GaWC Research Bulletin 297 |

|

|

|

This Research Bulletin has been published in Tijdschrift voor Economische en Sociale Geografie, 100 (2), (2009), 260-266. doi:10.1111/j.1467-9663.2009.00534.x Please refer to the published version when quoting the paper.

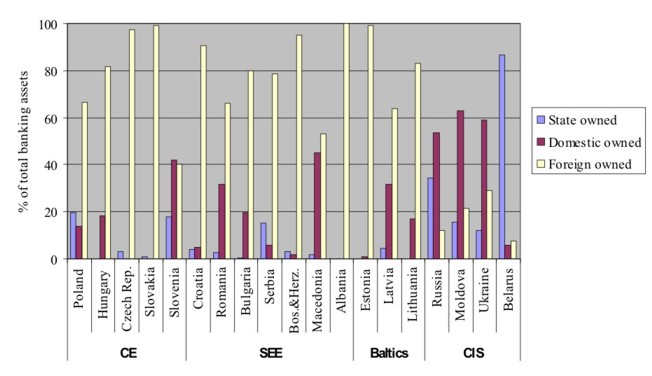

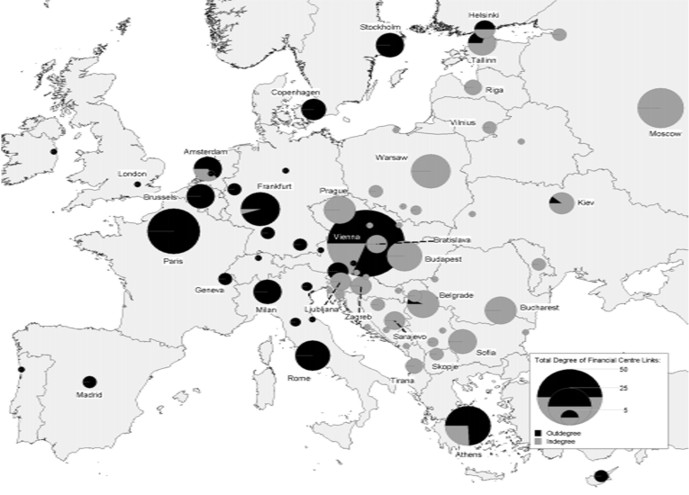

INTRODUCTIONThe heat goes on The subtitle of the latest Central and Eastern Europe (henceforth CEE) banking sector report by Raiffeisen Research (2007) points toward the outstanding prospects for further financial development in the region, and the still ample opportunities for foreign banks to tap into the region's market potential.1 As such, the rise of CEE countries in the global marketplace could not have taken place without rigorous transformations in the financial sector. The key drivers of this transformation process have been the gradual privatisation of state-owned banks and the opening up of the banking sector to foreign investment (Naaborg et al. 2004). As a consequence, most of these countries were able to attract large inflows of foreign investments into the banking sector. Today, over half the number of banks in the CEE region are foreign-owned. Moreover, with a majority of total bank assets, foreign banks have become a predominant factor in the development of the banking system in European transition economies. As a result of the continuous large inflow of foreign investments, new localities of financial importance are being established throughout Europe. Whereas new financial centres emerge in the CEE region, existing centres in Western Europe are reconsidering their market focus. Especially West European cities within close geographical proximity to the CEE (i.e. Vienna, Athens and Stockholm) have been likely to encounter new challenges in improving the competitive position of their financial centres. Unfortunately, ongoing interests in the reconfiguration of European financial geographies are still directed to the core financial centres of London and Frankfurt (Beaverstock et al. 2005; Faulconbridge 2004; Clark, 2002; Grote et al. 2002) or towards a major centre like Amsterdam (Engelen 2007; Faulconbridge et al. 2007). Only a few studies closely examine the spatial implications of the financial sector developments in the CEE region. One recent exception is Wójcik (2007), who provides a detailed case study of the geographical nature of the Warsaw stock exchange activities. Despite minor scholarly interest, sustained progress in the financial sectors of CEE may have considerable impact on the development of European financial geographies for two main reasons. First, while most of the CEE region's developments still take place in the European periphery, the dynamics of the region and the (future) accession of these countries into the EU, both affect the activities performed in the core centres. Second, and probably more important, several of these peripheral financial centres have the potential to become of considerable importance in the near future. The purpose of this study is to examine the contemporary financial geographies in CEE, and building on that, to determine the impact of these geographies on the established financial centre network in Western Europe. To accomplish this, two questions are empirically assessed. First, which financial centres in CEE exhibit sufficient power to attract multinational financial service firms? And second, from where are these investments controlled? As the capital markets in CEE are relatively underdeveloped, firms in need of external funds are still highly dependent on bank credit. Therefore, this paper emphasises the explicit role of banking activities by applying a banking perspective to financial centre development. Before discussing the empirical outcomes of this study, some literature is reviewed on the spatial implications of financial development in transition economies. THE SPATIAL IMPLICATIONS OF FINANCIAL DEVELOPMENT IN CEEThroughout the transition process towards a market based economy, the development of the banking sectors in the CEE countries has been hampered by many difficulties inherited from the system of central planning. Main examples of these difficulties include large stocks of non-performing loans, low savings and investment levels, low productivity, and geographically and sectorally concentrated loan portfolios (Blommestein & Spencer 1994). In order to overcome these problems and instil discipline in the market, most countries gradually restructured, recapitalised, and privatised their state-owned commercial banks and opened up the domestic banking sector to foreign competition and investment (Naaborg et al. 2004). Due to their low level of competitiveness, however, inefficient domestic banks faced the loss of market share and became attractive targets for takeover by foreign financial institutions. Consequently, this situation triggered a surge of