GaWC Research Bulletin 452 |

|

|

|

This Research Bulletin has been published in Progress in Human Geography, 39 (6), (2015), 752-775. Please refer to the published version when quoting the paper

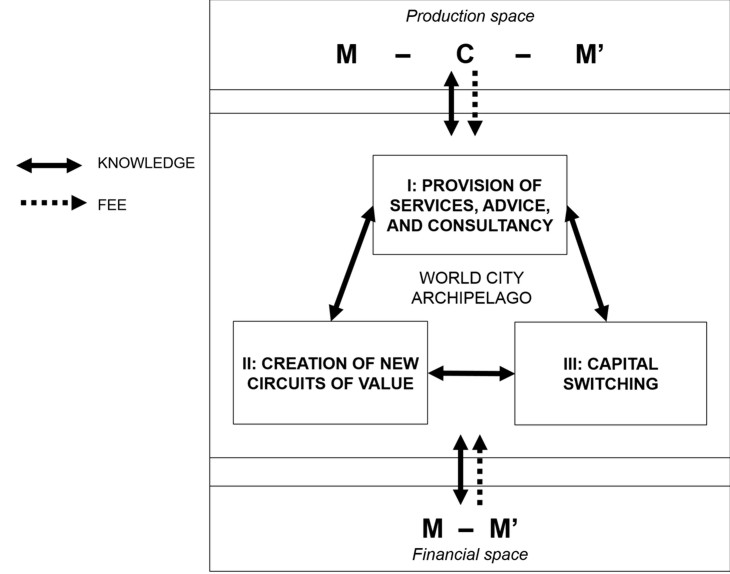

I World cities: Continuity and changeThe durability of the economic woes that erupted with the financial meltdown of 2008 challenge ideas of worldwide market-led economic convergence and invite a focus on the mechanisms that (re)produce geographies of uneven development (Aalbers, 2009; Engelen and Faulconbridge, 2009; Harvey, 2014). A recurring theme in these uneven geographies is the unmistakable metropolitan dimension in terms of the crisis' origins, manifestations, and remedies. While the crisis reaches deeply in terms of societal depth and geographical range, some places matter more to our understanding of its genesis than others (Clark, 2005). In terms of origins, New York and London, but also many other densely interconnected urban areas across the globe were crucial cogs in the production and spread of the crisis (French et al., 2009; Wainwright, 2012; Wójcik, 2013a). It was here that large bank defaults and massive temporary lay-offs first manifested themselves after the crisis commenced, even though the imminent default surge quickly expanded beyond the toxic-asset pools buried beneath the pinnacles of finance (Bassens et al., 2013a; Derudder et al., 2011). Since then, it have been the very same localities that are re-positioning themselves as candidates for post-crisis growth regimes (Engelen and Glasmacher, 2013). Metropolitan centers and the practices within them remain essential components of any analysis of the contemporary capitalist order of which the financial crisis was a direct product (Sassen, 2010). Comprehending capitalism from the perspective of metropolitan centers is all but novel. At least since the 1980s, the world cities research tradition has explicitly and critically analyzed the spatial organization of global capitalism from the vantage point of networked city localities (Friedmann and Wolff, 1982; Friedmann, 1986). More recently, world cities research has increasingly understood the global economy's spatial organization as an archipelago of world cities (Taylor, 2004) . This conceptualization, based on the notion of a flow-centered metageography, captures interurban interconnections that undergird the global economy (Beaverstock et al., 2000; Taylor, 2004; cf. Lewis and Wigen, 1997), which cannot be reduced to constituent national economies (Sassen, 1991 [2001]). The networked perspective invoked a lively empirical debate about the actual geographical articulation or 'footprint' of the world city archipelago (WCA) and its backbone of International Financial Centers (IFCs) in the past decade. This has occurred either through ever more sophisticated determinations of its most relevant 'islands' and connections (Derudder et al., 2010) or challenging where the boundaries of the archipelago space lie (Bassens et al., 2010; Lai, 2012). The overall consensus is that capitalist 'command and control' is exercised from a limited set of cities which function as nodes for transnational flows of capital, goods, people, and information from which actors operating from these places draw their power (Allen, 2010; Parnreiter, 2014). Accepting the more or less agreed-upon geographies of the WCA, this article sets out to meet the challenge of revisiting the question of what goes on in WCA space. Such an analytical exercise can be performed on at least two levels of abstraction. One can engage in a metatheoretical exercise envisioning the WCA as an abstract networked unity that performs a certain, yet to be defined, part in contemporary capitalism (Castree, 1999). Alternatively, the internal differentiation of the WCA could be the focus, where one details the role of (sets of) particular cities. The ambition of this paper is to take the former course of action, where as a mode of exposition we choose to augment Friedmann's (1986: 89) original world city hypothesis; not to retrospectively debate its validity at the time of conception, but to attempt to adapt the thesis to contemporary conditions of financialized globalization. Friedmann (1986) conceptualized world cities' as key basing points of capital from where the escape of the labor market rigidities of the 1970s crisis were orchestrated, while retaining capital accumulation in the world's economic core areas. The related work on global cities' (Sassen-Koob, 1982, 1985; Sassen, 1991 [2001], 1998) theorized places where global control functions are produced by Advanced Producer Services (APS) in accountancy, advertising, finance, law, and management consultancy. Following Parnreiter (2013), we take Friedmann's definition of world cities to stand very close