GaWC Research Bulletin 260 |

|

|

|

This Research Bulletin has been published in Regional Studies, 42 (8), (2008), 1113-1131. Please refer to the published version when quoting the paper.

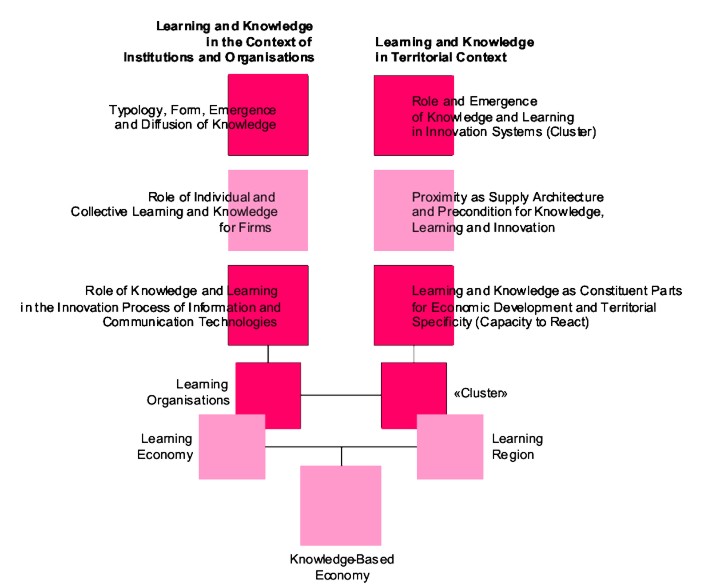

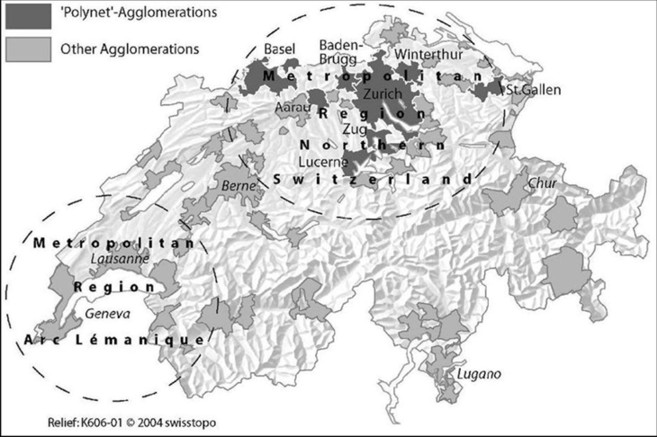

IntroductionThe knowledge economy is undergoing a process of spatial segregation. It tends to build a network of specialised service providers who cover different parts of the value chain. Most corporations build up their location network as a strategic tool to optimise their added value and to compete successfully in the global economy. Such networks can be organised either intra-firm or inter-firm. Intra-firm networks are spatially distributed branches of one individual corporation. The basic premise of these networks are that the more important the office, the greater its flow of information to other office locations (TAYLOR, 2004). Inter-firm networks, on the other hand, are relations between corporations and business clients or suppliers based on contracts, joint ventures or shared projects. We assume that the value added intensive elements of these networks tend to be increasingly anchored within Mega-City Regions due to the quality of infrastructures like airports, higher educational institutions, research facilities or large settlements of leading global companies, as well as the availability of specific knowledge (THIERSTEIN et al., 2006). Both, intra-firm networks and inter-firm networks are important in analysing the patterns of the changing value chain of the knowledge economy, because they illustrate the spatial division of labour and determine the degree of internationalisation of Mega-City Regions. Manuel Castells' Network Society is one of the most influential works for world city studies today. His thoughts have stimulated a new perception of spatial and urban development. He argues that our societies are constructed around flows: flows of capital, flows of information, flows of technology, flows of organizational interactions, flows of images, sounds and symbols (CASTELLS, 1996:412). Thus, he proposes the idea that there is a new spatial form characteristic of social practices that dominate and shape the network society. He calls it the space of flows (CASTELLS, 1996:412). Spaces of flows play a key role in the scientific discussion about Mega-City-Regions, which can be defined as clusters of towns and cities that are increasingly interconnected across geographical space through travel and non-physical communication (HALL and PAIN, 2006:4). An important driving force in Manuel Castells' space of flows is the knowledge economy. It can be defined as that part of the economy which requires high-skilled workers and a substantial proportion of research activities. Advanced Producer Services (APS) firms are important actors within the knowledge economy showing increasing employment rates (THIERSTEIN et al., 2006:40). In this paper, the term APS firm refers to the following business lines: accountancy, advertising, banking/finance, design, insurance, ICT consultancy, law, third-party and fourth-party logistics and management consultancy. Over recent decades, Switzerland has experienced the reorganisation of functional-territorial division of labour in the knowledge economy. The opportunity for flexible spatial organisation of company locations has influenced business strategies and location decision making. The workforce is becoming more mobile, which results in increasing numbers of commuters, increasing commuting distances and growing built-up areas in the outer belts of the agglomeration leading to urban sprawl and hybrid landscapes. Bordering along historical urban cores, a patchwork of urban and rural areas has been formed, evolving into a new kind of urbanised landscape. The growing relevance of the knowledge economy is a driving force slowly altering regional development and spatial functional specialisation. Their impact often goes beyond the official spatial development policies of the government system (OECD, 2002). Swiss spatial planning guidelines still struggle to acknowledge the existence of a functional spatial level. Obviously, there is a mismatch between the objectives and strategies for sustainable spatial development, and actual development tendencies. Whereas planning principles are based on a normative, territorial logic, actual spatial development follows a functional logic, largely driven by market forces (GABI et al., 2006:168). A similar situation can be observed within the European policy discussion, which is faced with an overarching dilemma between territorial cohesion and economic competitiveness. On the one hand, the Lisbon Agenda, adopted by the European Council, seeks to make Europe the world's most competitive and dynamic knowledge economy by the year 2010 (EUROPEAN COUNCIL, 2000). By stressing the development of the knowledge economy and its innovation processes, it reflects the current scientific understanding of contemporary global economic changes. On the other hand, there is the European Spatial Development Perspective (ESDP) and the later Gothenburg Agenda, which promotes a more balanced and sustainable pattern of urban development across Europe, reducing the weight of the central urban zone of North West Europe (the London-Paris-Milan-Munich-Hamburg-Pentagon) (EUROPEAN COMMISSION, 1999). The focus is on the paradigm of balanced territorial development to be promoted through polycentricity, largely based on a morphological view of spatial development. Unfortunately, the urban functional complementarities within and between Mega-City Regions are not recognised. Territorial cohesion, as proposed in the ESDP, might well suggest promoting growth in lagging areas, even at the expense of the most dynamic and competitive regions (HALBERT et al., 2006:207). An Informal Ministerial conference was held in Leipzig on 24 and 25 May 2007 within the framework of the German EU (European Union) Council Presidency. On the occasion of this conference, ministers responsible for Spatial Development in EU Member States agreed on the "Territorial Agenda of the European Union". It supports the implementation of both the Lisbon and the Gothenburg Strategies through an integrated territorial development policy (EU, 2007). Unfortunately, the Territorial Agenda hardly addresses the importance of the knowledge economy and the functional division of knowledge-intensive businesses in a spatial perspective. Prior to the launch of new political strategies boosting polycentric spatial development, there is a need for a deeper understanding of the interrelationships between polycentric spatial development and economic competitiveness. Economic competitiveness is strongly related to innovative enterprises and their performance, especially Advanced Producer Services (APS). The key aim of this paper is therefore to empirically investigate the functional polycentric patterns and interlocking networks of APS firms. In the form of a case study, we analyse the physical and non-physical functional connectivity of APS firms in the emerging Mega-City Region of Northern Switzerland on different geographical scales. By analysing the changing value chains of APS firms, we show the functional logic of actual territorial development. In doing so, we refer to the analysis of data from the Swiss Federal Statistical Office (NOGA statistics) and the results of empirical analysis of the INTERREG IIIB research project POLYNET (HALL and PAIN, 2006; THIERSTEIN et al., 2006). Three main aspects will be investigated empirically: first, the structure and dynamics of the knowledge economy; second, the spatial patterns of intra-firm networks on an international, national and regional scale; third, the spatial patterns of inter-firm networks within the emerging Mega-City Region of Northern Switzerland. These analytical findings will be related to the theoretical debate in regional sciences and to the concept of polycentric regional development. The paper is structured in four main sections: The first section focuses on the knowledge economy and its impacts on spatial development. We introduce knowledge and learning within an institutional as well as within a territorial context. The next section picks up the concept of Mega-City Regions by discussing associated theoretical approaches, and clarifies the definition used in the POLYNET study. Afterwards, we will introduce our understanding of Mega-City Regions as results of spatial systems of value chains. The third section combines the two foregoing streams of reasoning by analysing the knowledge economy in the emerging Mega-City Region of Northern Switzerland. This will be done in three parts: In the first parts, we define the study area in which we analyse functional polycentricity and economic interrelations. In the second part, we show the changing structure of the knowledge economy by focusing on sectoral patterns of structural change in order to show the different development processes of knowledge-intensive activities. In the third part, the paper presents the results of the empirical analysis of the intra-firm and inter-firm connectivity of Advanced Producer Services and shows the polycentric interlocking network between the different firms and institutions of the knowledge-economy throughout the value chain. In the fourth and final section we conclude by discussing the intricacies of morphological and functional polycentricity in the emerging Mega-City Region of Northern Switzerland. The Knowledge Economy and Spatial DevelopmentThe focal point of the knowledge economy is the concept of knowledge. Following Michael Polanyi knowledge can be divided into two major categories: codified and tacit knowledge (POLANYI, 1967). Codified knowledge can be applied, expressed and standardised. Hence, it is a marketable good which can easily be distributed over time and space. Tacit knowledge, in contrast, refers to knowledge which cannot be easily transferred. It comprises skills based on interactions and experiences. Since the transfer of tacit knowledge requires direct face-to-face interactions, the finding of POLANYI (1967) is of great importance for regional science. It raises the question of accessibility and spatial proximity in the context of the knowledge economy. The spatial characteristics of knowledge economies can be seen through the history of regional sciences and the analysis of regional economic literature. The following section gives a brief overview of the scientific debate about the knowledge economy by discussing the understanding of knowledge in regional and evolutionary economics. The first early theories on innovation and regional development are strongly inspired by Joseph Schumpeter who focuses initially on the roles of entrepreneurs and their small companies in recognising the importance of particular inventions and assembling the resources needed to turn them into marketable products (SIMMIE, 2005:790). While these initial explanations of innovation were being developed, other economists were seeking to explain the advantage of spatial concentration in terms of external economies, which include pools of common factors of production such as land, labour, capital, energy and transportation (SIMMIE, 2005:791). These two separate lines of theoretical analysis were brought together by François Perroux in Europe and Edgar M. Hoover as well as Raymond Vernon in the USA (HOOVER and VERNON, 1959; PERROUX, 1952; VERNON, 1966). These authors developed explanations of growth poles and the relationships between new product life cycles and agglomeration theory. Assigned to regional development, the concept of product life cycles attests that a region is strongly influenced by a certain line of business. In contrast to the product life cycle theory, a second broad theoretical approach was developed in the 1980s to explain why local space was still important for newly developing forms of production. Much of this work was inspired by Piore and Sabel's concept of flexible specialisation that identified the breakdown and deverticalisation of large firms as a key characteristic in modern economies (PIORE and SABLE, 1984). In the face of international competition and changing customer demands, this process is driven by the need for firms to be both more specialised and more flexible in the ways in which they organise their production. The result is a networked form of production that leads to a reconnection of economic activities to local space because of the need for proximity between the numerous specialists involved in any given value chain (SIMMIE, 2005:799). The flexible specialisation thesis inspired several new concepts dealing with innovation, knowledge and regional development. Influential among these were the innovative milieux