. In 2002 the level of production rose once again to 11,300,000. As a result of an unfavorable economic situation in 2003 and 2005 production declined to respectively 11,100,000 and 10,400,000 tons. In the years 2004 and 2006 the level of production rose to 11,700,000 and 11,600,000 tons because the economic situation improved again. Figure 3. Evolution of the production of crude steel in Belgium (1946-2005)

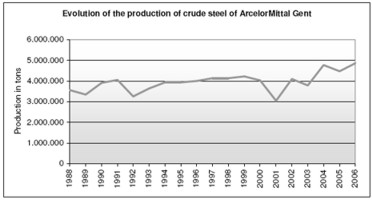

Source: De Groote, 2004 and Belgian steel federation, 2000-2006 Concerning the evolution of the production of ArcelorMittal Ghent (figure 4), one can see that since 2000 the production level has followed the same trend as for the whole Belgian steel production. In 2000 production was 4,956,000 tons while the level of production declined again to 4,155,000 tons in the following year. In 2002 production was 4,756,000 tons. In 2003 and 2005, the years when the economic situation wasn’t very good, production numbered respectively 4,508,000 and 4,055,000 tons. In they years 2004 and 2006, the level of production amounted to 4,785,000 and 5,051,000 tons. Figure 4. Evolution of the production of crude steel ArcelorMittal Ghent (1988-2006)

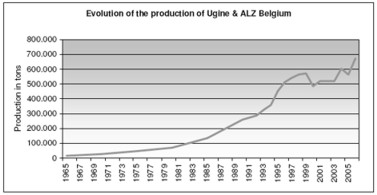

Source: Sidmar 1990-2005 and ArcelorMittal Ghent, 2006 Just as for the production of the whole Belgian steel industry and ArcelorMittal Ghent in particular, the level of production follows the worldwide economic situation. In the year 2006 the level of production of Ugine & ALZ Belgium (figure 5) increased to 673,000 tons. Figure 5. Evolution of the production of Ugine & ALZ Belgium (1965-2006)

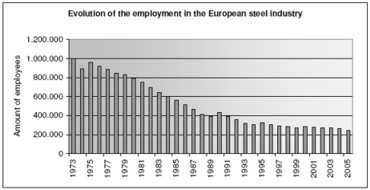

Source: Ugine & ALZ Belgium, 2006 and Sidmar, 1990-2000 EmploymentSince 1973 the employment in the European steel industry (figure 6) has significantly decreased from 998,000 employees until 247,000 employees. There are two major causes for this decrease. Firstly, there are the improvements of productivity that make it possible for companies to produce the same amount of steel with fewer employees. Secondly, some European companies disappeared during years because they merged with other companies or couldn’t produce effectively anymore. These are for example Hoesch Stahl and Krupp Stahl in Germany, British Steel in England and the steel factories of Ardoises and Isbergues in France. Further, globalisation also has the effect of shifting parts of industries to countries with lower labor costs and less severe environment regulations. In addition, there is the centralisation of services to save costs and to increase efficiency. The number of employees in these services has also been reduced. Figure 6. Evolution of the employment in the European steel industry (1973-2005)

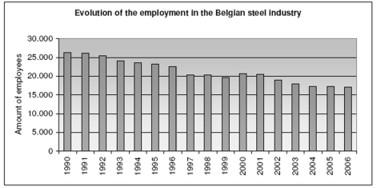

Source: ArcelorMittal Ghent, 2006 Concerning the evolution of the employment within the Belgian steel industry (figure 7), we can see there was also a decline of 9,124 employees between 1990 and 2006. The same explanation can be given for the decrease in the European steel industry. Figure 7. Evolution of the employment in the Belgian steel industry (1990-2006)

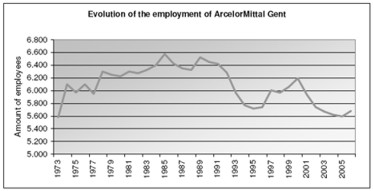

Source: Belgian steel federation, 2000-2006 For the individual Belgian steel companies this decrease trend isn’t very clear, because there are more peaks and lows for these companies. For ArcelorMittal Ghent (figure 8), there were 5,850 employees in 1973 and 5,680 in 2006. The reason for this stability is a particular and successful investment policy of the company through which there is a fixed budget every year to keep the business profitable. Figure 8. Evolution of the employment of ArcelorMittal Ghent (1973-2006)

