GaWC Project 104 |

|

|

The State of African Cities 2018 - The Geography of African InvestmentFunded by: UN-Habitat, University of the Witwatersrand (SEBS), Erasmus University Rotterdam (IHS), African Development Bank (AfDB), UKAID, Government of Norway and PFD Media Group Report development: Ronald Wall, Jos Maseland, Katharina Rochell and Mathias Spaliviero

IntroductionRecently the full 400 page State of African Cities 2018: The Geography of African Investment Report was launched. According to this UN-Habitat report, foreign firms and investors into African cities can play a critical role in the region’s development, and explores how Africa can help finance its development by attracting FDI to cities. This, hereby noting that SDG 11 (sustainable cities and communities) recognizes the role of cities as productivity hubs that drive growth and development, and attract investment. As such, African governments must connect FDI to sustainable urbanization by strengthening urban policies and planning, and financial and legal systems. According to Aisa Kirabo Kacyira, Deputy Executive Director UN-Habitat, the “groundbreaking” nature of the study is due to its focus on the economic geography of FDI, rather than strictly on urbanization itself, which is a necessary countermeasure considering that by 2030, half of Africa’s population will live in cities, which will likely exacerbate unplanned urbanization, informal settlements, poverty, inequality, unemployment, humanitarian crises and conflict. It is argued in the report that the advancement of African cities is not only important for the continent’s future, but arguably for the entire world. For this reason, the report’s studies have explored African cities as integral components in an evolving world system. The analyses explore the effects of past FDI on different African locations e.g. inequality, employment and food security, as well as the factors desirable to make African cities more attractive to future investors e.g. good governance, infrastructure and regional integration. About the reportDrawing on various databases e.g. fDi Markets and Orbis, investment flows between many world cities and covering the period 2003 - 2017, the report explores the economic integration of African cities with other world cities. The report is unique as it reveals FDI into cities as well as countries. The report empirically shows the networks of FDI that bind African cities into the world investment system, using GIS, network analysis and econometric techniques. The spatial structures, trends, and forecasts of African FDI are revealed in the report at global, continental, national and urban scales, and show how these impact social, environmental and economic developments in African cities. The report covers various studies done by researchers from different international universities, including Chinese FDI into Africa; the impact of investment on inequality, employment and wages; food investment and food security; investment competitiveness, renewable energy investments and climate change. Also, four case studies are explored in-depth by local researchers from the cities of Johannesburg (South Africa), Cairo (Egypt), Abidjan (Ivory Coast) and Kigali (Rwanda). The aim of the study has been to contribute to policies that can make African cities into more attractive, competitive and resilient FDI destinations, and how to use investment to improve economic development. For instance, it is shown that that cities need to intimately engage with higher scales of policy-making, e.g. supra-regional and continental. Urban regional agglomerations are critically important for attracting investors given their unique capacity to capture and enable diverse economic activities. African cities increasingly shape the economic performance of entire countries and regions and should therefore be more actively viewed as constituent parts of regional economies of scale. In advancing the economic development of the African continent, while addressing high levels of income inequality, unemployment and poverty, the five major African regions, within the responsibility of their respective regional institutions and the African Union, should closely collaborate to target different sources of FDI worldwide. Attracting global FDI is highly competitive and therefore regional cooperation is critical to amplify individual cities’ and nations’ negotiation strength. FDI in AfricaIn recent years, especially after the 2008 financial crisis, there has been a steady increase in FDI towards the Global South. This has been a welcome trend for Africa, not only because of its developmental challenges, but also due to the generally limited availability and expense of domestic financing, which has stubbornly hampered African businesses. Nonetheless, despite a growing FDI influx, Africa’s share of the total volume of world FDI remains small, at roughly 5%. This compares poorly with the continent’s 15% share of global population and over 30% of world poverty. The currently large GDP per capita gap is likely to widen if ‘business as usual’ were to continue. This