GaWC Research Bulletin 323 |

|

|

|

This Research Bulletin has been published in Die Erde, 140 (4), (2009), 371-390. Please refer to the published version when quoting the paper.

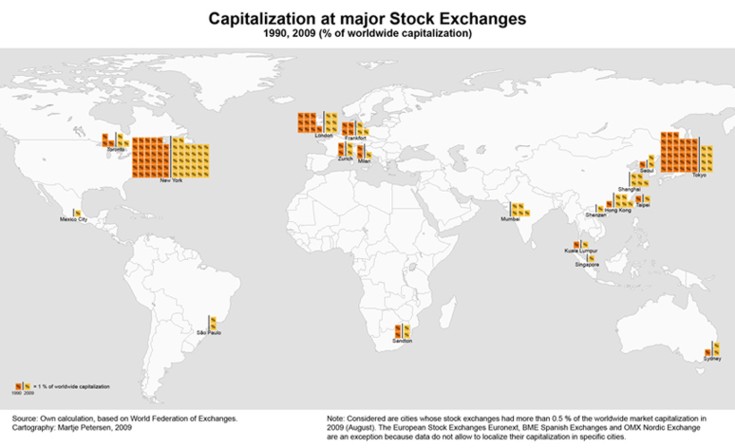

Introduction: On the problematic use of the term 'megacity'The intention of this article is to assess the role of megacities in Latin America (and in other poorer regions) in the world economy. For that purpose it is mandatory to address right at the beginning two major problems associated with the term megacity' and its common use. Firstly, a megacity is strictly quantitative defined according to United Nations (2008), megacities have at least 10 million inhabitants. However, since the World Urbanization Prospects does not provide a rationale for determining the threshold (nor do other authors, suggesting that five [e.g. Mertins 2009] or eight million [e.g. Davis 2006] inhabitants make a megacity) there is little if any explanatory power attached to the category megacity'. Has anything changed in Istanbul in recent years due to the crossing of the 10 million-line? Do any disparities between the megacity Lagos and the non-megacity' Chicago stem from the difference in population size? Do Los Angeles and Rio de Janeiro have, except for the size of their respective population, enough in common to be qualified in the same category of cities? Despite the claim that 'mass matters' (IGU Megacity Taskforce), researchers writing on megacities do not provide answers to these and similar questions. The mainstream literature does not seriously engage neither with Simmel's (2006 [1903]) stimulating notion that size makes a difference to the mental life of city dwellers nor with Jacobs' (1970) equally thought-provoking contention that cities are economically vibrant because of the necessity to resolve the many problems resulting from size and density. Thus, the question, whether crossing a certain quantitative threshold makes any qualitative difference in urban development or city life, remains unassessed. Even more problematic is, secondly, that much of the literature on megacities deflects from the quantitative definition in order to add a specific meaning to the term. In urban geography and beyond, megacity' is frequently used as a synonym for problems in big cities in poorer countries. The most popular account in this vein is Davis' 'Planet of Slums', which depicts megacities as 'stinking mountains of shit' (Davis 2006, 138; for a critical review of Davis' book see Parnreiter 2007a). The Megacity Taskforce of the International Geographical Union is, needless to say, much more serious in its investigations and more cautious in its diction. The message is, however, not so different. Megacities are portrayed as 'major global risk areas' (IGU Megacity Taskforce), which are, according to Kraas (2008, 583), 'particularly prone to supply crisis, social disorganization, political unrest, natural and man-made disasters due to their highest concentration of people and extreme dynamics of development'. Of course, big cities (and, in particular, those in poorer countries) face a lot of problems which I do not want to gloss over. The critical point is, however, that it is nowhere explicitly discussed and justified, a) why a purely quantitative term is charged with (mostly) negative connotations, and b) why the now changed term megacity' is applied mainly with reference to big cities in poorer countries. In that context, the shortcoming of not providing a rationale for a specific threshold turns out to be particularly problematic, because the mainstream megacity literature fails to offer a comprehensive, empirically sustained line of reasoning why bigger cities are supposed to be more prone to all the evils listed above. My contention is that such a general claim is both ageographical and ahistorical, because it ignores differences between urban trajectories in space as well as in time. The megacity New York is certainly less vulnerable to supply crisis than the non-megacity Lima, while the megacity Mexico City does in many, if not all aspects better than the non-megacity Ciudad Juárez on the Mexican-U.S. border. In brief: Though the megacity literature stresses that mass matters (in particular to urban problems), it provides neither comprehensive empirical substantiation nor theoretical arguments for that claim. The megacity discourse is even less suited to assess the (changing) roles of big cities in poorer countries in the world economy. Different to the research on global cities (e.g. Sassen 1991; Taylor 2004) 1, which establishes clear indicators to consider the qualitative functions of cities in processes of globalization, the literature on megacities does not offer convincing arguments on how to relate the population size of a city with its specific role in the world economy. Yet, despite this conceptual void, the underlying notion of the mainstream megacity literature is that there is such a relationship, namely the one that big cities in poorer countries are economically powerless. Contrary to this view, my contention is that a city's size and its position in the geography of global economic governance are not necessarily correlated. As a consequence of the widespread neglect of the question, which role (big) cities in poorer countries assume in the world economy (an ignorance that is also common in much of the global city research [for a harsh critique in that sense see Robinson 2006]), our understanding of their functions in the daily production and reproduction of globalization is still very limited. In order to overcome this shortcoming, I will reflect on the position of megacities (I use the term according to the UN-definition) in poorer countries in the geographies of a) stock markets, b) corporate headquarters, and c) the networks of producer service firms. The rationale behind this selection is, that all three elements point to economic epicentres': Market capitalization of stock exchanges indicates where financial revenue-seeking capital is flowing to, corporate headquarters are seemingly the places, where the big' economic decisions are taken and where profits are finally pocketed, and producer services firms play an important role in managing and controlling global commodity chains. My central claim is that Latin America's (and other regions') megacities constitute, despite their peripheral position on the map of stock exchanges and headquarters, critical nodes in global production networks. Taking Mexico City as a case study, I provide evidence for the notion that Latin American megacities are global cities, because key producer services are supplied, which are essential to the functioning of many commodity chains (for a theoretical account on the integration of global city and global commodity chain research see Brown et al. 2010). Thus, Mexico City is a place wherefrom some form of economic governance is exercised, what makes the Mexican capital to a place which has its hand' in the smooth running and shaping of cross-border commodity chains. Despite their peripheral position on the maps of stock exchanges and corporate profits, the megacities in Latin America and other low and middle income areas are therefore gateway cities in current processes of globalization. Geographies of stock markets, corporate headquarters and networks of producer service firmsIn considering the role of Latin America's megacities in the geography of financial markets, I will focus on just one segment, namely the stock exchanges. Though stock exchanges represent by no means the fastest growing sector of financial markets, for the purpose of this article an analysis of their geographically differentiated capitalization is convenient because it offers useful insights into the geography of capital flows and of profits envisaged by investors (see below). Stock markets are heavily concentrated in a few cities. New York is by far the most important centre, with NYSE Euronext (US) and NASDAQ OMX together accounting for 32 per cent (August 2009) of the capitalization of the 51 exchanges around the world (all data from WFE 2009). The next important market places are Tokyo (8.3 per cent of overall market capitalization), London (6), Shanghai (5), Mumbai (4.9), Hong Kong (4.5), Toronto (3.3), Frankfort (2.8), Sydney (2.5) and São Paulo (2.4). 