approach, the industrial districts and the new industrial spaces. In the theory of the milieux innovateurs developed by the GREMI (Groupe de Recherche Européen sur les Milieux Innovateurs), firms are seen as part of a milieu with an innovative capacity. In the current research agenda, the GREMI stresses the importance of learning, which enables firms to perceive changes in their environment and helps them to adapt their behaviour accordingly (MOULAERT and SEKIA, 2003:291). The theory of the new industrial district, on the other hand, emphasises the innovative capacity of small and medium sized enterprises (SMEs) which belong to the same industry and local space. Commonly, industrial districts are defined as localised production systems, based on a strong local division of labour between small specialised firms which are integrated in the production and value chain of an industrial sector. Newer approaches, however, highlight that such networks also connect large firms and their suppliers and enable the introduction of flexible specialisation by facilitating subcontracting. As a consequence, the manufacturing depth of large companies is reduced and a smooth diffusion of innovation throughout the whole regional economy is facilitated (GRABHER, 1991). The recognition that knowledge creation and diffusion is a process happening within the value chain of firms is of great importance for the empirical concept presented in this paper. Michael Storper and Richard Walker as well as Allen J. Scott finally launched the notion of new industrial spaces by combining insights from different literature such as industrial districts, flexible production systems, economies of agglomeration and others (SCOTT, 1985; STORPER and WALKER, 1988). The authors argue that in flexible production systems, the tendency to agglomeration was reinforced not only by externalisation but also by intensified re-transacting, just-in-time processing, variable forms of inter-unit transacting and the proliferation of many small-scale linkages with low unit costs. Scott argues that the economic process of vertical disintegration into extended and specialised divisions of labour is leading to spatial forces that encourage small firms to concentrate in space (SCOTT, 1985). The reasons for the increasing development of networks are seen as a response to the increasing uncertainty and instability of production and markets. Further interesting empirical evidence about the interrelationship between innovation and space is provided by several papers of James Simmie (SIMMIE, 2004; SIMMIE et al., 2002). By analysing the results of comparable surveys of innovative firms in Amsterdam, London, Milan, Paris and Stuttgart, SIMMIE et al. (2002) find evidence that, even among the most innovative European cities, there are significant differences in the ways in which their regional innovation systems are structured. The authors find that in regional cities such as Stuttgart and Milan, innovative activities are more closely linked to their regional and national economies than they are in the international world cities such as Paris and London. SIMMIE et al. (2002) present evidence that there is some justification in the case of Milan and Stuttgart for the view that local factors such as suppliers, education and technology transfer institutions do play an important part in the innovation system of those city regions. In these cases, geographic proximity of the various elements of the value chains seems to be a main reason for the concentration of innovations. Nevertheless, good local factor conditions also mean that innovative firms can take advantage of both geographic and time proximity to suppliers. SIMMIE et al. (2002) argue that the latter is a particular advantage for international cities as it brings a huge range and variety of possible suppliers within the reach of innovative firms located in them. SIMMIE (2004) uses evidence from the third Community Innovation Survey to test the interrelationship between innovation and space in the UK. Most evidence presented in his paper suggests that innovation performance in the UK is not dependent on localised cluster dynamics but on international links and networks. SIMMIE (2004) argues that part of the reason for this is the continued importance of multinational corporations whose spatial division of labour reinforces national and international urban hierarchies. Hence, many places remain part of the internationally distributed value chains of multinational corporations. SIMMIE (2004) suggests that the analysis of clusters should not start with their geography, but with the links between firms and institutions. This is exactly the approach adopted in this paper with respect to intra-firm and inter-firm networks of Advanced Producer Services firms. Since the objective of our study is to identify the functional space of economic interrelations, we seek to approximate the emerging Mega-City Region of Northern Switzerland by analysing the spatial patterns of intra-firm and inter-firm networks. These economic interrelations are investigated on a regional, national, European and global geographical scale. Figure 1 shows an overview of the scientific debate about knowledge and learning within an institutional and territorial context. As can be seen on the left hand side of figure 1, knowledge-intensive learning and development processes within institutions and firms lead to the fact that many knowledge intensive enterprises expand their core competencies in order to maintain or even strengthen their market position. Such activities within corporations result in learning organisations and finally in learning economies. The right hand side of figure 1 indicates that the spatial concentration of knowledge and learning leads to a territorial specificity of learning regions. STORPER (1997) underlines this aspect in the following way: Those firms, sectors, regions, and nations which can learn faster or better ( ) become competitive because their knowledge is scarce and therefore cannot be immediately imitated by new entrants or transferred, via codified and formal channels, to competitor firms, regions or nations (STORPER, 1997:31). The starting point of this paper is the assumption that the choice of location of institutions and organisations is not a coincidence but, to a greater or lesser extent, a strategic decision. Most corporations design their network of branches and locations as a strategic tool to optimise their added value and to compete successfully in the international economy. This means that learning and knowledge in the context of institutions and organisations is reflected in a territorial context. Changing configurations of such territorialised intra-firm networks of locations in turn affect urban hierarchies and contribute to the emergence of Mega-City Regions. For the purpose of this paper, the link between the institutional and the territorial context of knowledge and learning is of great importance. The increasing relevance of the knowledge economy as driver of socio-economic development becomes clear in the interplay of organisational knowledge and the concentration of collective competencies in Mega-City Regions. MALECKI (2000) describes this aspect as the local nature of knowledge and highlights the necessity to accept knowledge as a spatial factor of competition: If knowledge is not found everywhere, then where it is located becomes a particularly significant issue. While codified knowledge is easily replicated, assembled and aggregated ( ), other knowledge is dependent on context and is difficult to communicate to others. Tacit knowledge is localised in particular places and contexts ( ) (MALECKI, 2000:110). The Emergence of Mega-City RegionsTheoretical BackgroundThe concept of the polycentric Mega-City Region combines different theoretical approaches: John Friedmann's world cities, Saskia Sassen's global cities, Peter Taylor's world city network and Manuel Castells' spaces of flows. In the following part, the main ideas behind these theories will be explained. John Friedmann's world city concept describes the rise of a transnational urban network referring to a major geographical transformation of the capitalist world economy whose production systems are increasingly internationalised. This reconfiguration results in a new international division of labour whose main agents are multinational enterprises with complex spatial organisational structures. It is the presence of these multinational enterprises that makes world cities into geographical places of great economic power. Furthermore, Friedmann argues that the territorial basis of world cities comprises not only the central city, but also the whole economic space of the surrounding region. Therefore, world cities are often polycentric urban regions containing a number of historically distinct cities that are located in more or less close proximity (FRIEDMANN, 1986). In contrast to John Friedmann's world city concept, Saskia Sassen's global city approach discovers a new geography of centrality in which the city centres or the central business districts form the heart of the global urban network. The functional centrality of these global cities leads to an increasing disconnection of the city centres from their broader hinterlands or adjacent metropolitan region. The reason for this disconnecting process lies, according to Sassen, in the location strategies of Advanced Producer Services firms as spearheads of the rising global knowledge economy. These enterprises are increasingly located just within the city centres of economic regions and connect these places directly with other city centres in the world (SASSEN, 2001:21). The fundamental differences between John Friedmann's world cities and Saskia Sassen's global cities are well described by DERUDDER 2006): Sassen's focus on centrality leads her to conceptualising global cities' as focal points that operate separately from their hinterlands. Friedmann's focus on the relative concentration of power, in contrast, implies that a world city' may consist of multiple cities and their hinterlands that may themselves be subject to urbanisation processes (DERUDDER, 2006:2034). Peter Taylor's notion of world city networks analyses inter-city relations in terms of the organisational structure of the global economy and views world cities as global service centres' connected into a single worldwide network (TAYLOR, 2004). The Globalisation and World Cities Study Group (GaWC) at Loughborough University analyses the inter-city relations using a specific methodology, in which relationships between cities are not measured directly. Instead, the method uses a proxy by analysing the internal structures of large APS firms and revealing the relationships between head offices and other branches located all over the world. In doing so, world cities are not defined by their functions, but in terms of their external information exchange (HALL and PAIN, 2006:9). The last theoretical approach underlying our study is Manuel Castells' highly influential concept of a space of flows (CASTELLS, 1996). As mentioned in the introduction of this paper, he argues that the new spatial logic is determined by the pre-eminence of the space of flows over the space of places. By space of flows he refers to the system of exchange of information, capital and power that structures the basic processes of societies, economies and states between different localities, regardless of localisation. The INTERREG IIIB Study Project POLYNET Sustainable Management of European polycentric Mega-City Regions is one of the most recent research activities about the emerging of polycentric Mega-City Regions (HALL and PAIN, 2006). Peter Hall and Kathy Pain define Mega-City Regions as follows: Mega-City Regions are a series of anything between 10 and 50 cities and towns physically separate but functionally networked, clustered around one or more larger central cities, and drawing enormous economic strength from a new functional division of labour. These places exist both as separate entities, in which residents work locally and most workers are local residents, and as parts of a wider functional urban region connected by dense flows of people and information carried along motorways, high-speed rail lines and telecommunication cables (HALL and PAIN, 2006:3). Based on this definition, POLYNET hypothesises that [Mega-City Regions] are becoming more [polycentric] over time, as an increasing share of population and employment locates outside the largest central city or cities, and as other smaller cities and towns become increasingly networked with each other, exchanging information which bypasses the large central city altogether (HALL and PAIN, 2006:3). The POLYNET project was aimed at investigating the polycentricity