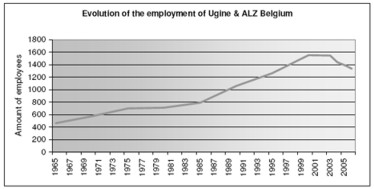

Source: Sidmar, 1990-2005 and ArcelorMittal Ghent, 2006 For Ugine & ALZ Belgium in Genk (figure 9), employment has increased from 464 to 1,336 employees since the start of the company. Here too, the increase is a consequence of the successful investment wave of the company in the past. Since 2003, however, the level of employment has slightly declined because of a centralisation of certain overhead services like informatics, finance and legal and fiscal services. Most employees could stay within the company but some had to move to other services or enterprises of the group. Figure 9. Evolution of the employment of Ugine & ALZ Belgium (1965-2006)

Source: Sidmar, 1990-2005; ArcelorMittal Ghent, 2006 and Ugine & ALZ, 2005-2006 CONSEQUENCES OF GLOBALISATION FOR THE BELGIAN STEEL INDUSTRYCentralisation of ServicesA major consequence of the evolution of globalisation and mergers is the centralisation of services like purchase and sale of products, research and development, accounting and financing, legal and financial services and information technology. Centralisation of indirect services offers the companies the chance to save costs and to become more competitive. Merging also offers the opportunity to specialise more, to offer a greater spectrum of steel products and to reach a greater market. Purchase and SupplyThanks to centralisation of purchase and supply the steel companies have a strong power while negotiating contracts with clients and suppliers. Before the merger of Arcelor in 2002, the politics of purchase and supply of the group began to grow to an alarming extent. The different companies didn’t have much power to negotiate competitive prices with suppliers and customers. Thanks to centralisation, the group ArcelorMittal can NOW decide on the price when negotiating with the three greatest ore suppliers in the world CVRD, Rio Tinto and BHP Billiton and the ten major automobile producers in the world. After all, the three greatest ore suppliers still cover seventy percent of the world production. Concerning one of the most important customers of the steel industry, the market share of ArcelorMittal in the automobile industry will rise to more than fifty percent in the near future. For the European automobile constructors this isn’t a favourable evolution because of the booming automobile market in Asia. After all, these producers press steel prices even further upwards. Research and DevelopmentFunctioning in a group of enterprises offers the opportunity to combine forces to invest in research and development. After all, research and development is a very expensive matter and for the steel companies it’s advantageous to spread out the costs over various enterprises of the group. An example of this in Belgium is the Ocas, het Onderzoekscentrum voor de Aanwending van Staal. The centre is a joint venture of Arcelor and the region of Flanders. It is situated near ArcelorMittal Ghent. Scientists who work for Ocas continuously invent new steel applications and optimize existing ones every day. In addition, the permanent cooperation with the different customers of the Belgian steel industry, like the automobile industry, is a real strength for the centre. Accounting and FinancingAnother consequence of the merger of Arcelor and ArcelorMittal is the centralisation of the accounting services of the different companies. As expected, this process will continue in the future. A major condition however is to bring the rules, concerning taxes, social matters …, of the different countries of the European Union to the same level. For the Belgian companies of the sector flat carbon steel, including ArcelorMittal Ghent and Arcelor Liège, there is only one bookkeeping department for the different companies. This is possible thanks to the setting up of one great partnership, Arcelor Steel Belgium N.V. All companies of the sector are integrated in this partnership. Earlier on, all the companies set up their own annual statement of accounts and they themselves had contact with the different customers and suppliers. Thanks to the centralisation the bookkeeping services of the smaller companies have been shut down and from now on, these companies only have to focus on their key activities, the production and coating of steel. Only the greater companies still have their accounting departments with employees who care for the bookkeeping of Arcelor Steel Belgium N.V. They handle received and sent invoices, process the general and analytical accounting and prepare the monthly consolidation of ArcelorMittal Ghent and Arcelor Liège. The Belgian companies Ugine & ALZ Belgium and Ugine & ALZ Carinox of the sector stainless steel are part of the coordinating legal entity Ugine & ALZ Belgium NV. With this entity the sector has created one point of address for the different customers. The financial centre of Arcelor is situated at the headquarters of the group in Luxembourg. It is like an internal bank within the group, where all the cash and the financial transactions of the group are managed. An internal system of accounts, intercompany accounts, is used to manage all balances. To administer the risks involved, the group works with internal credit limits. In addition, there is also a central financial service that manages the insurance contracts and covers all the involving risks with great insurance companies. Legal Services, Fiscal Services and Information TechnologyLegal and fiscal services are mostly specific for every country. Therefore Arcelor has offices in each country from which these services operate. These are the satellites, services where jurists and tax specialists are at the service of the different companies of the group. In Belgium the chair of these activities is situated in Brussels. Concerning informatics, Arcelor Technologies is the separate partnership of Arcelor which provides services to the different companies of the group. The employees of the partnership manage the infrastructure of the companies concerning informatics and they design new computer programs. In addition, they buy and maintain the hardware of the different enterprises. Investment DecisionsAnother important consequence of mergers and globalisation is the shift of authority to make investment decisions, from the level of the different steel companies to the level of the group ArcelorMittal. Only the best performing enterprises are granted new investments. The investment expenses of the group ArcelorMittal are divided in different investment classes, in function of the amount of the investment. The different companies themselves only can decide over small investments. For this, each company is assigned an investment envelope every year. The different investment classes (in million USD) are:

For the Belgian steel companies (figure 10), there was a clear decrease of the investments in the year 2002. Partly this was a consequence of the merger of Arcelor because the group reduced the investment projects drastically. In addition the group decided over possible investments in function of the performances of the different companies. In 2005 Arcelor invested 216 million euros in Belgian steel companies. Concerning the whole world the group invested two billion euros in its companies. The investments have different purposes like the improvement of quality, development and adjustment of equipment, the improvement of safety and the protection of the environment. Figure 10. Evolution of the investments of the Belgian steel companies (2000-2005)

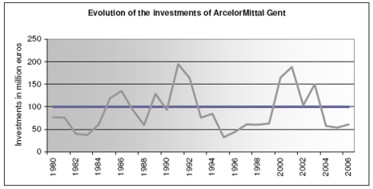

Source: Belgian steel federation, 2000-2005 Concerning ArcelorMittal Ghent (figure 11), the yearly investment budget is on average 100 million euros. So each year about 26 euros per ton shipped product is invested. However this investment budget can fluctuate from year to year, in function of what is necessary for the company. Thanks to this particular investment policy, ArcelorMittal Ghent can maintain its employment level and present very good results in general. Figure 11. Evolution of the investments of ArcelorMittal Ghent (1980-2006)

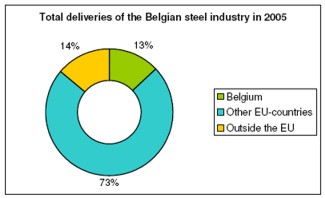

Source: Arcelor Ghent, 2006 Future of Cockerill-SambreAlso very important in the trend of globalisation and mergers is the planned closing down of the warm production phase of Cockerill-Sambre in Liège, which is no longer profitable as a continental business. The great disadvantages of the continental companies are the high transportation costs that result in high production costs and low profitability. Besides the 2,000 jobs of the employees of Cockerill-Sambre, also 5,000 jobs would be gone with the different suppliers of the company. A strategic plan of Arcelor in 2003 announced that the blast-furnaces would have to close in 2006. In 2006 however, it wasn’t very clear if the plan would be brought about thanks to the merger of Arcelor with Mittal Steel. In 2007 ArcelorMittal even announced to reopen this production phase, but the worlwide economic problems of 2008 annulated this intention. STRENGHTS OF THE BELGIAN STEEL INDUSTRYThe Belgian steel companies of ArcelorMittal have many strengths compared to those in other countries and those of other steel groups. Geographical Situation and ExportFirst there is the excellent geographical situation of the companies in the centre of Europe with a well equipped transport infrastructure. Especially the companies situated nearby great waterways which lead to North Sea, like ArcelorMittal Ghent, have a real competitive advantage. These are easy accessible for great sea-going vessels, which offers an opportunity to save costs on transportation of goods. Thanks to the harbors of Antwerp, Ghent and Zeebrugge, the tight road system and the extensive railway- and waterway network Belgium disposes of an efficient distribution network. The advantageous geographical situation in Europe and the excellent transport infrastructure offer the opportunity to develop a strong home market. The Belgian steel industry can exploit its central location in Europe compared to competing steel companies in Asia and South- America. These companies contend with the great disadvantage of enormous transport costs if they want to export their goods to Europe. However, it is very important for the Belgian steel industry to take into account that, in the future, the importance of the geographical situation probably will decrease. After all, other factors, like product quality and production capacity, will become more important in the worldwide competition. In 2005 the Belgian steel industry (figure 12) exported 73% of its products to European customers and 13% was for Belgian companies. Only 14% of the products was exported to countries outside the European Union. Figure 12. Deliveries of the Belgian steel products (2005)