2 Thus, 72 per cent of the worldwide capitalization is reached in only 10 cities, with five being megacites (New York, Tokyo, Shanghai, Mumbai and São Paulo). Three of the Top 10 stock exchanges are located in megacities in low and middle income countries (Shanghai, Mumbai and São Paulo), while the other megacities in Latin America, Africa and Asia have only small, if any, share in the worldwide stock market capitalization (Mexico City 0.7 per cent, Istanbul 0.5, Cairo 0.2, Buenos Aires 0.1) (see figure 1). New York's dominance is rather stable: In 1990 the stock exchanges in this city accounted only for slightly more of the worldwide market capitalization than today (34.9 per cent). Nevertheless, compared to the historical peak in 2001 (52 per cent), the recent years are characterized for New York by a drastic loss in participation in worldwide market participation. Another interesting aspect is that decentralization is discernible over time in 1990, the top 10 cites had 92 per cent of all market capitalization (2009: 72 per cent). This decentralization happened basically at the expense of Tokyo, whose participation dropped from 32.9 to 8.3 per cent. London and Frankfort suffered minor losses, while Asian stock exchanges increased their share in the overall market capitalization. Taken together, the stock exchanges in Shanghai, Mumbai, Hong Kong and Shenzen increased their share in the total market capitalization from 0.9 per cent in 1990 to 15.8 (2009). Yet, São Paulo, too is amongst the stock markets that showed an above average expansion (from 0.1 to 2.4 per cent of the worldwide market capitalization), while Mexico City's stock exchange did not become more important since 1990 (see figure 1). Figure 1: Stock Exchanges

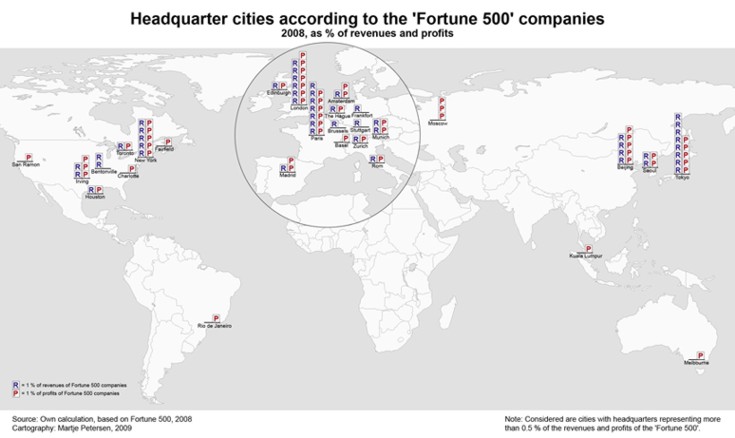

There is also a specific geography to the massive devaluation that occurred in 2008/09. Between May 2008 and March 2009 total market value was halved (all data WFE 2009; according to the WFE, stock markets are recovering since March 2009). Yet, the losses were distributed unevenly. While the two major global centres suffered below average devaluations (in New York, market value dropped by 43 per cent, in Tokyo by 41 per cent), many stock exchanges in non-core countries suffered above average devaluations. São Paulo and Mexico City, where market value was reduced nearly by two thirds, were particularly hard hit. The Chinese stock exchanges, on the other hand, did better (- 42 per cent). Thus, an analysis of the geography of the crisis reveals that the crisis fortified some of the old' centres of the stock markets (an exception is London with losses of 55 per cent), and some of the newcomers', too (Mumbai, however, is with a reduction of 56 per cent among the big losers). Turning to the geographies of corporate headquarters, the discernible pattern is one of centralization, too. The concentration is, however, less pronounced than in the case of stock exchanges (see figure 2). The headquarters of the Fortune 500' in 2008 (Fortune 2009; data refer to pre-crisis times) are distributed over 221 cities, which appears as a rather decentralized allocation. Yet, half of the revenues of the Big 500' were made by companies located in only 20 cities. Tokyo stands out with 48 head offices of corporations accounting for 8.2 per cent of the revenues of the Global 500', followed by Paris (27 / 6.9), London (23 / 5.6), New York (20 / 4.9) and Beijing (21 / 4). It is striking that only three megacities are among the 20 most important headquarter cities. Two of them are located in high income countries' (Tokyo, New York), while Beijing is the only important headquarter city in poorer countries. Though Moscow, Mexico City, Rio de Janeiro, São Paulo, Mumbai, New Delhi and Shanghai also appear on the map of corporate revenues, they account together for only 3.2 per cent of the revenues of the Big 500'. Thus, as headquarter locations for the most important companies, the megacities of the South are, with the exception of Beijing, out of the game. Figure 2: Headquarter cities

The picture changes slightly when profits are regarded. Profits are even more centralized, with the most important 20 headquarter cities housing 214 corporations that account for 53 per cent of the profits of the Global 500'. Secondly, the capital of profits' is not Tokyo, but London, with 7.5 per cent of the profits made by the biggest companies. Next come Paris (6), Tokyo (5), New York and Beijing (4.7 each) and Moscow (2.7). There are five megacities among the major 20 cities of profits': Tokyo, New York, Beijing, Moscow and Rio de Janeiro. Companies headquartered in megacities in poorer countries (Beijing, Moscow, Mexico City, Mumbai, Rio de Janeiro, São Paulo and Shanghai) account together for 10 per cent of the profits of the Big 500', though only the first two have a considerable share. An analysis of the headquarter locations for the largest 2000 firms as defined by the Forbes Global 2000', which was undertaken by Taylor et al. (2009) yields similar results, which nevertheless differ in some aspects from the findings presented above. According to Taylor et al., Tokyo is the leading command and control centre, followed by New York and the non-megacities London, Paris and Houston (because of the clustering of oil and gas companies). Among the 20 most important cities we find five megacities: Tokyo, New York, Osaka (ranked 8th), Beijing (9th) and Los Angeles (12th). As regards the headquarter locations for the 75 most important financial services firms (banks and insurance), Taylor et al. (ibid.) confirm New York's dominance, while London, Zurich, Paris, Toronto and Tokyo come next. In addition to New York and Tokyo, Beijing is the only megacity on the list of the 20 most important cities, and there is only one more city from low and middle income countries (Saint Petersburg [18th]). Thus, the megacities Shanghai, Mumbai and São Paulo, which have certain weight as locations for stock markets, are not on the map of headquarters of global providers of financial services. It is, however, important to refer to the difference between the locations of headquarters of financial and other producer services providers and their crossborder network of offices. The latter is analyzed by the studies of the Globalization and World Cities Research Network (for a description of the methodological approach see Beaverstock et al. 1999 and Taylor 2004, for data and other resources see GaWC 2009). The most recent analysis of 'the world according to GaWC 2008' (GaWC 2009) shows that New York and London are by far the most connected cities in the world city network, followed by Hong Kong, Paris, Singapore, Tokyo, Sydney, Beijing, Shanghai and Milan.3 There are, thus, four megacities among the most central cities in the world city network (New York, Tokyo, Beijing and Shanghai). As regards the complete list of the 129 alpha, beta and gamma world cities, a glimpse reveals that while of course most world cities have a population smaller than 10 million inhabitants, 18 of the 20 megacities are classified as world cities (see table 1). Only Dhaka and Osaka-Kobe (note well: one poor and one rich megacity!) do not figure in the list of world cities. Table 1: Megacities in the World City Network. Source: GaWC 2009 and additional information provided by Peter Taylor.