to Sassen's global city concept as both examined the same processes in the same places in the same era. Expanding these pioneering works, an augmented world city hypothesis has to address the different nature of the current crisis compared to the one of the 1970s. Both crises can be considered as different expressions of a general crisis of overaccumulation, even though the barriers to capital realization are currently very different (Harvey, 2010). Following Marx (1894[1991]), Harvey (1982[2006]: 192) defines overaccumulation as a state of over-production of capital when the 'capitalists' necessary passion for surplus-value-producing technological change, when coupled with the social imperative 'accumulation for accumulation's sake', produces a surplus of capital relative to opportunities to employ that capital.' As Harvey (2010: 64) notes, the crisis of the 1970s was characterized by a profit squeeze in the context of stagflation, whereas the recent crisis shows capitalism's flipside expressed in overproduction facing a lack of effective demand in established circuits of value (Harvey, 2010: 65-66, 116). Following the arguments of Harvey (2010, 2014) and Arrighi (1994[2010]), we expect the increasing importance of financial capital circuits i.e. financialization and rent-seeking behavior (Harvey, 2014) to change the character of command and control functions exercised from world cities. While still functioning as a space from where global production is coordinated to an important degree, we argue that these practices related to command and control have been subsumed in a logic of financialization, making that the world city archipelago constitutes an obligatory passage point for the relatively assured realization of capital under conditions of financialized globalization (cf. Allen, 2010). The rise of global financial markets has increased the global level of uncertainty about capital realization to such an extent that APS in world cities - as providers of the necessary and seemingly sufficient authority and expertise - collectively hold a fee-earning class monopoly' that yields 'class monopoly rents' (Harvey, 1974). Such an augmentation blurs differences between world cities research and financial geography since the social processes and associated geographies overlap significantly (Coe et al., 2014; Sassen, 2010; Wójcik, 2013b). Yet, at the same time, it is overly reductionist to collapse the more extensive geography of the WCA onto a concise network of IFCs. Typologically, whereas all IFCs are world cities, the WCA does greatly extend beyond that shortlist because, as we shall extensively argue below, APS practices relating to the worlds of finance and production have increasingly become interdependent. The paper is organized as follows. Section two will review the evolving political-economic context in which world city research operated since the 1980s and describes associated changes in command and control. Section three sets up the theoretical apparatus to incorporate financialization in the world city hypothesis. By analyzing the hazards of capital accumulation under the current round of overaccumulation it elucidates the practices and interactions among APS firms and their clients that help reproduce the geography of world cities. We subsequently discuss how this relates to understandings of the financial crisis of 2008. The paper concludes with suggestions for how empirical research on the WCA could be informed by, and simultaneously corroborate, this augmented world city hypothesis. II The changing mode of command and control in world citiesThe defining feature of world cities at least from its political-economy perspective that originates with the work of Stephen Hymer (1972) and that became famous through John Friedmann and Goetz Wolff (1982, see Parnreiter, 2013; Surborg, 2011 for recent historical overviews) is their role as 'basing points' for global capital from which 'command and control' is exercised over capitalist accumulation (Friedmann, 1986; Hymer, 1972; Sassen 1991[2001])1. Although world city research has more recently been focused on the geography of the archipelago of world cities and its interrelations (Taylor, 2004), the notion that capitalist command and control defines the research object has been broadly maintained (Saey, 2007; Surborg, 2011; Parnreiter, 2013, 2014). However, not all scholars accept the relation between command and control and world cities uncritically. Criticisms cover two broad topics. First, command and control has been argued to be too crude a notion to specify the relation between world cities and the exercise of power and therefore needs unpacking (Allen, 2003, 2010; Jones, 2002; Thrift, 1993). John Allen (2003: 5) convincingly makes the case in this respect that we have to 'clearly distinguish between the