foreign investments in the banking sector, causing a true investment and acquisition wave throughout most of CEE over the course of the last decade. Spatial diversity in CEE - Foreign investments in the banking sector are not evenly distributed across the various countries in CEE region. Depending on the degree of financial development - in terms of financial regulation and the general business environment - national or sub-national spaces are maintained (Budd 1995). This indicates that the heterogeneity of the financial and economic conditions across space has serious implications for the investment decisions of foreign financial institutions. When considering national spaces, Figure 1 shows that while foreign-owned firms are dominant in the banking sectors of the CE, SEE and the Baltics (with the exception of Slovenia), foreign presence in CIS countries is considerably lower. This primary difference between CIS and the other regions is caused by the differences in the level of financial development and the regulatory measures adopted by the CIS state authorities to protect their domestic banking sector against international competition. Besides, the high degree of foreign ownership in the banking sector of the CEE countries implies a strong financial dependence on other countries outside CEE. In terms of sub-national spaces, foreign financial institutions obviously try to choose the optimal location to set up their business within a particular country. As the most frequently used mode of entry for foreign banks in CEE is an acquisition (Naaborg et al. 2004), however, these banks are constrained by the locational inertia of the existing office locations and the networks of the acquired banks (see Porteous 1999). As most such domestic banks have a history of state-ownership, their head-office locations were often co-located with the state planning agency and therefore typically concentrated in the financial centre of each country's capital. In addition, foreign banks have the tendency to focus their activities on large borrowers (Berger et al. 2001). In former centrally planned economies these large borrowers are, in most cases, real sector companies with a past of state ownership. Similar to domestic banks, these companies are predominantly located in the capital city. For regions more remote from the financial centre, the high market share of foreign financial institutions in the domestic banking sector may lead to rather constrained credit availability (Dow, 1999). Therefore, sub-national spaces in CEE are determined by specific spatial-economic profiles that still largely result from each country's history as a centrally planned economy. Foreign investments - In an expanding European market, multinational financial institutions are positioning themselves to cope with the increasing pressures of international competition. A primary policy is to search for new strategic markets to increase the geographical scope and market power of the firm (see Dermine 2006). The transition markets of CEE provide interesting new opportunities, especially for those financial institutions within close geographical proximity to the region. Table 1 provides an overview of the investments of the largest foreign investors in the banking sectors of CEE. The ranking is dominated by banks from Western Europe, with the United States' Citibank and Hungary's OTP being the exceptions. Table 1 includes two additional noteworthy details. First, some of Europe's largest financial institutions are not extensively investing in the region. London-based HSBC and Barclays, for example, have only very limited stakes in CEE. The same holds true for Deutsche Bank. Second, Austrian banks are well represented in the top 10. In addition to Erste Bank and Raiffeisen, Vienna's Bank Austria, as a member of the Italian UniCredit Group, is responsible for the activities throughout CEE. The fact that mostly West European financial institutions are investing in CEE indicates a specific role for distance in determining investment decisions. As indicated by Grote et al. (2002), various dimensions of proximity, like cultural, organisational, institutional, or geographical proximity, are among the main determinants of the financial sector's spatial organisation. These different dimensions of proximity are united by the fact that they all reduce uncertainty (Boschma 2005) and, therefore, make it less hard and costly for financial firms to manage the risk profile of an investment project. For financial institutions located within close proximity of the CEE region, it may therefore be more appealing to invest than it is for other multinational financial institutions. FINANCIAL CENTRE NETWORKS: METHODOLOGY AND DATAIn order to examine the contemporary financial geographies in CEE and explore the interregional attachments with West European financial centres empirically, this paper takes up an interlocking network approach. Building