For the purpose of this paper this finding is particularly important, because it adjusts the megacity' image created by the dominant discourse. Buenos Aires, São Paulo and Mexico City, for example, which are not (prominently) represented on the maps of stock exchanges or corporate headquarters, are as alpha world cities 'very important world cities that link major economic regions and states into the world economy', while Rio de Janeiro is still an important node, 'instrumental in linking (its) region or state into the world economy' (GaWC 2009). Even cities like Calcutta and Lagos house, according to GaWC, significant capacities to link economic activities in India and Nigeria to the world market. As a consequence, the conceptual separation of mega- from global cities, which is suggested by Bronger (2004, 154f), Kraas (2007, 876f) and others, is misleading. Before addressing this point in more detail, I shall briefly discuss the results achieved so far. Analysis I: Latin America's megacities as locations for stock marketsIn the previous section I have shown that the capitalization of world's stock markets is geographically highly differentiated. From a global perspective, Latin America's stock markets are of little importance, accounting together for only 3.8 per cent of the total market capitalization (or for 12 per cent of the value of the two New York exchanges). The biggest market in Latin America the Bolsa de Valores, Mercadorias & Futuros de São Paulo represents 2.4 per cent of the worldwide capitalization, Mexico City's Bolsa Mexicana de Valores another 0.7 per cent, while the Bolsa de Comercio de Santiago has 0.5 per cent, and the Mercado de Valores de Buenos Aires and the Bolsa de Valores de Lima 0.1 per cent each (own calculations, based on WFE 2009). Though the technical explanation of market capitalization is simple (market capitalization is the number of issued shares of domestic companies and those foreign companies which are exclusively listed on an exchange, multiplied by the respective prices of the shares), the implications of a high or low capitalization are not so clear. Is the uneven geography of stock markets' capitalization an adequate indicator for real' economic power located in specific cities or does it just reflect the bigger bubbles in an overall speculative game'? Does the relatively poor market value of Latin America's stock exchanges reflect poor economic prospects for the region and a subordinate role of major cities in the world economy? Though it is beyond the scope of this article to resume (let alone to deepen) the decoupling debate (which suggests that the financial sector has become detached from the real economy' [see, for example, Huffschmid 2002]), pondering on the role of Latin American megacities in the global stock markets requires at least some understanding of what market capitalization actually means.4 The overall increase in market value (1990 2009: + 378 per cent) reflects a shift of capital from productive investment to the financial sphere. Though this shift was certainly facilitated by technological innovations, the driving force in the growth of market value is not technology. Arrighi (1994, ix f) argues that '(t)hroughout the capitalist era financial expansions have signalled the transition from one regime of accumulation on a world scale to another. They are integral aspects of the recurrent destruction of old' regimes and the simultaneous creation of new' ones'. In Arrighi's reading the increasing capitalization of stock markets results from an overaccumulation crisis, in which surplus capital cannot find profitable investment in the productive sector (that is, it cannot find investment that meets the expectations of investors) and is therefore channeled into financial markets where capital seeks high returns as well as high flexibility through (increasingly short term) investment. Another interpretation of the growing market capitalization (which is not necessarily contradictory to the argument put forward by Arrighi) is that the increase results from changing cultures of capitalism, namely the turning towards the shareholder model. High liquidity (as a result, for example, of overaccumulation) will generate high demand at stock exchanges particularly when companies act first and foremost in order to maximize investors' (short term) interests. Thus, the concurrence of the shift in corporate governance 'from retain and reinvest' to downsize and distribute'' (Lazonick and O'Sullivan 2000, 17), the deregulation of all kinds of markets, and the expansion of market capitalization is by no means accidental. When shareholder value principles become decisive for corporate governance, profit seeking capital will flow into stock markets, what drives the prices for the shares. Yet, t his argument is apt not only to explain the timing of the expansion of market capitalization, but also its uneven geography. Demand for stocks will not only increase when shareholder value principles become critical, it will increase particularly in those places, where the pervasiveness of the shareholder model is strongest. As a result, the geographical differentiation of the capitalization of stock markets reflects different histories and cultures of doing big business, e.g. between the U.S. and Europe. Given that high demand for shares is assumed to drive their prices, the uneven geography of market capitalization also indicates where profit-seeking capital is directed to. Notwithstanding whether the buying of stocks is triggered mainly by the (speculative) search for short term profits or by long term strategic decisions, it always reflects investors' return assumptions. Market capitalization points, therefore, to the reputation of a stock exchange and of the firms listed there. Though this reputation' cannot be equalized with the real' economic performance of the listed firms (let alone the real' value), market capitalization does reflect shareholders' readings of the economy: They invest in corporations which in their opinion are the most promising ones in order to increase the value of the shares. Shareholders' readings of the economy are, of course, not confined to the economic' in a narrow sense (e.g. profits of a company). Rather, the decision to invest might have much to do with the overall, national' business climate and national' regimes of regulation (e.g. those that favour the shareholder value principles). Another aspect of shareholders' interpretation of the economy is that there is a self enforcing dynamic to market capitalization. According to conventional wisdom, high liquidity which is reflected by a high turnover rate of stocks leads presumably to a more accurate stock price