is further reflected in Africa’s relative disconnection with the global investment system. There is a pressing need for more FDI in Africa. Financial and policy interventions are needed to support Africa’s emerging transformations and strengthen the already declining primary sector (resources) investments, towards secondary and tertiary sectors (manufacturing, services and hi-tech). This would facilitate structural economic transformation and generate higher value added productivity on economic activities. In this light, FDI is a key resource to expedite Africa’s growth potential, since it promises to bring not only financial resources, but also new technologies, knowledge and expertise. Investment generally promotes employment, productivity and competitiveness through entrepreneurship in FDI destinations. Substantial private capital injections can, for instance, help close Africa’s massive gap in physical infrastructure, improve the quality of the built environment, and make it a more attractive destination for FDI. The role of citiesCities perform a quintessential role in Africa’s evolving transformation because urban environments facilitate growth in critical economic sectors. Cities can accommodate the industries that already demonstrated notable and sustained economic growth from 2003 to 2017, and whose trend is anticipated to continue. African cities can boost their economies by positioning themselves as desirable locations for multinational firms’ regional headquarters or sub-offices and thereby become important nodes in these firms’ corporate strategies and supply chains. However, it is pertinent that, as potential FDI destinations, cities should understand investors’ rationales to expand business to foreign countries. In an age of globalization and the emerging 4th industrial revolution, the role of African cities and urbanization must reverberate in the long-term economic, spatial and demographic planning of the continent. Under conditions of very rapid urbanization, African cities bring both problems and solutions; notably in respect to urban poverty incidence. In the absence of commensurate economic growth in urban and rural economies alike, urban poverty occurrence has become proportional to the rate of urban-rural migration and natural urban growth. Conversely, urban economic development can lift millions out of poverty, as it has done in East-Asia over the past three decades, with African cities becoming hubs of productivity that accelerate economic growth and broad-based well-being. For that to happen, African cities need to seize a more prominent position in the world economy by enhancing their accessibility, connectivity, markets and place attachment. They also need to build workers' skills and productive capacity, their knowledge and technology levels as well as their institutions and investment networks. FDI can be a means to kick-start this. General conclusionsDespite its relatively low ability to attract FDI in comparison to other continents, the recent rate of FDI growth into Africa is the second highest in the world. While this is partially explained by the low investment base from which the continent started, it does demonstrate a growing interaction between Africa and the global economy. Indeed, FDI is now an important source of finance and represents roughly a third of foreign financial sources flowing into the continent. The better a city or urban agglomeration is globally and regionally connected as an FDI destination, the more FDI it will be able to attract. Cities will have stronger economies when they facilitate international trade and link up to diverse FDI clusters in the world economy, while at the same time boosting their own local markets and economies. African cities should, therefore, develop strategies to become key nodes for commodities and services in the global marketplace. Spatial policies such as industrial zoning and clustering are conducive to this because they help create opportunities to engage peripheral parts of the urban agglomeration in economic development. They also help provide investments in physical infrastructure and social capital, while enhanced ICT supports improved accessibility and connectivity. Key aims would be to make major inroads into addressing urban unemployment and poverty, lower urban informal settlement (slums) proliferation and, not in the least, securing critical future urban food security. In this sense Africa’s urban revolution will have to go hand-in-hand with a pronounced agricultural revolution. Nonetheless, FDI is neither a panacea nor the ultimate answer since it has both good and less helpful traits. Commonly recognized negative aspects of FDI are its potential for crowding-out local businesses in developing economies; its tendency to prevent or reduce domestic investments; and latent adverse consequences of certain sectors to increase wage inequality and block the development of indigenous skills. Therefore, careful choices should be made by cities in their pursuit of new and additional FDI, which can lead to inclusive economic growth. Some key findings