of Mega-City Regions and its current state of functional division of labour. For that, the methodology of the Globalisation and World Cities Study Group was adapted to the new phenomenon of Mega-City Regions. Instead of analysing the world city network, the focus was on inter-city relations in terms of the organisational structure of the global economy (TAYLOR, 2004). Starting from a fundamental criticism of previous urban research that focused on attributes of urban areas or places mostly in a national context, the relationships between the cities should be measured on the basis of flows taking a global perspective (HALL and PAIN, 2006). As a consequence, Mega-City Regions have been defined in terms of their internal linkages between different cities and towns as well as analysed on an international, national and regional scale. When analysing polycentric Mega-City Regions, one has to distinguish between a morphological and a relational view (ESPON, 2004): the morphological view lays out the distribution of urban areas in a given territory by studying the distribution of locations, the number of cities and their hierarchy. The relational view, in contrast, is based on networks of flows and cooperation between urban areas on different spatial scales. ESPON (2004) recognises that there are inherent difficulties embedded in the concept of polycentricity, as contradictions exist between different geographical levels. On the European scale, ESPON (2004) shows that regional polycentric integration will tend to increase the contrast between core and periphery. On the national scale, a policy for increased spatial balance at the European level will lead to a concentration of investments in urban areas strengthening these regions at the expense of other more peripheral regions. On the city scale, finally, there is no observable correlation between the levels of polycentricity and their capacity to integrate in polycentric networks on the European or national scale (ESPON, 2004). To sum up, it is important to recognise that spatial processes at the European level can have opposing consequences on the national or even city scale. Therefore, it is important to think simultaneously on different geographical scales. Furthermore, it is important to analyse not only the morphological and visible aspects of polycentricity, but also the relational and hidden polycentric structures of Mega-City Regions. For this, the POLYNET project introduced a new way of looking at these spatial phenomena, analysing non-physical connectivity by intra-firm networks in order to define the realm of APS networks at different geographical scales. The Swiss case study for the POLYNET project extended this analysis by looking also into inter-firm networks of APS firms. By doing so, we understand Mega-City Regions as spatial systems of socio-economic added value, which interconnect different value chains. Mega-City Regions as Systems of Spatial Value ChainsThe knowledge economy is undergoing a process of differentiation and spatial segregation leading to a constant rearrangement of the value chain of knowledge intensive businesses. The analysis of changing value chains as a consequence of the dynamic restructuring of companies in capitalist economies is strongly influenced by Piore and Sable, who identified the breakdown and deverticalisation of large firms as a key characteristic in modern economies (PIORE and SABLE, 1984). According to Saskia Sassen, the location strategies of Advanced Producer Services (APS) firms play an increasing role in the system of spatial value chains (SASSEN, 2001). These APS firms tend to have their knowledge-rich head offices in core metropolitan regions that act as nodal points within an international network of cities. Like many pharmaceutical industries in the mid 1990s, APS firms are experiencing a similar segmentation of their value chain. This leads to the emergence on the market of new institutions from different areas of Advanced Producer Services such as hedge funds, venture capital, the financial arms of large production companies as well as specialised information technology corporations and specialised consultancies. Additionally, rapid changes in communication infrastructure, computer capacities, data storage and collaborative models and platforms will drive more structural changes by enabling outsourcing across the value chain. When looking at the value creation process of knowledge it becomes obvious that these processes follow a functional and networked logic of independent as well as interdependent institutions throughout the value chain. These processes are not necessarily bound by the limitations of territorial borders. To the extent that business is not concerned by limiting regulations, the knowledge economy tends to build a network of specialised service providers who cover the different parts of the value chain, which means that the spatial organisation of the knowledge-intensive economy follows its inherent functional logic. Globalisation leads to increasing competition in the world economy and forces knowledge intensive firms to constantly innovate and improve their added value. This is reflected in the spatial organisation of their branches and cooperation partners. For Switzerland DÜMMLER et al. (2004) show that branches with senior management functions are mostly located in the cores of international cities such as Zurich and Basel, where they find a direct neighbourhood of head offices of competitor or partner firms. Branches with R&D functions are located in places with high densities of potential partners and competitors too, for example the high-tech industry in the Jura region. Branches with distributive functions are located close to the customers or in places with low costs and well developed traffic access, such as many smaller agglomerations in Switzerland 's Central Plateau (DÜMMLER et al., 2004). Spatial concentration processes are not a coincidence, but the result of firms strategically choosing their locations. In order to improve their added value, knowledge-intensive firms need several local business conditions such as proximity to global infrastructures like airports and universities, the presence of competitors, business partners and customers as well as qualified manpower. In a similar way, PORTER (1998) argues that the enduring competitive advantage in a global economy are often heavily local, arising from concentrations of highly specialized skills and knowledge, institutions, rivals, related business, and sophisticated customers. Geographic, cultural, and institutional proximity leads to special access, closer relationships, better information, powerful incentives, and other advantages in productivity and innovation that are difficult to tap from a distance (PORTER, 1998:90). Thus, there is a growing concentration of knowledge-intensive firms in Mega-City Regions, where these conditions are met. Starting from these findings, we propose that there is an emerging Mega-City Region of Northern Switzerland with the two main centres Zurich and Basel. Because of the various requirements for competing in the world economy, it is not possible for Zurich, although the biggest agglomeration in Switzerland, to act without the smaller agglomerations in its proximity. In the context of Mega-City Regions, smaller cities fulfil an important role as complementary economic spaces. Interlocking networks of knowledge-intensive firms multi-city and multi-branch intra-firm as well as inter-firm value chain connectivities link these different agglomerations together, thus defining the functional Mega-City Region of Northern Switzerland. Knowledge Economy in the Emerging Mega-City Region of Northern SwitzerlandDefinition of the Study AreaThe spatial expansion of economic networks over recent decades led to the emergence of two Mega-City Regions in Switzerland (THIERSTEIN et al., 2006). It is important to recognise that the emerging Mega-City Region of Northern Switzerland is not a clearly defined region but a spatial concept approximating to a functional space of economic interrelations. Our study is an explicitly explorative project touching a field, which has hardly been explored in Switzerland. Firstly, we look at spatial development from a functional point of view and reveal the driving forces of large-scale spatial patterns. Secondly, we move beyond the usual perimeters of spatial analysis. Therefore, our study is freed from determining institutional borders and approaches the real' economic functions. However, for the quantitative analysis, it was necessary to decide on a working definition that delimits the emerging Mega-City Region of Northern Switzerland in a more pragmatic way. For this study, the methodology of BEHRENDT and KRUSE (2001) has been used as an initial delimitation of the emerging Mega-City Region of Northern Switzerland, calculating the area that can theoretically be reached within a one-hour car journey from the airport of Zurich (see Figure 2) (BEHRENDT and KRUSE, 2001). It is based on the GEMACA (Group for European Metropolitan Areas Comparative Analysis) approach using commuter data as a functional criterion for the delimitation of metropolitan areas (GEMACA, 1996). Within this area, the eight agglomerations with the largest shares of APS multi-branch firms have been chosen for the purpose of our analysis: Basel, Aarau, Baden-Brugg, Lucerne, Zug, Zurich, Winterthur and St. Gallen. These agglomerations will be referred to below as FURs (functional urban regions), whereas the designations FUR and agglomeration are used synonymously. As we will see in the following sections, the analysed FURs are linked together by spatial patterns of interlocking networks of APS firms, thus providing evidence for the emerging Mega-City Region of Northern Switzerland. Figure 2 gives an overview of the agglomerations that have been analysed in our study. Apart from the Mega-City Region of Northern Switzerland, it is assumed that there is a second emerging Mega-City Region in the French speaking part of Switzerland, the so-called Arc Lémanique (COMTESSE and VAN DER POEL, 2006). The Changing Landscape of the Knowledge Economy in the Emerging Mega-City Region of Northern SwitzerlandWithin the emerging Mega-City Region of Northern Switzerland, the knowledge economy is facing a pronounced structural change due to the reorganisation of its value chain, the emergence of new market players and the outsourcing tendency within the financial as well as the services industry. This has implications on the spatial division of labour respectively on the spatial organisation of the value chains of firms and affects the national as well as the international connectivity of the emerging Mega-City Region of Northern Switzerland. In the following section, we would like to show these processes by emphasising changes in the employment and location structure of the financial services industry and the knowledge-intensive business services within Switzerland and in the emerging Mega-City Region of Northern Switzerland. Table 1 gives an overview of total employment within different sectors of knowledge-intensive industries in Switzerland and compares its dynamics with the emerging Mega-City Region of Northern Switzerland. 2001 is the year of the most recent employment data on a micro-branch level. The next business census in late 2005 will not be ready for use until late 2007 on such a disaggregated branch level, enabling the recomposition of the APS sectors of the knowledge economy. The table reveals the absolute and relative importance of two basic aspects of the knowledge economy. Firstly, according to the calculation, one out of six work places can be found within the defined knowledge-intensive economy. More than 68 percent of these jobs are incorporated within financial and related services, and the knowledge intensive services industry itself. With an overall employment growth of 18.7 percent, compared with 3.8 percent for total employment in Switzerland, these sectors can be seen as the main drivers of the Swiss economy. These figures clearly underline the growing importance of knowledge and innovation within the Swiss economy. Secondly, the employment figures reveal the importance of the emerging Mega-City Region of Northern Switzerland for the Swiss economy as more than 60 percent of total employees in the Swiss knowledge economy work in this geographical area. Table 2 lists location and employment data at the Swiss national level and takes a closer look at those sectors with the highest structural change in Switzerland. They are important elements of the Swiss financial industry and a crucial subset of Advanced Producer Services (APS) firms. The classification is based on the official NOGA statistics of the Swiss Federal Statistical Office:

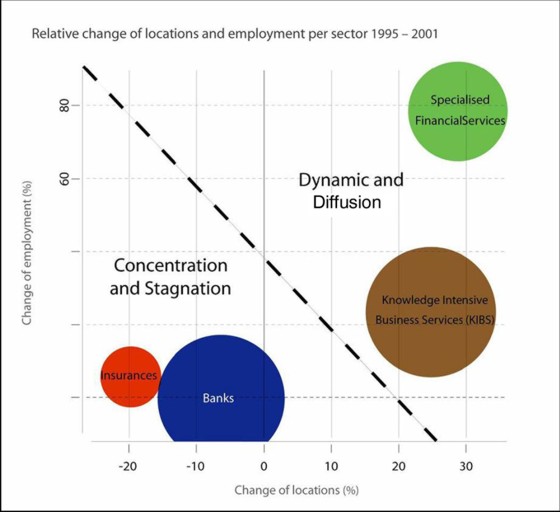

Employment figures are important economic indicators because they show those areas needing increased human capital in order to build a market position. However, this must be differentiated in detail, because the intensity of added value is not necessarily linked to high employment figures. At first glance, table 2 reveals two different types of structural change. Firstly, banks and insurance companies show clear signs of concentration. In general, both sectors have shifted their locations. Insurance companies decreased their number of locations by about 14 percent. The decrease within the banking sector is slightly less, and is due in particular to relocation strategies in Retail Banking. Note that the aggregate employment figure in the banking sector has remained stable. However, within the banking sector, a constant and intensive decrease in employment, notably within the major banks, has been compensated for by an increase in employment mainly in regional banks, private banks and stock exchange banks. This does not necessarily mean that employees have moved from one bank to another. Many of the employees entered the sector of specialised financial services, such as independent asset management or the field of alternative assets such as hedge funds, venture capital, private equity and others. Secondly, the specialised financial services and Knowledge Intensive Business Services (KIBS) sector experienced exactly the opposite development. With a growth rate of about 35 percent for locations and 85 percent for employment, specialised financial services show the greatest alteration. In 1995, absolute employment figures were almost three times lower than in the banking sector. In 2001, this difference has been reduced to about 1.5 times. Looking at the total number of locations and the geographical distribution in Switzerland, it may be observed that these two sectors are ideally located in agglomerations close to cities like Zurich, Zug, Basel, Geneva or St. Gallen. But with on average 6.5 employees per location, compared to 29.17 employees in the banking sector, the specialised financial services sector seems to be smaller and probably more specialised than the banking sector. Figure 3 provides another perspective on the structural change described above. It shows the relative change in locations and employment for each sector and visualises two forms of structural change. On the one hand, banks and insurance companies are characterised by spatial concentration and stagnation because of rather low changes in employment and locations. On the other hand, specialised financial services and Knowledge Intensive Business Services (KIBS) are characterised by dynamic employment and diffusion processes due to their relatively high change of employment and workplaces. In conclusion, there are four important key messages which emphasise the changing value chain of the knowledge economy in the emerging Mega-City Region of Northern Switzerland.