than in markets where trading is inert. This on its part will increase demand (because investors trust to buy at real' market prices, which are not distorted by insider trade or political interventions) and hence drive market capitalization. Thus, as an interim result I would conclude that investors' return assumptions (and thus market capitalization) are linked, at least to a certain extent, to the real economy'. Of course, profit-seeking investors may be wrong, as the dot-com and other bubbles have unmistakably shown (and one might pose that the more surplus capital is seeking lucrative investment, the more often they err). Nevertheless, the value of shares has always to be generated in the real' economy (and be it through downsizing of the labor force, which for many workers is a very real' fact), and that is why market capitalization is more than a virtual indicator. It has also very real impacts on urban economies, as has been pointed out by Sassen and others: The concentration of stock markets imply an equally high concentration of financial service firms, what shapes the socioeconomic restructuring of cities, and what gives these cities more centrality in the crossborder networks of the producer service firms. The link between market capitalization and real' economic development is probably best witnessed by the upsurge of the stock exchanges in Hong Kong, Shanghai and Shenzen, which parallels the rise of China to the world's third biggest economy, its seconds biggest exporter and also second biggest recipient of FDI. It is not by accident that the two biggest IPOs (initial public offering; first issuing of shares) in 2009 took place in Shanghai and Hong Kong, with the China State Construction Engineering raising about 50 billion Yuan ($ 7.3 billion) in Shanghai and the Metallurgical Corp. of China raising about 19 billion Yuan ($ 2.8 billion) in Shanghai and further 16 billion Yuan ($ 2.3 billion) in Hong Kong. The sheer volume of the investments shows the amount of surplus capital available in and flowing to China, what cannot be detached from the economic success story of Chinese companies. Following this line of reasoning, the poor performance of Latin America's stock exchanges shows that this region is, probably with the exception of Brazil, out of the game of emerging economies'. The relation between market capitalization and assumptions about the future performance of a certain economy is well illustrated by the development of the Mexican stock exchange. Between the end of 1990 and the end of 1993, when the negotiation of NAFTA nurtured high expectations both in Mexico and abroad, the market value of the Bolsa Mexicana de Valores tripled, and the Mexican stock exchange reached 1.6 per cent of the worldwide market value the highest share the Bolsa Mexicana de Valores would ever attain. In 1994, when NAFTA was enacted, the Zapatista insurrection in the South and, more importantly, the tensions within the governing party PRI, which resulted in the murder of the presidential candidate Luis Donaldo Colosio Murrieta, provoked doubts about Mexico's political stability. The result was an enormous capital flight, a recession, and a crash at the Mexican stock exchange. Contrary to the worldwide expansion of market capitalization in these years, the market value in Mexico decreased by 55 per cent (end 1993 end 1995) (own calculations, based on WFE 2009). Despite the recovery of political stability in the following years, the development of Mexico's economy could not meet the high expectations raised before the enactment of NAFTA. Therefore, Mexico never fully won back investors' trust. Today it is Brazil which is seen as Latin America's great economic white hope, what is reflected in the comparably high capitalization of the Bolsa de Valores, Mercadorias & Futuros de São Paulo. Moreover, this argument that market capitalization mirrors to some extent the real' economic development is backed by an analysis of foreign direct investment (UNCTAD 2009). Data reveal a similar (though not exactly equal) trend: Mexico was surpassed by Brazil as recipient of FDI in the second half of the 1990s, when the São Paulo stock exchange became the biggest market in Latin America. Thus, my answer to the above raised questions, whether the relatively poor market value of Latin America's stock exchanges indicates poor economic prospects for the region and to a subordinate role of major cities in the governance of the world economy, is Yes. Yet, the Yes' is much more firm regarding the overall economic scenario than it is with reference to the role of Latin America's megacities. Here the Yes' has to be qualified by a more in dept analysis (see Analysis III). Analysis II: Latin America's megacities as locations for corporate headquatersIt is common in economic geography and in urban studies to equalize the number of headquarters of major global corporations a city has with the city's worldwide economic power. In such readings of the geography of global economic governance, cities that have few or no corporate headquarters are seen as to be inactive in a global perspective, confined to their roles as national centers of production (see, for example, Alderson and Beckfield 2004; Bronger 2004). If that were true, Latin American megacities were in fact by and large irrelevant to the functioning of the world economy. Only Mexico City and Rio de Janeiro house headquarters of important global players: the state owned oil company PEMEX, 42nd in the Fortune 500' (Fortune 2009), in Mexico City, and the equally oil producing Petrobas, a parastatal company with headquarters in Rio de Janeiro (63rd in the list of the Fortune 500'). Mexico City has three more important global players (the mobile phone provider América Móvil [283rd], the state owned Comisión Federal de Electricidad [408th] and Carso Global Telecom [464 th ], a firm whose only purpose is to hold stocks of telecommunication companies). Rio de Janeiro has, in addition to Petrobas, one further important headquarter (the mining company CVRD, today Vale [235th]), while São Paulo has also one (the holding Itaúsa, ranked 273rd, which controls companies in the financial and real state sectors, as well as the wood paneling, ceramic and metal sanitary, chemicals and electronic). Buenos Aires has no Fortune 500' headquarter. Though I do not agree with the notion that cities with few or now headquarters of the world's biggest corporations are not involved in the governance of the world economy (see section 5), I do acknowledge that the picture drawn above reflects to a certain extent the position of Latin America and its cities in the world economy. The number of transnational corporations registered in a specific country mirrors the strength of the economy in this region because of two reasons. Firstly, because headquarters are, at the end of the day, 'responsible for all the major strategic investment and disinvestment decisions that shape and direct the enterprise' (Dicken 2007, 141), they are the loci wherefrom economic power is exercised. Secondly, transnational corporations so far have not moved their headquarters out of the country of origin (despite their growing global activities in general). Headquarters, thus, seem to be sticky' (Baaij et al. 2004). It is therefore no wonder that while most corporate headquarters are in cities in core countries, peripheral areas such as Latin America have only few. Concordant with this line of reasoning