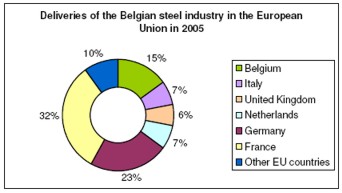

Source: Belgian steel federation, 2005 In particular, the Belgian steel industry (figure 13) exports most of its products to France (32%), Germany (23%) and Italy and the Netherlands (each 7%). Figure 13. Export of the Belgian steel products in the European Union (2005)

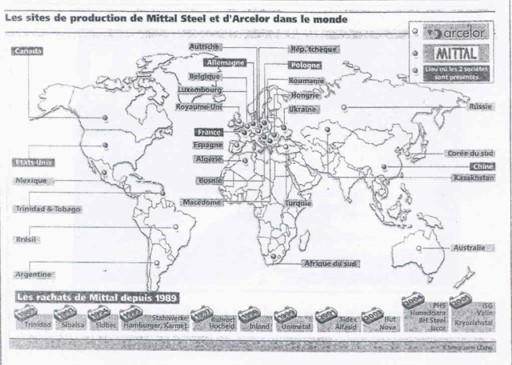

Source: Belgian steel federation, 2005 Since the merger of Arcelor with Mittal Steel there is also a geographical complementation in the group, so the activities of the group don’t overlap. This means that the group can satisfy the needs of international acting clients. The companies of Arcelor are especially active in Western Europe and South-America. Mittal Steel particularly has branches in Central and Eastern Europe, Kazakhstan, North-America, China and India (figure 14). Figure 14. Production locations of Arcelor and Mittal Steel in the world

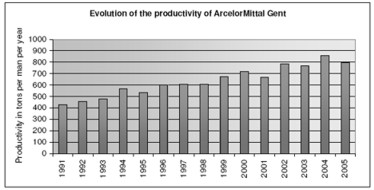

Source: L’echo, 2006 Product Quality and Delivery TermsFurthermore the Belgian companies have an extensive supply of steel products with an exceptional quality and high added value. The Belgian companies dispose of a lot of knowledge and have an edge over their competitors in Asia and South-America concerning scientific research for new steel applications and production methods. The knowledge of the different raw materials and steel properties in the Belgian steel industry is a real strong point for these companies compared to those of other steel companies. The companies have the newest technologies at their disposal and invest a lot of money in research and development. In addition, there are a lot of top scientists who work in specialized centers in the steel industry like Ocas in Ghent. There are also the very competitive delivery terms. These are achieved thanks to projects like On Time In Full (OTIF). Here the companies try to make sure that a big share of the orders are delivered on time. A good planning of the orders is crucial but also the certainty that the equipment doesn’t fall out. ArcelorMittal Ghent, for example, strives for an OTIF score of 95 percent. Labor Productivity, Flexibility and CreativityFurthermore, the very high labor productivity, flexibility and creativity are other real strong points for the Belgian companies in the competition with other steel companies. In general, the productivity of the Belgian employees is very high. The Belgian labor productivity is even one of the highest in the world. This high productivity is a crucial factor for the Belgian steel industry in the worldwide competition. Concerning ArcelorMittal Ghent (figure 15) one can see that productivity has increased from about 400 to 800 tons per man per year, which is a great improvement. As for the other Belgian steel companies, there are a lot of projects to further ameliorate productivity, creativity and flexibility of the employees. The most important thing is to motivate employees to participate in the production process and to give own proposals. Figure 15. Evolution of the productivity for ArcelorMittal Ghent (1991-2005)