General recommendationsThe report makes city-level, country-level, regional-level, continental-level and global-level recommendations, calling for, inter alia:

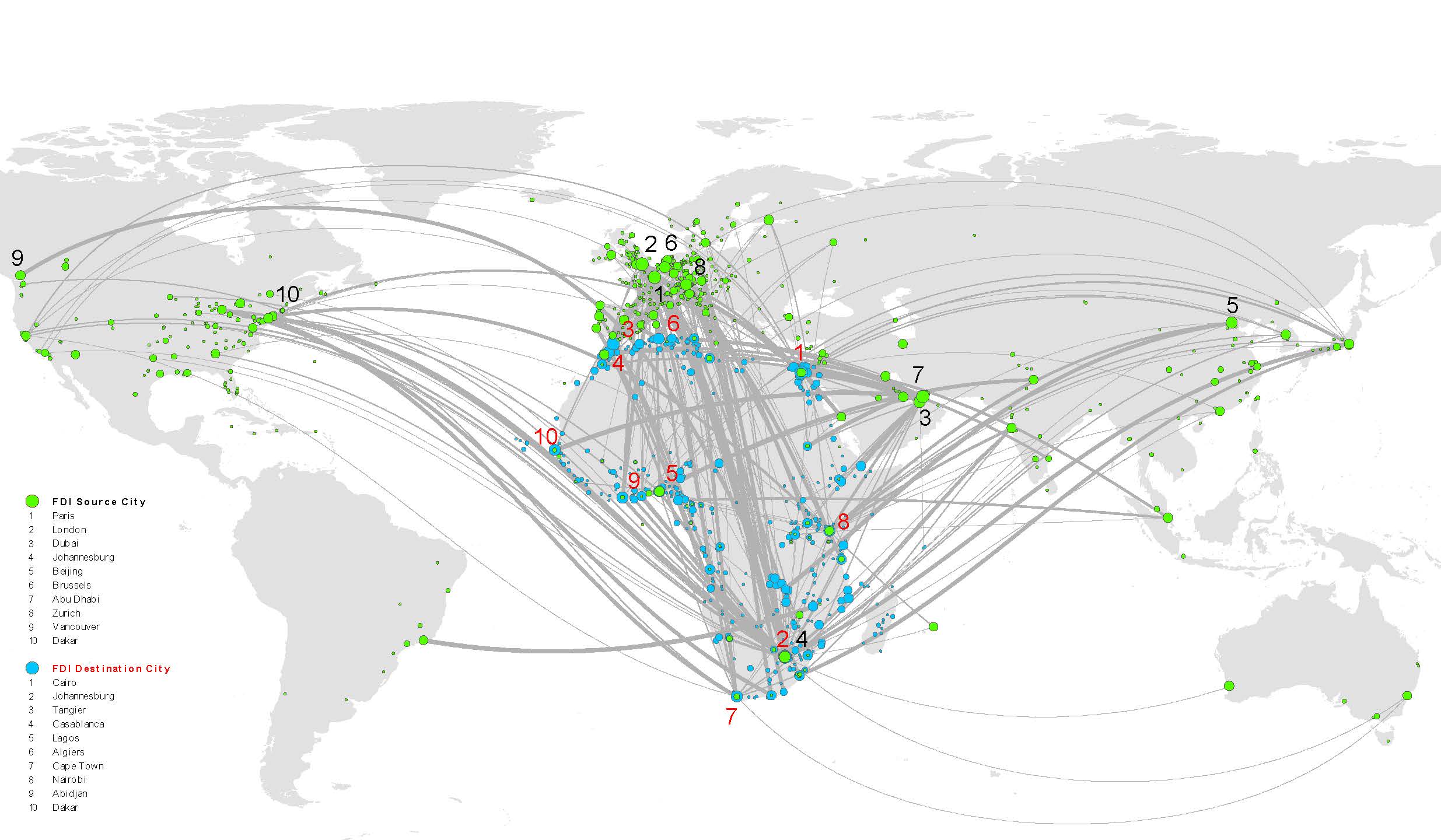

All FDI from global cities into African cities (2003-2016)

Blue nodes: total inward FDI Green nodes: total outward FDI Grey lines (linkages): all investments with Africa (Source: Wall, 2017. Based on fDi Markets data) Foreign Direct Investment Distribution to World Cities (animation)

This post was written by Ronald Wall, and is based on The State of African Cities 2018 – The Geography of African Investment (UN-Habitat) report. The report was initiated and developed by Ronald Wall (Wits University and IHS-Erasmus University Rotterdam), Alioune Badiane and Jos Maseland (UN-Habitat), and co-developed by Katharina Rochell and Mathias Spaliviero (UN-Habitat). This post represents the views of the author. Professor Ronald Wall is a Full Professor in the School of Economics and Business Sciences (SEBS) at the University of the Witwatersrand, Johannesburg. His research concerns global and regional economic development, inter-city network analysis and urban planning studies.

For results of this project, see The State of African Cities 2018 – The geography of African investment

|

||