it is no wonder that Chinese cities have made it in the last 20 years into the league' of headquarter cities (with Beijing having 21 of the Big 500' companies, and Shanghai another two). Data presented above are indicative for Latin America's weak position in the world economy in yet another way. The most important Latin American global players are companies active in the primary sector (PEMEX, Petrobas, Vale). Headquarter functions are, thus, confined to products which mirror the typical role of peripheral economies: the export of primary products with low value added. In addition, the picture drawn is instructive because it reveals the importance of current or former public sector enterprises (or some mix of it) among the corporations headquartered in Latin America (PEMEX, Petrobas, Vale, Comisión Federal de Electricidad). The fact that most of the few global players located today in Latin America' megacities are (or have been) state owned companies mirrors the economic policy during the time of import substitution, when nationalization of foreign companies (e.g. in the oil and mining sector) were seen as key instruments for an active commitment to national' economic development. Despite these insights we gain from a geographical analysis of locations for major headquarters, the usual equalization of the number of headquarters a city has with its economic power is fraught with problems. One conceptual flaw I will address later concerns the relationship between firms and cities. Another problem is the frequent mix up of headquarter cities with global cities (see, for example, Coe et al. 2007, 230; Dicken 2007, 141f). Though it is true that the maps of headquarter cities and of world cities overlap, it is important to be accurate about the argument. Global city research does not deal with headquarters nor with economic power in general. Rather, it is concerned with the geography of a very specific input into global commodity chains, namely producer services. The rationale behind this shift of attention to producer services is that the long-established equalization of corporate headquarters with economic power is challenged, while producer service firms are seen increasingly involved not only in the management of global production networks, but also in their control (Sassen 1991). Doubts on the unlimited command and control capacity of headquarters are also raised by the literature on transnational corporations. Dunning and Lundan (2008, 245), for example, assert that if 'the MNE (multinational enterprise, C.P.) is to achieve operational flexibility, yet fully capture the benefits of geographical diversity and the economies of cross-border governance, its organizational mentality will need to shift from one based on a pyramid of vertical control relationships to one based on a network of cooperative and lateral relationships' (for a similar point see also Dicken 2007, 120-123). A shift of economic power away from the corporations' headquarters is also suggested by the emerging literature on transnational private governance (Djelic and Sahlin-Anderson 2006; Graz and Nölke 2008; Sassen 2006, ch. 5). The argument here is that private actors (e.g. rating agencies, institutional investors and global producer service firms) are, backed by national governments, ever more setting and implementing standards, which oblige other firms (e.g. the corporations to which they sell services) to specific habits of doing business. The ongoing global harmonization of accountancy standards, for example, is much more than a technical adjustment of different practices. Rather, by advancing a worldwide synchronization of norms, the global auditing firms promote a shift towards a stronger capital market orientation of companies (Botzem et al. 2007). Alike, it is argued that the increasing financialization of companies influences the ways in which corporations are governed and hence the creation and distribution of surplus in production networks (Milberg 2008; Palpacuer 2008). From these notions follows that, if economic governance is defined as the 'authority and power relationships that determine how financial, material and human resources are allocated and flow within a (commodity; C.P.) chain' (Gereffi 1994: 97), producer service firms are strongly involved in global economic governance. Yet, the claim that producer service firms have an increasing bearing on corporate decision-making is of immense importance if our task is to locate economic governance. In order to achieve a refined analysis of the geography of global economic power, we have to identify first and foremost who actually exercises governance. If it is the lead firm (transnational corporations) in production networks, as assumed by much of the global commodity chains literature (for a review see Gibbon et al. 2008), then our map of headquarter cities (figure 2) would correctly depict the geography of economic governance. If, however, producer service firms have really ever more to do with the shaping of decisions of (big) corporations, than it would follow that the governance of commodity chain is much more decentralized as a focus on headquarter cities suggests. My assertion is that a map of the networks of producer service firms gives a more correct picture of the geographies of global economic governance than the maps of stock markets and of the headquarter cities do. As a consequence, megacities (such as Mexico City, that will be used as case study in the next section) are, just as other not so big cities in poorer countries, important nodes in numberless global commodity chains, because it is from there that crucial producer services are supplied. As a consequence, they are on the map of global economic power. Analysis III: Mexico City in the network of producer service firmsMexico City is, as shown in table 1, an Alpha- world city, whose connectivity in the world city network is comparable to the one of Amsterdam, Chicago or Frankfort. Global city formation is under way since the late 1980s, when Mexico's economy was being redirected towards the world market. As a consequence Mexico City, which in the era of ISI (import substitution industrialization) was developed as the economic epicentre of the domestic market, changed to a hinge between production carried out in Mexico and the world market (for a detailed account on global city formation in Mexico City see Parnreiter 2007). One indicator of this transformation is the sharp decline of manufacturing in the city, while another is the strong growth of producer services. Financial services increased their share in the city's GRP from 9 to 25 per cent (1980 2003), and producer services in general accounted for more than a third of urban production (2003). As a consequence of this growth, Mexico City's share of the national production of producer services had risen to 76 per cent (Sobrino 2000; INEGI 2004). A more detailed analysis of Mexico City's growing producer service sector reveals that there is reliable evidence on forward linkages to economic sectors, which are strongly linked to the world market via FDI and/or exports. Thus, the cluster of producer services in Mexico City delivers to companies firmly integrated into global commodity chains, that emanate in, run through, or end in Mexico (the following draws, if not indicated otherwise, on Parnreiter 2010). An input-output analysis of the Mexican economy (2003) shows, for example, that 60 per cent of the producer