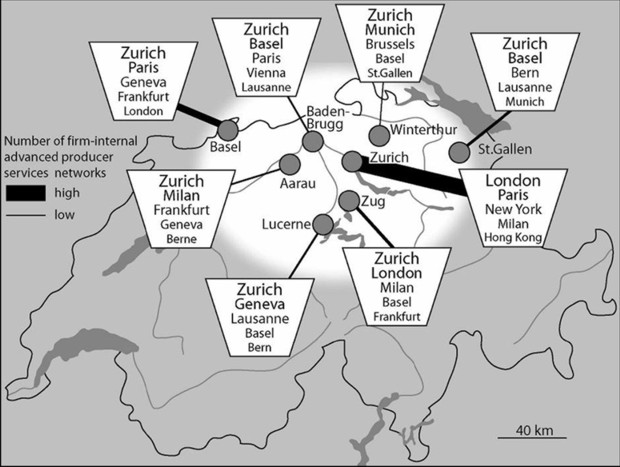

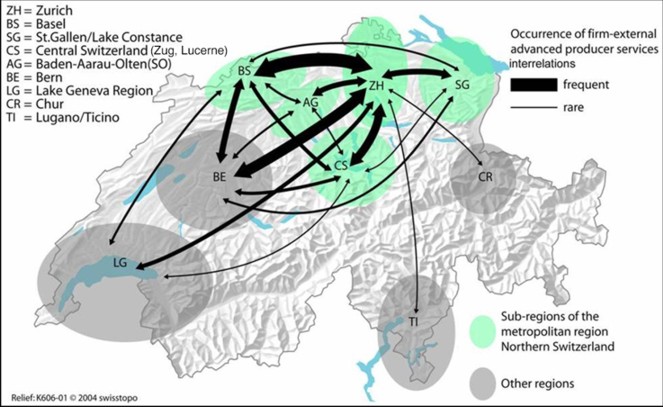

The changing structure of the knowledge economy described in this section has a major impact on the spatial patterns of knowledge networks in the emerging Mega-City Region of Northern Switzerland. Because of the highly connected economic activities within the value chain of the knowledge economy, knowledge-intensive service firms clearly show evidence of a polycentric and functionally structured division of labour within the emerging Mega-City Region of Northern Switzerland. These value chains will be analysed in greater detail in the following section. Networks of Knowledge in the Emerging Mega-City Region of Northern SwitzerlandThe emerging Mega-City Region of Northern Switzerland can be regarded as a functional region, where sub-centres have different functional and hierarchical roles. The two largest economic centres, Zurich and Basel, are at the top of this functional hierarchy, providing favourable location conditions for knowledge-intensive services. Interviews that were conducted during the POLYNET case study clearly indicate that in these two agglomerations, knowledge-intensive firms find the best conditions for direct international knowledge exchange (THIERSTEIN et al., 2006). However, the agglomerations of Zurich, with about one million inhabitants, and Basel, with about 500,000 inhabitants, are both too small to concentrate all major functions of the metropolitan region in their own location. It is an important characteristic of the emerging Mega-City Region of Northern Switzerland that many of the important functions are distributed throughout a polycentric network of the two core cities of Zurich and Basel as well as the sub-centres Zug, Lucerne, Winterthur, St. Gallen, Aarau and Baden-Brugg. As will be shown further down, there is a dense interlocking network between the different institutions and firms of the knowledge economy in these locations throughout the value chain. It is the complementary combination of Zurich and Basel, together with supplemental centres, which raises the emerging Mega-City Region of Northern Switzerland to a competitive level in the context of the global economy. In the following sections we first present the results of the empirical analysis of both the intra-firm and inter-firm connectivities of Advanced Producer Services firms. Secondly, we show on the basis of a stylised value chain the polycentric interlocking network between the different firms and institutions of the knowledge economy. Spatial Patterns of Intra-firm Networks The analysis of intra-firm networks is based on the methodology of the Globalisation and World Cities Study Group (GaWC) at Loughborough University. This approach estimates city connectivities from the office networks of multi-city Advanced Producer Services firms. These services are described as advanced because they sell high value information and knowledge (TAYLOR and EVANS, 2005:3). The basic premise of this method is that the more important the office, the greater its flow of information to other office locations. The following lines of business have been analysed in our research project: accountancy, advertising, banking/finance, design, insurance, ICT consultancy, law, third-party and fourth-party logistics and management consultancy. In the first stage of our empirical work, we had to create a reliable company database. In identifying Advanced Producer Services firms within the emerging Mega-City Region of Northern Switzerland, the basic data set from the Swissguide database has been used. The firms are allocated to the sectors using its NACE codes (Nomenclature générale des activités économiques). Afterwards, records without websites or less than five employees have been removed from the database prior to detailed data analysis. The result was a basic set of over 12,500 company entries distributed among the nine business sectors and eight FURs. Then, we had to filter out firms that are only active on a purely local basis, meaning that companies whose action radius is almost exclusively focused on their own location or neighbouring municipalities had to be eliminated from the database. Table 3 shows the business inventory used for the calculation of the city connectivity. Having compiled the database of Advanced Producer Services firms, we used an interlocking network analysis to estimate connectivities of FURs within and beyond the Mega-City Region of Northern Switzerland (TAYLOR, 2004). To carry out an interlocking network analysis requires the construction of a so called service activity matrix, defined by n FURs and m service firms. Each cell in the matrix is a service value (vij) that indicates the importance of FUR i to firm j. The importance is defined by the size of an office location and its function. By analysing the firms' websites, all office locations are rated at a scale of 0 to 3. In a first step, the connectivity between two FURs (a, b) of a certain firm (j) is analysed by multiplying their service values (v). In this respect, the following equation represents the so called elemental interlock between two FURs for one firm. rabj = v aj * v bj (1) To calculate the total connectivity between two FURs, one has to summarise the elemental interlock for all firms located in these two FURs. This leads us to what is known as the city interlock (rab). rab = ∑ rabj (2) Aggregating the city interlocks for a single FUR produces the interlock connectivity (Na). This describes the overall importance of a FUR within a network. Na = ∑ rai (a≠i) (3) If we relate the interlock connectivity for a given FUR to the FUR with the highest interlock connectivity (Nh), we gain an idea of its relative importance in respect to the other FURs that have been considered. The resulting values of relative connectivity score somewhere between 0 and 1. Pa = (Na/Nh) (4) In addition to the quantitative network analysis, we have conducted several in-depth face-to-face interviews with senior business practitioners and organisations. The interview method provides qualitative evidence complementing quantitative data gathered by the other empirical research actions. This has produced an extensive and rich data source on the actual changes and issues relevant to the study that could not be elicited by alternative means. Therefore, in the following sections, we will supplement the quantitative findings with selected qualitative statements from the interviews. Let us now take a closer look at the results. Figure 4 shows the spatial dimension of intra-firm connectivity for each FUR and illustrates the five most intensively connected locations on an international scale. There are not only huge differences in the absolute number of connected branch office locations reflected by the thickness of the line but also in the hierarchy of the intra-firm connectivity for each agglomeration. The legend shows a bold and a thin line. The bold line depicts the highest connectivity value created by intra-firm interlocking networks of APS firms, which in figure 4 corresponds to the agglomeration of Zurich. London in the top position for the FUR of Zurich indicates that Advanced Producer Services firms in the FUR of Zurich most often choose London as their second most important location. The thin line, on the other hand, shows the lowest connectivity value. The other lines in figure 4 vary in thickness between the highest and the lowest connectivity value, depending on the calculated connectivity values for the corresponding agglomerations. Those companies located in the agglomeration of Zurich show by far the highest degree of internationalisation. The first national location in Zurich 's connectivity ranking is Geneva, placed in ninth position and therefore not apparent in figure 4. All other FURs within the emerging Mega-City Region of Northern Switzerland are primarily connected to Zurich, generally followed by a European location. Generally, medium-sized and small urban centres, such as Lucerne or Baden-Brugg, are not directly integrated in international networks of knowledge-intensive economic activities, but instead are well integrated in regional networks of knowledge exchange. Zurich and Basel, on the other hand, are the central nodes and gateways to the world for smaller centres in the emerging Mega-City Region and beyond. This finding confirms the important role of the agglomeration of Zurich, and to a lesser extent Basel, within the emerging Mega-City Region of Northern Switzerland for interactions at international or global levels. One reason for this is the worldwide image of these two agglomerations. For many companies operating at an international or even national level, an address in one of these cities is a matter of prestige. Many of these companies are concerned that they will not be taken seriously enough by potential customers or cooperation partners if they are not based in Zurich or Basel, but in one of the smaller centres. A management consultant in Zurich argues that they could do their job just as well in a location other than Zurich, for example in Winterthur, but their customers would not understand this at all. It would clearly affect their reputation (GLANZMANN et al., 2005:14). Furthermore, Zurich has a special role among top-ranking financial firms with international presence. It is not possible to extend this function to other centres of the emerging Mega-City Region, apart from certain back office aspects (GLANZMANN et al., 2005:14). An even more significant factor that illustrates the gateway function of Zurich is its infrastructure with the international airport and the universities with their reputation, in particular the Swiss Federal Institute of Technology (ETH). A management consultant states that it is a huge drawback for Basel that it does not have an ETH like Zurich (GLANZMANN et al., 2005:7). An interviewee from the fourth party logistics' sector points out, however, that both Basel and Zurich are indispensable agglomerations for their activities because of their rail and airport infrastructures. Whereas Basel assumes the role of gateway for international rail connections, Zurich assumes this role in the field of air travel. As a consequence, these two locations have a complementary gateway function. In this context, an essential prerequisite is the efficient transport infrastructure linking the various centres to one another and linking smaller subcentres to the international gateways of Zurich and Basel. The emerging Mega-City Region of Northern Switzerland has an excellent transport system. The rail network has a very widespread geographic coverage with high frequency and reliability. Switzerland 's motorway network is one of the densest in Europe having a very high standard. Smaller FURs profit from this, as their distances from central points such as Zurich airport become more and more insignificant. A rather interesting example is Zug, a small agglomeration with about 95,000 