exercise of power and the resource capabilities mobilized to sustain the exercise'. Interpreting Allen (2003: 108, 112, 152-157), it is the assemblage of resources and abilities accessible from the WCA that enables command and control in world cities, leaving the actual exercise of that power a contingent matter. For Allen (2010: 2898, building on Callon, 1986), world cities constitute an 'obligatory passage point' for particular business practices 'to work'. Its micro-foundations are built on the practices of financial and business elites in the WCA that involve modes of power such as manipulation, seduction or inducement other than top-down domination and control (Allen, 2010; Jones, 2002). This revision of command and control informs the analysis developed hereafter (cf. Saey, 2007) and is illustrative of how analytical strategies informed by poststructuralist perspectives can illuminate aspects of time-tested debates regarding the workings of capital in new ways (cf. Berndt and Boeckler, 2010; Jones, 2008). Second, the contingent nature of the exercise of power on the micro-level has led some authors to question the validity of the claim that command and control define world cities on the macro-level (Smith and Doel, 2010; Thrift, 1993) up to the point of calling the existence of command and control in world cities a myth (Smith, 2014). The central tenet of this conviction is that capitalism has changed so profoundly in the last decades due to the rise of finance and its associated complexity that it is essentially 'uncontrollable' (Thrift, 1993: 232), as is taken to be exemplified by the erratic, volatile, and crisis-prone nature of the global financial system (Smith, 2014: 104). For Thrift, ongoing concentration in world cities should primarily be explained from their role as ' sites of social contact and narrative innovation, as places where this new world presents and represents itself, as places for storytelling rather than strategy' (Thrift, 1993: 233). Whereas the processes in world cities have changed substantially, we see no evidence to conclude that the notion of command and control as conceptualized above is a myth. Rather, we argue, current modes of command and control seem to come to a crucial extent with the ability of agents in world cities to produce strategic narratives' (Christophers, 2009; Froud et al., 2006; Hall, 2006) which rely to a significant degree on storytelling to make the crisis-prone global financial system legible, but which also involves circumscribed expertise of the specific APS trade. For instance, as is evident in offshoring, law firms and investment banks have a set of standard or customized solutions on offer that allows clients to circumvent tax regulations (e.g. Wainwright, 2011). The enduring concentration of command and control in world cities and its qualitative changes under financialization then become a crucial conundrum to disentangle. To understand this shifting emphasis in the modality of command and control it is helpful to revisit the changes in the political-economic context from the crisis of the 1970s and 1980s onwards. We identify three epochs in particular, which exemplify distinct dominant practices of command and control that morphed into one another. When Friedmann and Wolff (1982) first articulated their world city hypothesis they had a very specific goal in mind. By the 1980s it had become clear that the world economy had found ways out of the crisis of Fordism that had ravaged the 1970s. Culminating with the Volcker Shock, a decade of massive capital shortage in core economies like the US had gradually been reversed as a consequence of the massive transnationalization of global financial capital flows (Christophers, 2013; Krippner, 2010) enabling large transnational corporations (TNCs) to readjust their global capital outlay. Part of this readjustment was an increased globalization of industrial capital as labor-intensive production was being offshored to the periphery' to reap the benefits of low skilled non-unionized cheap labor while the same corporations divested their production plants in the 'core'; a process that was labeled the New International Division of Labor (NIDL) (Fröbel et al., 1977 [1980]; Hymer, 1972). World city scholarship of the early 1980s, such as Cohen (1981), Friedmann and Wolff (1982), Ross and Trachte (1983), and Sassen-Koob (1982, 1985) was concerned with the spatiality of the causes and consequences of these developments. Centralization of capital in the core while production was offshored to the periphery posed a coordination problem. This spatial division of labor had to be conducted in a global institutional context that was not yet optimized for global capital and yielded a significant amount of labor for highly-educated service work in the world's best connected