services go to three strongly globalized economic sectors: wholesale and retail trade (23 per cent), manufacturing (19 per cent), and the producer service sector itself (18 per cent) (INEGI 2009). These links between economic sectors can be spatialized. In manufacturing, for instance, the (mainly Northern) cities where much of Mexico's export manufacturing is carried out are not at all equipped to manage this production within global networks. Cd. Juárez, for example, has 26.2 per cent of value added in computer and electronic industries and 7.5 per cent in the automotive industry, while only 0.6 per cent of value added in producer services are produced there (own calculations, based on INEGI 2004). Thus, cities that serve as export platforms import the producer services necessary for global integration either from abroad or from Mexico City. Forward linkages of Mexico City's producer service sector are also documented by an analysis of the client structure of global producer service firms in Mexico City. For example, 91 per cent of the publicly traded companies (220 of the 300 biggest firms in Mexico) get their auditing services from the Mexico City office of one of the Big Four' global accountancy firms (Deloitte, Ernst & Young, KPMG, PricewaterhouseCoopers). As a consequence, a considerable number of commodity chains obtain at least one producer service from Mexico City. The state-owned oil producer PEMEX is audited by KPMG, as is the privately-owned cement company CEMEX (3rd in Mexico and 389th worldwide), while the mining company Industrias Peñoles, one of Mexico's major exporters, gets its audit services from Ernst & Young, a firm which also services Teléfonos de México, to which América Móvil (Latin America's biggest mobile phone network provider) belongs. In the automotive industries, Deloitte works for GM, Ernst & Young for Nissan, KPMG for Chrysler, PricewaterhouseCoopers for Volkswagen and Ford, while in financial and insurance services, Deloitte (working for Grupo Financiero BBVA-Bancomer, Grupo Financiero Santander, Grupo Financiero Banorte) and KPMG (Grupo Financiero Banamex, Grupo Financiero HSBC México) have the largest banks as clients. Finally, Wal-Mart, which is responsible for the rapid globalization of Mexico's retail sector, is audited by Ernst & Young. Thus, the question whether Mexico City is a node, from where producer services are fed into production networks can be answered: for auditing this is clearly the case. Mexico City is, thus, one of those nodes where 'specialized services needed by complex organizations for running a spatially dispersed network of factories, offices, and service outlets' (Sassen 1991, 5) are supplied. Yet, what are the implications of this finding for the question of economic governance? Are contributions to the smooth functioning of commodity chains also contributions to their governance? If there are linkages between Mexico City's producer service sector and export oriented companies, what can we learn from that as regards the role of Mexico City in the world economy? Results of my field work in Mexico City corroborate the notion that producer services provided in Mexico City are important not only for the running of global commodity chains but also for their command. Mexico City turns out to be also a place wherefrom some economic governance is exercised, though the influence of producer service firms in Mexico City is in general relatively weak. Nevertheless, auditors and lawyers interviewed agreed that producer service firms in general are increasingly influencing corporate decision-making (though they frequently rejected this notion for the specific service they themselves supply). As Luis Cortés, a lawyer at Holland & Knight (worldwide the 36th biggest law firm, which operates in Mexico jointly with a long established Mexican law firm [Gallastegui y Lozano]), put it: '(Clients come and say), look, we want to put a plant in this place, how is it convenient for us to structure the business? Thus, the one who takes the decision how things should be done, rather would be here, from the (law) firm. That is, the way to do make a deal, to take decisions, if it is not coming from the lawyer's office, I do believe that the one who makes the strategy, it's the partners of the law firm'. Another way of influencing corporate decision making is that lawyers participate in the Board of Directors of big companies. As such, they become part of its administration and hence shape the decisions of the society. E xamples of such a pre-structuring of decisions refer to real estate, tax and labor law issues. While it is arguable that some of these fields are less important (e.g. the decision whether to buy or to lease a plant), the choice of the labor union with which an investing foreign company signs the collective bargaining agreement, or decisions on the benefits workers are granted, have an impact on how resources are allocated (or withdrawn) from the Mexican segment' of a global commodity chain. Though this evidence is still tentative, it shows that not only producer service firms in general have some bearing on their clients' decision-making processes. Rather, some of this governance is exercised from offices in Mexico City. This finding is in line with another result of my research, namely that respondents perceived neither a clear-cut hierarchy between the Mexico City office of their company and the global headquarters nor an only one-way (headquarteraffiliate) communication. The production and diffusion of knowledge in global producer service firms tends to be horizontal, what concurs with the conclusions reached by Beaverstock (2004), Faulconbridge and Muzio (2007) and others. Yet, as to the case of Mexico City, arguments that indicate a rather flat organization of global producer service firms are to some extent thwarted by the also frequent remark of respondents that there is a specific hierarchy in doing businesses, which stems from the client's geography. Thus, what defines the position of the Mexican office of a particular producer service firm compared to other offices of this firm is the place where a client firm has its headquarters, because it is always the partner with direct contact to the client who is in command. Javier Romero Río, partner of Deloitte in Mexico City, states that 'the hierarchy (between offices, C.P.) is not through countries but through the partner who is the head of an account'. For companies investing in Mexico, the responsible partner (of accountancy, legal or real estate firms) might be in New York, London or Hong Kong, while the Mexican partner cooperates. If a Mexican company goes global, then the Mexican partner is in command, with support from partners in other cities. It is precisely this structure of the service firms' global networks that helps to understand the role and reach of Mexico City as a global city. Though at a first glimpse the networks of producer service firms seem to be rather flat, their organizational model implies a chain of command. Though local offices are seen by producer service firms as being essential to do business, the big' strategies are made by the lead partners, which in most cases are located abroad. It is realistic to assume that this division of labor shapes the distribution of value along the chain of producer services the more lead partners an office has, the more deals it will command, and the more revenues it will capture. This obviously brings