inhabitants. From a relative perspective, it has comparatively strong connections with international locations. Despite its small size, Zug seems to benefit from a dense network of global companies owning branch offices in several international locations giving it a special position within the emerging Mega-City Region of Northern Switzerland. The reason for Zug's relative importance lies on the one hand in its proximity to the international hub of Zurich, and on the other hand in its attractive tax policy. In contrast, Lucerne and Winterthur, which are larger agglomerations than Zug in terms of population and employment, do not display the same international connectivity. It seems that the internationalisation of companies in a specific location has a greater effect on the degree of connectivity than the mere size of an agglomeration or a core city. Generally speaking, medium-sized and small urban centres in the emerging Mega-City Region of Northern Switzerland are not directly integrated in international networks of advanced producer activities. Figure 4 shows that Advanced Producer Services firms in these locations mainly have offices in Zurich or other national urban centres, whereas international intra-firm networks are rare. Another case of direct integration in international knowledge networks is St. Gallen, an agglomeration in Eastern Switzerland with about 145,000 inhabitants. St. Gallen's virtual gateway' to international knowledge exchange networks is its internationally well known Graduate School of Business, Economics, Law and Social Sciences as well as banking institutions and business consulting firms. APS firms benefit from close ties with the university, for example with developers of ICT and business software or start-up firms in finance (THIERSTEIN, 2003). Using the same approach but shifting the scale of analysis to the national level, the spatial patterns of intra-firm networks appears different from the international scale. In this case, Zurich shows a dense branch office network with Geneva and Basel (THIERSTEIN et al., 2006:63). The smaller agglomerations, on the other hand, have an important role as regional centres, supplying regional markets with services and products due to Switzerland 's high quality infrastructure. Smaller agglomerations have to be viewed as complementary centres taking over functions which cannot be provided by cities such as Zurich or Basel. Zurich 's position as important node and gateway' location for global connectivity as well as the functional differences between the smaller agglomerations provides further evidence for the hypothesis of an emerging functional, polycentric Mega-City Region of Northern Switzerland. Spatial Patterns of Inter-firm Networks That, which has been described so far, outlines the structural organisation and spatial impact of intra-firm networks. We have focused on the analysis of the distribution of branch offices of individual companies. This approach assumes connectivity of locations by emphasising the existence of a network in line with the idea of potential knowledge exchange between the branch offices. However, this kind of approximation does not tell the whole story of the nature and quality of business activities between those different locations. Relationships between knowledge exchange and business activities do not only arise through branch office networks, but primarily from the division of labour between companies. In many cases, outsourcing strategies in respect of single activities are more efficient and lead to a higher quality of products and services. Many firms concentrate on their key competencies, which are produced in-house, while activities that do not belong to the core business are outsourced to other companies. Even networks between competitors open the opportunity for formal and informal knowledge exchange within the same field of business. We assume that these networks are strongly anchored within Mega-City Regions due to the quality of infrastructures like airports, universities with a good reputation or large settlements of leading global companies, as well as the availability of specific knowledge (THIERSTEIN et al., 2006). Under these conditions, there is a high potential for developing new products and services needing upstream and downstream inputs and costumers, which represents the different elements of the value chain in the knowledge economy. In order to fully grasp these networks, it is necessary not only to analyse the connectivity within a single firm but also the value chain relations between different enterprises and sectors. The empirical analysis of inter-firm relationships is based on an internet-based survey of about 1200 APS firms of the knowledge economy, in which 360 firms have completed the survey satisfactorily. The distribution of the numbers of companies questioned varies widely across the nine services sectors under study. At over a third, companies in the area of management consulting were the most frequent participants, followed by companies in the advertising and design consultancy sector with 17 percent. Companies in the accounting, logistics, banking and finance sector participated between 6 and 7 percent. At 4 percent and 3 percent, legal advice and insurance companies form the smallest groups. In order to keep the reply time short, the web survey comprised only four sections concerning issues about the economic region, the inter-firm relationships, the political environment of the firms as well as spatial aspects of their value chain. In order to relate the inter-firm relationships to a stylised value chain, the responding firms had to localise their business activities along the individual value chain elements of research & development', processing', marketing', sales & distribution' and customers'. Figure 5 highlights the spatial patterns of inter-firm connectivities between Advanced Producer Services (APS) firms at a national and regional level in Switzerland. It is important to note that figure 5 is a schematic diagram based on the number of interactions along the value chain, as stated by the responding firms in the internet-based survey. The thick bold line in the legend illustrates the maximum of firm-external Advanced Producer Services interrelations; the thin line, on the other hand, shows the minimum of interactions. The other lines with arrows in figure 5 vary in thickness between the highest and the lowest connectivity value, depending on the number of stated interactions by the responding firms. The most important finding of this figure is that the predominant part of the inter-firm networks is located within the demarcation of what we have been labelling from the outset of our research as the emerging' Mega-City Region of Northern Switzerland. The manifold interactions between Advanced Producer Services firms along their value chain underpin the relevance of the initially-designated area as a localised system of value chains. Within this spatial configuration, four main messages can be deduced from figure 5. Firstly, Zurich seems to be the central location in national APS networks. Interlocking networks between APS firms in different sub-centres excluding Zurich are rare. This is because Zurich is generally chosen as a location by companies which occupy a central role in the economic network. An important example here is the financial sector. Due to their central position in the functional network, these companies have corresponding radial relationships with APS firms in the other agglomerations of the emerging Mega-City Region of Northern Switzerland. Therefore, the geographical location of companies and the spatial patterns of their relationships depend strongly on the centrality of their position in the functional economic network. A second striking feature is the important relationship between Zurich and Basel. This link forms a kind of central backbone' in the national and regional interlocking network. Our analysis of the external interlocking networks between companies in the knowledge-intensive economy clearly shows strong functional links between Zurich and Basel. For many firms, Basel and Zurich are not separate economic areas, but one resource pool of potential knowledge, partners and customers. On the scale of the emerging Mega-City Region of Northern Switzerland, these two agglomerations take over complementary functions for Advanced Producer Services activities. The in-depth interviews confirm that Basel and Zurich are seen as complementary locations by knowledge intensive firms. A management consultant, for instance, states that it is simply not sufficient to have Zurich alone as a spider weaving a web of developments. He argues that Basel comprises a huge potential for encouraging innovation, thus drawing from the three neighbouring cultures of Switzerland, France and Germany (GLANZMANN et al., 2005:6). A third aspect is the rather strong connectivity that links Zurich and Berne. However, this link must be analysed in detail. THIERSTEIN et al. (2006) show that Berne is not only characterised by rather low economic dynamics but, also by pronounced regional specialisation patterns. The link today between Zurich and Berne is dominated by the information and telecommunications sector. The reason lies in the fact that Berne is home to the headquarters of Swisscom Ltd, which serves as a big provider of various telecommunication services for the emerging Mega-City Region of Northern Switzerland. This relatively strong regional specialisation characterising Berne is based on the former monopoly of the Telecom PTT. After a series of market liberalisations, Swisscom's business activities are still primarily focused on the Swiss home market. A wide array of business-related services firms that have started up since the dismantling of Telecom PTT are still located in the Berne area. As market leader Swisscom covers the largest share of domestic demand for voice and data communication services and products for residential and business applications. Thus, the strong link between Zurich and Berne is due to a singular specialisation and in our interpretation does not qualify Berne for integration in an expanded demarcation of the emerging Mega-City Region of Northern Switzerland. Another significant reason not to include the FUR of Berne in the Mega-City Region of Northern Switzerland is to be found in figure 4. The map with the intra-firm connectitivies across Switzerland clearly indicates that Berne although nevertheless an important location for formerly state-owned companies and the capital city of Switzerland is only weakly integrated into the intra-firm networks of Advanced Producer Services firms. A final salient feature is the fact that there are only few links between the knowledge economy of the emerging Mega-City Region of Northern Switzerland and the French- and Italian-speaking parts of Switzerland. The main reason lies in the language and cultural barrier. Firms in French-speaking urban