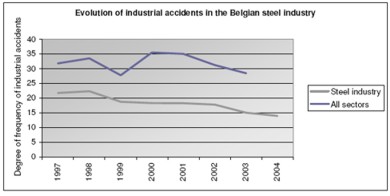

Source: ArcelorMittal Ghent, 2006 Safety and HealthThe group ArcelorMittal also takes care of the human capital of the different companies because it plays a crucial part in growth process of these firms. Therefore, ArcelorMittal feels very strongly about safety on the workplace and the health of the employees. After all, in the steel industry in particular it is very difficult to assure safety in the workplace because there is always a great chance of getting an accident. The Belgian companies present outstanding results concerning safety and absenteeism. Between 1997 and 2003, compared to the safety in all sectors of the Belgian economy, the amount of industrial accidents (figure 16) with Belgian steel producers was remarkably lower. Since 1997 the amount of accidents declined from 22 to 14 accidents per million labor hours. Both companies ArcelorMittal Ghent and Ugine & ALZ Belgium present very good results concerning safety because the amount of accidents declined substantially during the past years. To reach these good figures the group has the project Total Productive Maintenance/Management (TPM). On the basis of this project and the principle of shared vigilance the different companies want to prevent life threatening risks like the danger of falling, electrocution, intoxication and squeezing. The group also has signed the Charter of Safety, by which Agoria and the Belgian steel federation call on to their members to takes measures to ameliorate safety and health. Figure 16. Degree of frequency of industrial accidents for the Belgian steel industry (1997-2004)

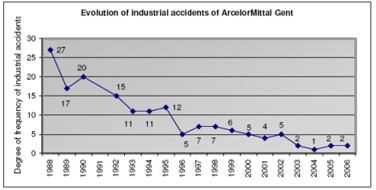

Source: Belgian steel federation, 2004-2006 With ArcelorMittal Ghent (figure 17) the number of accidents declined from 27 in 1988 to 2 accidents per million labor hours in 2006. Figure 17. Degree of frequency of industrial accidents for ArcelorMittal Ghent (1988-2006)

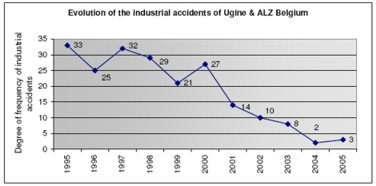

Source: Sidmar, 1990-2005 and ArcelorMittal Ghent, 2006 Ugine & ALZ Belgium (figure 18) was able to diminish the number of industrial accidents from 33 per million labor hours in 1955 to 3 per million labor hours in 2005. Figure 18. Degree of frequency of industrial accidents for Ugine & ALZ Belgium (1955-2005)

Source: Sidmar, 1990-2005 and ArcelorMittal Ghent, 2006 WEAKNESSES OF THE BELGIAN STEEL INDUSTRYNevertheless, there are also some weak points for the Belgian steel producing companies. For steel producing companies, it’s crucial to keep control over costs to stay competitive. However, the Belgian steel industry has three important cost handicaps. After all, the Belgian steel companies contend with problems concerning high labor costs, high costs caused by rigorous environment regulations and high costs of energy. It is common knowledge that the Belgian labor costs are very high, both in international and in European context. In 2006 the taxes and contributions for social security amounted to about 39% of the gross pay. On a worldwide scale only Denmark did worse, with 44% of the gross pay. As a consequence of these high labor costs the companies have to consider moving production to low-cost countries (like NICs, which is harmful for the employees of these firms. However, according to the management of the Belgian steel companies this cost handicap isn’t an insurmountable problem because this disadvantage is partly balanced by the high labor productivity, the exceptional quality, the high level of research and development … In addition, the contribution to social security for shift work and night- and weekend work is reduced since 2004 by the Belgian government.The high costs concerning the environment are caused by the many regional, national and European environment standards. Competitors in Asian and South-American countries have to comply with less or no environment rules. Moreover the Belgian government also appreciates it when the steel companies go a bit further than just comply with the rules. The high energy prices are a consequence of the fact that up to now, the planned liberalisation of the Belgian energy market has not been achieved yet. CONCLUSIONOne can conclude that the Belgian steel producers are a benchmark for certain crucial key performance indicators of the business. In the sector flat carbon steel ArcelorMittal Ghent is the crown jewel of the group ArcelorMittal (L. Mittal, 2007) and concerning the sector stainless steel Ugine & ALZ Belgium NV presents very good results thanks to the cooperation between Ugine & ALZ Belgium in Genk and the Ugine & ALZ Carinox in Charleroi. Altogether, the trend of globalisation offers a lot of opportunities for the Belgian steel companies and these have a lot of strengths to survive in the worldwide steel industry. So, if the management of the Belgian steel companies will continue their efforts, these steel companies will have a future in the worldwide steel business. REFERENCESArcelor, several PPP: Arcelor presentation and Arcelor, the world number one steel manufacturer, 2006. Arcelor Ghent, ArcelorMittal Ghent, 2007, p. 25 (ppt)05) Arcelor annual report 2005, Paris, Labrador, p.3-14, 27-39, 59-72. Belgian steel federation (2000-2004, 2005) Annual reports of the Belgian steel federation, Brussels. BUYST E. (red.) (2002) Sidmar 1962-2002, Veertig jaar staalproductie in