me back to the map of headquarters, because the number of lead partners an office of a global service provider has depends normally on the geography of headquarters of TNCs. Since there are much fewer companies with origins in Mexico that compete successfully at the world market than foreign firms in Mexico, the Mexico City offices of producer service firms will not often be in command. Despite the high grade of autonomy of the Mexico City offices in conducting business, the economic world order poses serious limitations to the development of governance functions in Mexico City. In a similar vein, the cities with the highest capitalized stock exchanges are those with the highest concentration of financial service firms, simply because this is where the big business' is. If, however, financial service firms have an increasing influence on corporate governance, than many of the 'control relationships based on a network of cooperative and lateral relationships' allude to by Dunning and Lundan (2008, 245) can supposedly be localized in the global financial centres. My conclusion is, thus, that the commonsensical assumption that global cities are centers for both the management of the world economy and its command needs to be qualified (yet not rejected) with regard to non-core global cities such as Mexico City. The influence of producer service firms in Mexico City on the governance of commodity chains depends both on sector- and on firm-specific factors (namely the geographical origin of the firm), and, furthermore, those influences are in general supposed to be weak. It is important to stress, however, that the mentioned chains of command do not exist between cities. Despite the unevenness of the geographies of profits and economic governance, it is not cities that are in power over other cities. Even if o wnership relations between the headquarters of a corporation and its subsidiaries would be wholly transmitted into command capacities (what can be doubted, at least according to the above quoted literature), they would not end up in the power of a city to dominate other cities, because chains of command exist within and to some extent also between firms. Thus, despite all existing differences in the wealth, concentration of economic power, etc., New York does not command São Paulo (see Taylor 2006 for a discussion of the problem of reifying cities). Concluding remarksThe analysis presented here shows, that megacities in Latin America and in other poorer regions are rather marginal places in the geographies of stock markets and of headquarter locations of the world's biggest companies. The picture changes somewhat when we consider the networks of producer service firms, because here all megacities (except two) are firmly integrated. While Buenos Aires, São Paulo and Mexico City are classified as Alpha or Alpha- world cities, Rio de Janeiro is a Beta- world city. In a more in dept-analysis of global city functions carried out in Mexico City, I have provided evidence that there are connections between the world city network and global commodity chains, connections that are created by the flows of auditing, legal and other producer services from firms in Mexico City to companies operating in Mexico and catering to the world market. This supports the notion that Mexico City and other (big) cities in poorer countries are not at all inactive', nonessential to the day by day production of globalization. Rather, they assume global city functions, obtaining their centrality through the provision of producer services for a myriad of commodity chains. I have also argued that Mexico City is also a node wherefrom governance for production networks is exercised, though the scope of both local affiliates of TNCs and of local offices of global producer service firms to influence value creation and distribution along commodity chains is limited. Nevertheless, I conclude with Peter Taylor (2004, 92) that Mexico City is 'a classic gateway [city] of contemporary globalization'. Now, the term gateway' can assume different meanings. Interpreted as interface, gateway city' means that producer service firms in Mexico City act as pivots between the world market and production carried out in Mexico. Thus, the Mexico City offices of the Big Four' global accountancy firms, of global law firms or of banks and other financial institutions help to link specific production sites (the many non-global, but yet totally globalized cities as Cd. Juárez) to other nodes in global commodity chains, and that is why Mexico City is a place where globalization is produced. Gateway' has, however, also the meaning of door' or entryway'. This connotation adds a specific value to the interpretation of gateway as pivot, namely a very critical one. If the term gateway' is used in the sense of entryway', the world system heritage of global city research becomes very obvious. In a seminal text on the 'development of underdevelopment', André Gunder Frank conceptualized Latin America's metropolises as bridgeheads', necessary to organize the South-North transfer of resources: 'Just as the colonial and national capital ( ) become the satellite of the Iberian (and later of other) metropoles of the world economic system, this satellite immediately becomes a colonial and then a national metropolis with respect to the productive sectors and population of the interior. ( ) Thus, a whole chain of constellations of metropoles and satellites relates all parts of the whole system from its metropolitan center in Europe or the United States to the farest outpost in the Latin American countryside' (Frank 1969, 6). Just because Frank did not provide comprehensive empirical backing for his assertion, the notion that cities like Mexico City are strategic places for the organization of uneven development at a global scale is worthwhile to be taken as a guiding hypothesis for further research on the current role of megacities in poorer countries. As argued elsewhere, my own research shows that Latin America's shift from import substitution to the world market, that is, the opening of the domestic markets for imports of goods and capital and the reorientation of production to the world market, went along with a structural transformation of the economic basis of major cities. During this transformation, many cities (Santiago de Chile, for example, provides one of the few examples) lost the capacity to integrate the domestic market in economic as well as in social terms. Available data reveal that economic growth slowed down, that informal work grows at the expense of formalized capital-labor relations, and that real wages stagnate or grow only slowly. As a consequence, the last three decades have been a time of the urbanization of poverty: Today, more than two thirds of poor people in Latin America live in cities (note well, of different population size!). As regards the prospects for sustainable development, the transformation from national centres of production into gateway cities of globalization is, thus, an unpromising change. REFERENCESAlderson, A. S. and J. Beckfield 2004: Power and Position in the World City System. American Journal of Sociology, 109 (4): 811851 Arrighi, G. 1994: The Long Twentieth Century. Money, Power, and the Origins of Our Times. London. Baaij, M.; F. Van Den Bosch and H. Volberda 2004: The International Relocation of Corporate Centres: Are Corporate Centres Sticky? European Management Journal 22 (2): 141-149 