centres like Geneva or Lausanne have a tendency to focus on markets in the francophone or Latin parts of the world, or an associated post-colonial background, while Zurich and Basel concentrate more on German- and English-speaking markets. ConclusionKnowledge-intensive business services firms are found to be important driving forces for spatial development in Switzerland. When looking at their value creation processes, it becomes obvious that they follow a functional and networked logic of independent as well as interdependent institutions throughout the value chain. This means that clustering in first cities within Mega-City Regions is still vital. For the knowledge economy, spatial concentration remains a key priority; there is no evidence that global functions are deconcentrating (HALL and PAIN, 2006). Clustering promotes a depth of knowledge production and is driven by the globalisation of markets and services and facilitated by developments in information and communication technologies (ICT). Knowledge-intensive businesses are agents that build spatially concentrated knowledge gateways between the regional and the global economies. Zurich is the largest of these gateways, while Basel holds number two. Within the emerging Mega-City Region of Northern Switzerland, these two agglomerations have more cultural facilities and are the only cities that have an international image for firms operating at an international or a national level. Some of the medium-sized centres are indeed able to attract knowledge-intensive industries, but they are mostly dependent on Zurich 's gateway function for international business. As mentioned at the outset of the paper, when considering polycentricity, one has to distinguish between a morphological and a relational view. Accordingly a polycentric Mega-City Region of Northern Switzerland does exist from a morphological point of view. However, from a functional perspective, considering relational patterns based on interlocking networks between Advanced Producer Services firms, there is a monocentric character to it, since Zurich is the culturally and economically dominant centre. In the case of the emerging Mega-City Region of Northern Switzerland, polycentricity has proven adequate as a descriptive model, but claiming it as a strategy for sustainable spatial development would clearly go too far. The polycentric morphology of the emerging Mega-City Region of Northern Switzerland overlaid by the functional interrelations of knowledge-intensive businesses does not lead to the desired effect of sustainable spatial development. On the contrary, the tendency towards dispersion of inhabitants that is peri-urbanization and also tendencies towards concentration of knowledge-intensive business firms in the core cities and specified locations within the agglomeration leads to an undesired sprawl of infrastructure and settlement development together with growing commuting distances. In the introduction to this paper we underlined the need for a deeper understanding of the interrelationships between polycentric spatial development and economic competitiveness. Our study provides a few facets that ultimately help to paint the whole picture. We have demonstrated that, in addition to the FUR of Zurich as core driving force behind an emerging Mega-City Region of Northern Switzerland, the smaller FURs have developed valuable positions as secondary locations. This process of an emerging new networked urban hierarchy is driven above all by Advanced Producer Services firms. Our interviews show that the location of a company outside the two largest centres of Zurich and Basel does not necessarily mean being outside the crucial information flows. Many interviewees emphasised that within the emerging Mega-City Region of Northern Switzerland it is not the precise location that is the deciding factor behind whether a firm can successfully be part of and have access to regional, national or global networks, but the well-developed network infrastructure. The real impact of changing value chains in spatial development in Switzerland is difficult to grasp. On the one hand, there is an accelerated concentration of highly advanced and knowledge-intensive functions in just a few centres; on the other hand, there is a diffusion of associated functions, such as supply, residence or leisure functions. These contradictory processes are a great challenge to the concept of polycentricity, as both polycentric and monocentric tendencies are results of the same process towards a more knowledge-intensive economy. These functional interrelations in the emerging Mega-City Region of Northern Switzerland are not yet sufficiently anchored in the awareness of most stakeholders, the least with policymakers. Despite of the actual development tendencies at the level of Mega-City Regions, the fields and spheres of activity of the institutional bodies responsible for spatial development are largely determined by the awareness of problems on a local, or at most, cantonal level. Therefore, further research has to deal with two specific aspects. Firstly, interrelationships between APS firms and the wider economy have to be analysed in greater detail. A matter of particular interest is the comparison of APS firms and the High-Tech sector. By revealing their business strategies and their rationale to locate branches and business offices, important insights into the spatial division of labour within and between Mega-City Regions can be gained. In this respect, the value chain approach is a promising tool to identify and localise the core business activities and to determine where the different functions are mainly anchored. Secondly, it is important to grasp the networks of the knowledge economy simultaneously on different geographical scales. In order to show the potential contradictions of polycentricity between different geographical levels, new methods of analysing and visualising polycentric development have to be established. REFERENCESBEHRENDT H. and KRUSE C. (2001) Die Europäische Metropolregion Zürich - die Entstehung des subpolitischen Raumes, Geographica Helvetica 56, 202-213. CASTELLS M. (1996) The Information age: Economy, society and culture. Blackwell Publishers, Malden. COMTESSE X. and VAN DER POEL C. (2006) Le Feu au Lac. Vers une Région métropolitaine lémanique. Avenir Suisse, NZZ Libro, Editions du Tricorne, Zürich, Genf. DERUDDER B. (2006) On Conceptual Confusion in Empirical Analyses of a Transnational Urban Network, Urban Studies 43, 2027-2046. DÜMMLER P., ABEGG C., KRUSE C. and THIERSTEIN A. (2004) Analysen zur Betriebszählung 2001: Standorte der innovativen Schweiz. Räumliche Veränderungsprozesse von High-Tech und Finanzdienstleistungen. Bundesamt für Statistik, Neuchâtel. ESPON (2004) ESPON 1.1.1. Potentials for polycentric development in Europe. Project Report. European Spatial Planning Observation Network, Luxembourg. EU (2007) Territoriale Agenda der Europäischen Union. Für ein wettbwerbsfähiges nachhaltiges Europa der vielfältigen Regionen, Leipzig. EUROPEAN COMMISSION (1999) ESDP: European Spatial Development Perspective: Towards Balanced and Sustainable Development of the Territory of the European Union, Brussels. EUROPEAN COUNCIL (2000) Presidency Conclusions - Lisbon European Council, 23 and 24 March, Lisbon. FRIEDMANN J. (1986) The world city hypothesis, Development and Change 17, 69-83. GABI S., THIERSTEIN A., KRUSE C. and GLANZMANN L. (2006) Governance Strategies for the Zürich-Basel Metropolitan Region in Switzerland, Built Environment 32, 157-171. GEIGER H., BRETSCHGER L. and KRUSE C. (2006) The Swiss Financial Center as a value added system. First Report. Swiss Financial Center Watch, Zürich. GEMACA (1996) North-West European Metropolitan Regions. IAURIF, Paris. GLANZMANN L., GRILLON N., KRUSE C. and THIERSTEIN A. (2005) POLYNET Action 2.1. Northern Switzerland. Qualitative Analysis of Service Business Connections, Institute of Community Studies/The Young Foundation & Polynet Partners. GRABHER G. (1991) The Embedded Firm: The Socio-Economics of Industrial Networks. Routledge, London. HALBERT L., CONVERY F. J. and THIERSTEIN A. (2006) Reflections on the Polycentric Metropolis, Built Environment 32, 110-113. HALL P. and PAIN K. (2006) The Polycentric Metropolis. Learning from Mega-City Regions in Europe. Earthscan, London. HOOVER E. M. and VERNON R. (1959) Anatomy of a Metropolis. Harvard University Press, Cambridge, MA. MALECKI E. J. (2000) Creating and Sustaining Competitiveness. Local Knowledge and Economic Geography, in BRYSON J., DANIELS P., HENRY N. and POLLARD J. (Eds) Knowledge, Space, Economy, pp. 103-119, London, New York. MOULAERT F. and SEKIA F. (2003) Territorial Innovation Models: A Critical Survey, Regional Studies 37, 289-302. OECD (2002) Territorial Reviews. Switzerland, OECD, Paris. PERROUX F. (1952) Note sur la notion de Pole de croissance, Economie applique. PIORE M. J. and SABLE C. F. (1984) The second industrial divide: Possibilities for Prosperity. Basic, New York. POLANYI M. (1967) The tacit dimension. Loutledge & Kegan Paul, London. PORTER M. E. (1998) Clusters and the New Economics of Competition, Harvard Business Review, 77-90. SASSEN S. (2001) The Global City: New York, London, Tokyo. Princeton University Press, Princeton, New-York. SCOTT A. J. (1985) Location processes, urbanisation and territorial development: an exploratory essay, Environment and Planning A 17, 479-501. SIMMIE J. (2004) Innovation and Clustering in the Globalised International Economy, Urban Studies 41, 1095-1112. SIMMIE J. (2005) Innovation and Space: A Critical Review of the Literature, Regional Studies 39, 789804. SIMMIE J., SANETT J., WOOD P. and HARDT D. (2002) Innovation in Europe: A Tale of Networks, Knowledge and Trade in Five Cities, Regional Studies 36, 47-64. STORPER M. (1997) The Regional World. Territorial Development in a Global Economy. The Guilford Press, New York, London. STORPER M. and WALKER R. (1988) The geographical foundations and social regulations of flexible production complexes, London. TAYLOR P. and EVANS D. (2005) POLYNET Action 1.2. Quantitative analysis of service business connections. Summary Report. Institute of Community Studies/The Young Foundation & Polynet Partners. TAYLOR P. J. (2004) World City Network: A Global Urban Analysis. Routledge, London. THIERSTEIN A. (2003) Financial places, regional production system, and the gap to bridge: considerations for a research agenda, in THIERSTEIN A. and SCHAMP E. W. (Eds) Innovation, Finance and Space, pp. 197-214. Selbstverlag Institut für Wirtschafts- und Sozialgeografie der Johann Wolfgang Goethe Universität, Frankfurt. THIERSTEIN A., KRUSE C., GLANZMANN L., GABI S. and GRILLON N. (2006) Raumentwicklung im Verborgenen. Untersuchungen und Handlungsfelder für die Entwicklung der Metropolregion Nordschweiz. NZZ Buchverlag, Zürich. VERNON R. (1966) International Investment and International Trade in the Product Cycle, The quarterly journal of economics LXXX, 190-207.