places, world cities, to alleviate transaction costs. The fact that TNCs were actually making huge profits globally in the midst of local deindustrialization gave rise to case-based scholarship on these issues (e.g. Massey, 1984 [1995]; Soja et al., 1983). Control in this context meant literally control over assets stretched over space': How could a global production process be organized with the cheapest possible labor inputs while repatriating the profits to the corporate headquarters? Even in the early 1980s, the debate was embroiled by notions of the rise of a service economy' and the coming of postindustrial society' (Bell, 1973). However, more complicated socio-spatial configurations were also emerging that could not be explained by the somewhat crude capital seeks cheapest labor' arguments of the NIDL thesis (see Henderson and Castells, 1987; Ross and Trachte, 1990). Silicon Valley (e.g. Saxenian, 1996) and the Japanese Toyotism model (Schoenberger, 1997) were examples of capitalist growth regimes based on relative surplus value realization that could retain their local embeddedness'. Regional economies could be competitive by specializing in sophisticated production processes that were difficult to replicate elsewhere (Storper and Walker, 1989, cf. Tickell and Peck, 1992). Innovative regions within these competitive flexible production systems could then utilize their comparative advantages in the trade system of a new regional world (Scott, 1998; Storper, 1997), all made possible by the new technologies that powered the 'rise of the network society' (Castells, 1996 [2000]). Importantly, this regional narrative of flexibility had its counterpart in changes to how control was exercised within large corporations. During the 1980s, corporate governance had gradually transformed from a hierarchical portfolio organization under managerial control (central in Hymer, 1972) to flexible organizations dominated by a shareholder value regime (Fligstein, 2001). Once initiated, these organizational forms and strategies gradually became omnipresent across industrial fields through organizational mimicry (DiMaggio and Powell, 1983). These evolutions were also crucially mediated by the state: The decision in 1981 by the Reagan administration to relax antitrust laws, which until then stymied large mergers and acquisitions, raised the relevance of their stock market performance (Fligstein, 2001: 156). Moreover, in a context of progressive financial deregulation and an emerging new international financial system (Thrift and Leyshon, 1988), TNC reorganizations also involved rerouting capital through IFCs like London (Burn, 1999) and offshore financial centers (Roberts, 1995), which since long had served their purpose in Eurobond markets. Even if the outcomes were far from premeditated (Krippner, 2010), one can appreciate that financial and industrial capital deregulations allowed reaffirmation of US hegemony despite falling profit rates in industry permitting a new growth regime based on the massive import of foreign capital (Arrighi, 1994[2010]; Harvey, 2003). World cities seemed to fit into the new postfordist growth theory as they were theorized as sites hosting command and control functions that served as alleviators of transaction costs barring the realization of the comparative advantages of the new regional world. Services were interpreted to lubricate the process of flexible specialization in a globalizing economy that became increasingly interconnected through information technology (see Daniels and Moulaert, 1991; Knox and Taylor, 1995; Moulaert et al., 1997). Collectively, APS could be regarded as just another regional specialization as control functions were gradually being externalized to independent APS TNCs that themselves were subject to agglomeration economies in world cities (Coffey and Bailly, 1990) acting as neo-Marshallian nodes in global networks' (Amin and Thrift, 1992; Brenner 1998; Sassen, 1991 [2001]). Sassen (1988, 1991 [2001]) introduces the term 'Advanced Producer Services complex' (henceforth APS complex) to express this specialized and collective role of APS in the world economy. Yet, it was acknowledged that APS differed from other regional specializations by having a seemingly indispensable function for the others, namely that of providing 'global control capability' (Sassen-Koob, 1985; Sassen, 1991 [2001]). Operational efficiency through flexibility implied an increased focus on the return on capital of the firm. Thus, firms aiming for shareholder value were drawn to optimize these efficiency metrics as they became more important for investors to gauge and compare firms' operational performance. Apart from assisting TNC in optimizing and making more flexible their supply chains, APS firms played an important role in the codification and