Beaverstock, J. V.; R. G. Smith and P. J. Taylor 1999: A roster of world cities. Cities 16 (6): 445-458 Beaverstock, J. V. 2004: Managing across borders: knowledge management and expatriation in professional legal service firms Journal of Economic Geography 4: 157-179 Botzem, S.; M. Konrad and S. Quack 2007: Unternehmensbilanzierung und Corporate Governance - Die Bedeutung internationaler Rechnungslegungsstandards für die Unternehmenssteuerung in Deutschland. Perspektiven der Corporate Governance. In: Weiß, M.; D. Sadowski, U. Jürgens and F. G. Schuppert (eds): Perspektiven der corporate governance. Baden-Baden: 358-84 Bronger, D. 2004: Metropolen, Megastädte, Global Cities. Die Metropolisierung der Erde. Darmstadt Brown, E.; B. Derudder; C. Parnreiter; W. Pelupess; P. Taylor and F. Witlox 2010 / in press: World city networks and global commodity chains: towards a world-systems' integration. Global Networks, Special Issue Coe, N.M.; P.F. Kelly and H.W.C. Yeung 2007: Economic Geography. A Contemporary Introduction. Malden Davis, M. 2006: Planet of Slums. New York Dicken, P. 2007: Global shift: mapping the changing contours of the world economy. London Djelic, M.-L. and K. Sahlin-Anderson 2006: Transnational governance: institutional dynamics of regulation. Cambridge Dunning, J. H. and S. Lundan 2008: Multinational enterprises and the global economy. Cheltenham Expansión, different years: Las 500 empresas más importantes de México. México D.F. Faulconbridge, J. R. and D. Muzio 2007: Reinserting the professional into the study of professional service firms. Global Networks 7 (3): 249-270 Fortune 500 2009: Global 500. Our annual ranking of the world's largest corporations. New York: http://money.cnn.com/magazines/fortune/global500/2008/full_list/, 02/11/09 Frank, A. G. 1969: Latin America: Underdevelopment or Revolution: Essays on the Development of Underdevelopment and the Immediate Enemy. New York Globalization and World Cities Research Network 2009: The world according to GaWC 2008: http://www.lboro.ac.uk/gawc/world2008.html, 04/08/2009 Gereffi, G. 1994: The Organization of Buyer-Driven Global Commodity Chains: How U.S. Retailers Shape Overseas Production Networks. In: Gereffi, G. and M. Korzeniewicz (eds): Commodity Chains and Global Capitalism. Westport: 95-122 Gibbon, P.; J. Bair and S. Ponte 2008: Governing global value chains: an introduction. Economy and Society 37 (3): 315-38 Graz, J.-C. and A. Nölke (eds) 2008: Transnational private governance and its limits. London Huffschmid, J. 2002: Politische Ökonomie der Finanzmärkte. Hamburg International Geographical Union, Megacity Task Force: http://www.megacities.uni-koeln.de/, 02/11/2009 INEGI 2004: Censos Económicos 2004, Aguascalientes. Aguascalientes INEGI 2009: Matriz insumo producto: http://www.inegi.gob.mx/est/contenidos/espanol/proyectos/scnm/mip03/default.asp?s=est&c=14040, 02/11/2009 Jacobs, J. 1970: The Economy of Cities. New York Kraas, F. 2007: Megastädte. In: Gebhardt, H.; R. Glaser; U. Radtke and P. Reuber (eds): Geographie. Physische Geographie und Humangeographie. München: 876-880 Kraas, F. 2008: Megacities as Global Risk Areas. In: Marzluff, J. et al. (eds): Urban Ecology. An International Perspective on the Interaction between Humans and Nature. New York: 583-596 Lazonick, W. and M. O'Sullivan 2000: Maximizing shareholder value: A new ideology for corporate governance. Economy and Society 29: 13-35 Milberg, W. 2008: Shifting sources and uses of profits: sustaining US financialization with global value chain. Economy and Society 37 (3): 420-451 Mertins, G. 2009: Megacities in Lateinamerika: Informalität und Unsicherheit als zentrale Probleme von Governance und Steuerung. Technologiefolgenabschätzung - Theorie und Praxis 18 (1): 52-60 Palpacuer, F. 2008: Bringing the social context back in: governance and wealth distribution in global commodity chains. Economy and Society 37 (3): 393-419 Parnreiter, C. 2003: Global City Formation in Latin America: Socioeconomic and Spatial Transformations in Mexico City and Santiago de Chile. Paper presented at the 99th Annual Meeting of the Association of American Geographers, 4-8 March 2003. New Orleans: http://www.lboro.ac.uk/gawc/rb/rb103.html, 02/11/09 Parnreiter, C. 2007a: Rezension zu: Davis, Mike: Planet der Slums. Aus dem Englischen von Ingrid Scherf. Berlin 2007: http://hsozkult.geschichte.hu-berlin.de/rezensionen/2007-3-079, 01/08/2007 Parnreiter, C, 2007b: Historische Geographien, verräumlichte Geschichte. Mexico City und das mexikanische Städtenetz von der Industrialisierung bis zur Globalisierung. Stuttgart Parnreiter, C. 2010 / in press: Global cities in global commodity chains. Towards a geography of governance in the world economy. Global Networks, Special Issue Robinson, J. 2006: Ordinary Cities: Between Modernity and Development. London Sassen, S. 1991: The Global City. New York, London, Tokyo. Princeton Sassen, S. 2006: Territory, authority, rights: from medieval to global assemblages. Princeton Secretaría de Economía, Dirección General de Inversión Extranjera 2009: Reporte de Estadísticas. México D.F.: http://www.si-rnie.economia.gob.mx/cgi-bin/repie.sh/reportes/selperiodo, 02/11/09 Simmel, G. 2006 (1903): Die Großstädte und das Geistesleben. Frankfurt / Main Sobrino, J. 2000: Participación económica en el siglo XX. In: Garza, G. (ed): La Ciudad de México en el fin del segundo milenio. México D.F.: 162-169 Taylor, P. 2004: World City Network. A global urban analysis. London Taylor, P. 2006: Parallel paths to understanding global intercity relations. American Journal of Sociology 112 (3): 881-894 Taylor, P.; P. Ni; B. Derudder; M. Hoyler; J. Huang; F. Lv; K. Pain; F. Witlox; X. Yang; D. Bassens and W. Shen 2009: The way we were: command-and-control centers in the global space-economy on the eve of the 2008 geo-economic transition. Environment and Planning A 41: 7-12 UNCTAD 2009: Interactive database. Division on Invetsment and Enterprise: http://www.unctad.org/Templates/Page.asp?intItemID=3199&lang=1, 02/11/09 United Nations 2008: World Urbanization Prospects. The 2007 Revision. Highlights. New York World Bank 2009: World Development Indicators Quick Query. New York: http://ddp-ext.worldbank.org/ext/DDPQQ/member.do?method=getMembers&userid=1&queryId=135, 15/01/09 WFE (World Federation of Exchanges) 2009: Domestic Market Capitalization. Paris: http://www.world-exchanges.org/, 02/11/09 NOTES* Christof Parnreiter, Department of Geography, University of Hamburg, Germany, email: christof.parnreiter@uni-hamburg.de 1. I use the terms global city' and world city' as synonyms. Also, I use the terms global commodity chains' and global production networks' as synonyms. 2. It is important to note that in Europe several platforms of exchanges operate (NYSE Euronext [ Europe ] with 6.1 per cent of market capitalization, BME Spanish Exchanges with 2.8 per cent and SDAQ OMX Nordic Exchange with 1.8 per cent). Since it is not possible to break market capitalization at these platforms down according to the stock exchanges in particular cities, they are not considered here. 3. My thanks go to Peter Taylor for providing me with the exact data on connectivity in the world city network. 4. I am thankful to Vanessa Redak for many useful details concerning the principles of stock exchanges. Any misinterpretations are, however, mine.

Note: This Research Bulletin has been published in Die Erde, 140 (4), (2009), 371-390 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||