Vlaanderen, Tielt, Publisher Lannoo, p. 12-17, p. 36-37, p. 69-72, p. 97, p. 167-194, p. DE GROOTE P. (2004) Geo-economie, Leuven, University Press Leuven, 436 p. De Tijd (2006) ‘Een verstandshuwelijk bezegeld’, De Tijd, june 27th De Tijd (2006) ‘Overnamebod Arcelor’, De Tijd, june 27th De Tijd (2007) ‘Staalproductie stijgt tot 1,2 miljard ton’, De Tijd, april 14th GENTILE A. (2006) ‘Kokend staal’, Trends, february 23th HEYMANS K. (2007) De Belgische staalindustrie in de ban van de globalisering, thesis UHasselt, -p. Internet: Agoria, consulted on april 7th 2007, www.agoria.be ArcelorMittal Ghent, consulted on august 27th 2006, www.sidmar.be Arcelor, consulted on august 27th 2006, www.arcelor.com ArcelorMittal, consulted on august 27th 2006, www.arcelormittal.com Belgian steel federation, consulted on august 27th 2006, www.steelbel.be FOD Economie, KMO, Middenstand en Energie, consulted on october 7th 2006, http://mineco.fgov.be FOD Buitenlandse Zaken, Buitenlandse Handel en Ontwikkelingssamenwerking, consulted on october 7th 2006, Onderzoekscentrum voor de Aanwending van Staal, consulted on october 14th 2006, www.ocas.be Ugine & ALZ Belgium NV, consulted on august 27th 2006, www.alz.be Site of the prime minister of Belgium, consulted on april 3th 2007, premier.fgov.be Veiligheidscharter, consulted on february 6th 2007, www.veiligheidscharter.be KILLEMAES D. (2007) ‘Nieuwe kostenhandicap voor de industrie, kortsluiting op de elektriciteitsfactuur’, Trends, march 15th. L’echo (2006) ‘Mittal/Arcelor: les numéros un et deux mondiaux de l’acier en chiffres’, L’echo, may 17th . NAERT P. (red.) (2000) Globalisering, zegen en vloek, Tielt, Publisher Lannoo, p. 12-17, p. 97, p. 135-136, p. 167-194. Sidmar, Internal and external communication Sidmar NV (1990-2001, 2002, 2003-4, 2005, 2006), Annual report 1990-2001, 2002, 2003-4, 2005, 2006, Ghent. Sidmar, Internal and external communication Sidmar NV (1997) Sidmar, ARBED Groep, Ghent, B. De Lembre, p. 1-6, 11. Sidmar (2006) ‘Arcelor Mittal, de onbetwiste leider in staal’, Sidmar nieuws, october, p. 5-6 Ugine & ALZ Belgium, Ugine & ALZ Belgium, several PPP: Introduction CAO 2005-2006, april 2005. Ugine Ugine & ALZ Belgium (2005, 2006) Info brochure 2005 and 2006 VAN HORENBEECK E. (2003) Geïntegreerde communicatie. Concern-, interne en marketingcommunicatie, Utrecht, Publisher Lemma, p. 2-5

NOTE* Prof. dr. Patrick De Groote, Universiteit Hasselt, patrick.degroote@uhasselt.be

|

|||||||||