Table 1 Knowledge-intensive economies in the emerging Mega-City Region of Northern Switzerland and in Switzerland. (THIERSTEIN et al., 2006:41).

Table 2 Development of the most dynamic economic sectors in Switzerland (GEIGER et al., 2006:74).

Table 3 Business inventory for the eight main Functional Urban Regions (FURs) and their Cores in the emerging Mega-City Region of Northern Switzerland. Source: Swissguide online registry (http://www.suissguide.ch) (Own classification).

Figure 1 Knowledge and Learning within institutional and territorial context (Own illustration).

Figure 2 Two emerging Mega-City Regions of Switzerland (Own illustration).

Figure 3 Relative change of locations and employment per sector 1995-2001 (percentage) (GEIGER et al., 2006 :75).

Figure 4 International dimension of intra-firm networks of the emerging Mega-City Region of Northern Switzerland (Own calculation).

Figure 5 National and regional inter-firm connectivity of the emerging Mega-City Region of Northern Switzerland (Own calculation).

NOTES* Alain Thierstein; Munich University of Technology, Chair for Territorial and Spatial Development, thierstein@raumentwicklung.ar.tum.de ** Stefan Lüthi; Munich University of Technology, Chair for Territorial and Spatial Development, luethi@raumentwicklung.ar.tum.de *** Christian Kruse; Bank Morgan Stanley AG, Zürich, christian.kruse@morganstanley.com **** Simone Gabi; City of Zurich, Urban Planning, simone.gabi@zuerich.ch ***** Lars Glanzmann; ALSTOM (Schweiz) AG, Baden, laglanz@bluewin.ch

Note: This Research Bulletin has been published in Regional Studies, 42 (8), (2008), 1113-1131 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||