implementation of these metrics as well (Froud et al., 2000, 2006). This emphasis on world cities as particular regional specialization received significant criticism, since it works to naturalize highly unequal power relations, while covering up proactive state policies and subsidies that support world city formation (Massey, 2007). Nevertheless, the postfordist discourse of innovative regional specialization as a growth model remains dominant, albeit contemporarily subsumed in discourses regarding a knowledge based economy' (e.g. Rodrigues, 2002) or the cognitive-cultural economy' (Scott, 2012: 11). Innovation persists to be an important competitive strategy to achieve capital accumulation (Scott, 2012; Storper and Walker, 1989). However, in an effective demand crisis it is highly unlikely to be sufficient to achieve a sustainable three percent worldwide compound growth path (Harvey, 2010, 2014). Therefore, we expect that other capital accumulation strategies such as expansion in space through processes associated with globalization and time through credit have become increasingly important as the world slid into a crisis of overaccumulation (Arrighi, 1994 [2010]; Harvey, 1982 [2006], 2010). Moreover, research on geographies of innovation processes and scientific knowledge production (Asheim et al., 2007; Saxenian, 2007) suggest that the relationship between geographies of world cities and innovation is often ambiguous. Accountants, lawyers and bankers might play a role in commodifying inventions, but they are not very likely to be at the heart of the matter, although APS narratives aim to make clients believe the contrary (Engelen et al., 2010a). In fact, multinationals relocating to world cities often tend to leave their research and development departments at their old location (Baaij et al., 2004; Muellerleile, 2009). These remarks caution against a too direct association between APS firms and development in a knowledge-based economy. If less fundamental to innovation, then, where does that leave the meaning of command and control produced in world cities? Here we hypothesize that financialization dynamics require continued and accelerated agglomeration in world cities beyond the IFC shortlist as clients are in dire need for services that allow indirect control over financial assets. While financialization entails a wide set of processes (Engelen, 2008), it can generally be understood as the growing relevance of financial motives, financial markets and financial institutions in the operation of domestic and international economies (Epstein, 2005) . First evidence is already abundantly in place: World cities have been shown to be involved in practices of territorial and financial arbitrage (Sassen, 2006; Wainwright, 2011; Wójcik, 2013a, 2013b). Furthermore, the shareholder value mode of control has led to radically different corporate strategies making corporations dependent on APS as market intermediaries (Folkman et al., 2007) to maneuver in global financial markets (Froud et al., 2006; Lee et al., 2009). Beyond the attraction of capital in primary markets, firms are directly influenced by the trading of their equity or debt in secondary markets which in turn strongly influences the possibility of raising capital in the primary market. This development has necessitated the deployment of a range of APS for the financial optimization of industrial corporations bringing along all kinds of consequences for how the firm produces adequate numbers' (i.e. value of stocks, return of investment) for shareholders and projecting strategic narratives' for external and internal consumption (Froud et al., 2006; O'Neill, 2001). These developments further drive the need for services that aid the rationalization of actual production and the optimization of the surplus, and secure a credible' and creditworthy' profile. Lastly, the deepened implementation of financial logics in post-welfare states, for instance through massive privatized pension schemes (Boyer, 2000; Clark, 2003; French et al., 2011; Hall, 2012), but also through state strategies that fuel world-city formation as growth strategy (Harvey, 1985; Massey, 2007; Olds and Yeung, 2004), are likely to augment and deepen command and control functions in world cities. Taken together, these three developments suggest financialization processes are not just emanating from practices taking place in mainstay IFCs, but are introduced more deeply into wider economies by APS operating from a much broader set of world cities.III World cities as obligatory passage points under financialized globalization1 The Emergence of an APS Class Monopoly due to OveraccumulationIn order to understand the enduring relevance of world cities for command and control over capital we have to delve into the specific role that the APS complex plays in the valorization and realization of capital in the context of financialization. We construct that argument by drawing on the conceptual apparatus of historical-geographical materialism (Harvey, 1982 [2006], 2010). We start our inquiry with the central axiom that contemporary capitalism is increasingly characterized by a state of overaccumulation of capital that is the root cause of the increasing prevalence of economic crises (Arrighi, 1994 [2010]; Harvey, 2010). Capital' is a process of value in motion: Money capital is brought into a circulation process consisting of a combination of constant and variable capital that eventually allows for the realization of its initial value and a surplus. This necessarily implies the consumption of a use value of some sorts (Marx, 1885 [1992]). The lag between the initial capital layout and the moment of final consumption, and therefore the ultimate realization of surplus value, can be stretched across space and time. Until this moment of realization, capital has to be regarded as fictitious' since it is unknown whether or not it will finally realize itself: an investment can fail (Marx, 1894 [1991]: 594-606; cf. Harvey, 1982 [2006]: 267). In order for capital to reproduce itself and expand there have to be enough investment opportunities to realize surplus value. And these opportunities have to be orchestrated by socially constructing material circuits of value (Lee, 2006, 2011). Switching capital between these various circuits involves significant transaction costs which function as barriers to capital and surplus realization and a source of crises (Harvey, 1982 [2006]). The alleviation of these transaction costs is generally considered one of the important functions of the financial system, which collects a fee in return (Strange, 1988 [1994]). In absence of overaccumulation, one could argue that the APS complex serves to alleviate transaction costs and thereby make markets more efficient: It is through the labor of the APS complex that valorizations of capital come into existence that otherwise would not have occurred (Bryson et al., 2004; Christophers, 2013; Walker, 1985). However, in a period of overaccumulation these transaction costs acquire a new character. During overaccumulation there is 'a situation where there is excess capital relative to the opportunities to use capital profitably' (Harvey, 2010: 45), otherwise known in financial circles as the wall of money' problem (cf. Engelen et al., 2010a, 2011). Inevitably, some capital will not realize itself and will hence be devalued or destroyed. This generates a fundamental uncertainty about the profitability of capital. Consequently, capitalists who are better informed about which segments of capital will eventually realize themselves with a surplus, will incur a lower uncertainty than others. Lower uncertainty does not imply calculated risk, and therefore participating in the capital allocation game on the basis of lower uncertainty is still an unpredictable affair (cf. Engelen et al., 2010a; Wainwright, 2012). However, if this knowledge about lower uncertainty is derived from a structural dominant position in circuits of value, it allows the actor to sell relative certainty of capital realization' for a fee, offloading the risk of the actual investment to the client. This fee is essentially a form of rent, since it is incurred regardless of capital realization (Mandel, 1972 [1975]: 192; Marx, 1894 [1991]: 785; Walker, 1974). These surplus- or superprofits (Marx, 1894 [1991]) will not dissolve as long as there is overaccumulation combined with knowledge asymmetries about potential surplus value realization. The structural dominant position in circuits of value' from which these knowledge asymmetries are derived, is not the exclusive property of one single actor, but emerges from the combined activities of a class of actors (Swyngedouw, 1992). As an abstract category, the APS complex holds exactly such a position under the current conditions of overaccumulation. Collectively, the APS complex forms a class monopoly' as their collective knowledge resources allow the appropriation of class-monopoly-rent (Harvey, 1985: 65). This 'class-monopoly rent describes a situation in which the rate of return to a class of providers of a [...] resource [...] is set by the outcome of conflict with a class of consumers of that resource' (Harvey, 1974: 239)2. Whether that rent is actually incurred by the class-monopoly is contingent on the socio-spatial relations within the APS complex. The APS class monopoly involves a strong spatial expression, since its underlying structural dominant position in circuits of value draws on a network of localization economies where the right combination of people and information can be converted into knowledge about potential surplus generation (Amin and Thrift, 1992; Taylor, 2000). The effects of this localization economy reverberate throughout the cities that form its main nodes and provide it with structured coherence (Harvey, 1985: 125-164, 2005 [2006]: 102-103), as urban land and labor markets, politics and growth regimes tend to co-evolve with the prevalent accumulation logic. The system of interconnected localization economies reveals itself as the particular geography of the WCA (Taylor, 2004), while the salience of this structured coherence can be observed in its main nodes (Sassen, 1991 [2001]; Massey, 2007; Lizieri, 2011). The notion of 'class monopoly' should, however, not be confused with the class distinction that stems from the organization of production and the division of labor (Harvey and Chatterjee, 1974: 36). Neither does a class monopoly imply that the APS complex has to be considered a unitary actor, as different actors within the monopoly alternately cooperate and compete for their piece of the pie (Harvey, 1974, 1985). The existing literature on APS firms under globalization discusses how a variety of socio-spatial practices, which crucially depend on face-to-face contact and tacit knowledge transfer, are deployed to manage knowledge across borders (e.g., Beaverstock, 2004; Morgan, 2001; Morgan and Quack, 2006). These strategies range from temporary detachments and expatriation to the development of transnational business communities both inside and outside the firm. The community concept suggests transnational social groups that hinge on a common set of business and media sources and a shared institutional space for professional education (Hall, 2009). Notwithstanding internal strife, then, the exploitation of this class monopoly relies on a shared interest of the complex that can resembles a fraction of capital (cf. Jessop, 2000). This is a situation of oligopoly that Schumpeter (1928) called correspective competition' and was explicitly attributed to the financial sector and its sustained high profits just prior to the crisis (Crotty, 2008: 170). In the context of world city research, a similar argument of capitalists actively attempting to subdue market competition by establishing an anti-market monopoly position was first brought up by Braudel (1982) and was elaborated by Arrighi, (1994 [2010]: 10, 21) and Taylor (2000). 2 Class Monopoly Exploitation and Reproduction through APS PracticesHaving reasoned the emergence of the APS class monopoly in an abstract way, this section theorizes the associated command and control position from the practices within the APS complex in the WCA that exploit and reproduce that position. In our view, the APS complex' class monopoly emerges from the interplay of three distinct processes or 'elements' at the juncture of conceptual spaces of production and finance (Figure 1). These conceptual spaces can be understood through the various moments of capital in the accumulation process; i.e. the classical M-C-M' formula, Marx (1867 [1976], 1885 [1992]) that can be disaggregated and spatialized (Lee, 1989). Four distinctive moments in such a circuit of value can be identified that elucidate the functions of command and control: (i) the origination/pooling of capital (M), (ii) the transformation of respectively capital into commodities (M-C) and (iii) commodities into expanded capital (C-M'), and (iv) the optimization and multiplication' of the surplus (M'). This formula can be read in terms of two ideal-type spaces: production space typifies the industrial and commercial circuits of capital, which are driven by the maximization of capital accumulation through the process of finding the optimal combination of labor and capital in production on the one hand and allocation to the most profitable markets on the other. The modus operandi of this space has been greatly influenced by the challenges and opportunities of globalization in terms of coordinating global production (Henderson et al., 2002). Financial space, on the other hand, explains capital accumulation through the maximization of returns on credit that even if only in the very last instance - has been extended to the production circuit (Labban, 2010). The workings of financial space itself have profoundly changed by the globalization and virtualization of financial markets and the growing proliferation and trading of debt products and derivatives. Both spaces ultimately reflect perspectives, or windows', on the same process of capital circulation (Marx, 1885 [1992]). Both spaces also crucially depend on knowledge-producing practices by the APS complex that drives a clear-cut tendency towards the further agglomeration and urbanization of capital in world cities (Krätke, 2014; Sassen, 1991 [2001]). Figure 1 A conceptual overview of the elements driving world city archipelago formation