on the world city literature (e.g. Beaverstock et al. 2000; Taylor 2001), financial centres are considered to be interlocked by the office networks of multinational financial institutions. Taking up the view that the financial centres are a result of the networks and relations they possess and the flows they produce (Faulconbridge 2004), it becomes easier to understand the role they play in the European system of financial centres. In this context, the power of a financial centre in CEE is not determined by its respective attributes, but by the number of different connections with its West European counterparts (see Taylor et al. 2002), whereby the connections represent the past investments of foreign financial institutions in the centre. In turn, financial institutions located in Western Europe control their investments in the CEE region. The size of the number of investing banks from a particular financial centre is what constitutes the involvement of the centre in the CEE region. This indicates that the emerging centres in CEE are analysed based on a connectivity-through-subordination network' (Taylor et al. 2002). The data sample for the empirical analysis was retrieved from the Bankscope database (2007 edition) provided by Bureau van Dijk, which contains data for about 13.000 banks worldwide. Due to the fact that most of the investments in CEE by foreign financial institutions are performed through a stepwise acquisition, it can become difficult to distinguish whether an office is a true subsidiary based on the degree of ownership. Therefore, only CEE offices in which a foreign investor had a direct or indirect ownership of 50 percent or more are included. Furthermore, as the analysis is limited to the banking sector, the sample is restricted to foreign subsidiaries of multinational financial institutions classified in Bankscope as commercial banks, savings banks, cooperative banks and medium/long term credit banks. Finally, the parent bank had to be European, with its headquarter located outside CEE, and with subsidiaries located in CEE. RESULTS: CITY CLUSTERS IN BANKINGFigure 2 provides an overview of the total degree of financial centre connectivity in Europe. The main findings are fourfold. First, banks headquartered in Vienna play a crucial role as foreign investors in CEE. These investments are predominantly from Austria-based banks, but as indicated by the relatively large indegree of financial centre links, financial institutions headquartered in other West European centres use their Vienna subsidiary as a gateway to CEE. Second, alongside Vienna, the financial centres which host the most investors in CEE are Paris, Athens, and Frankfurt. Interestingly, there are only minor connections between London-based banks and CEE. Third, besides Vienna, Athens, Amsterdam, and Helsinki perform gateway roles to CEE, largely due to (recent) merger and acquisition activity between Western European banks. For example, Crédit Agricole controls its market share in Albania, Bulgaria and Romania through the acquired Emporiki Bank of Greece headquartered in Athens, while Danish Danske Bank acquired Sampo Bank from Finland including its CEE subsidiaries, which are still directed from Helsinki at the time of writing. Fourth, the financial centres in CEE with the highest number of foreign investors in banking are, in descending order, Moscow, Warsaw, and Budapest. These findings are hardly surprising as they largely correspond with the outcomes of Taylor & Hoyler's (2000) research on the spatial order of European cities in terms of corporate service complexes. While Figure 2 makes clear which financial centres in CEE have sufficient power to attract foreign investments into the banking sector, Figure 3 explicitly shows from where these investments are controlled. The parent-subsidiary network shows a distinct spatial configuration of financial centres organised around three main city clusters: a SEE-cluster controlled by Athens, a CE-cluster controlled by Vienna and a Baltics-cluster controlled from Copenhagen and Stockholm. In addition, Paris, Frankfurt, Brussels, and Milan host a large number of investors, but these do not concentrate on a particular cluster of regions in CEE, though Paris has explicit linkages with Moscow and Kiev - the main financial centres in CIS. CONCLUSIONSWhile the literature on the dynamics of European financial geographies is burgeoning, little attention has been directed to rapid (financial) developments in CEE. In this paper it is shown that the financial sector developments in CEE are largely dependent on the investments made by financial institutions from Western Europe. This indicates that a further rise of CEE will most probably also affect the dynamics of established European financial geographies, not only in the peripheral but, if growth continues, eventually also in the core financial centres. The empirical analysis shows that the contemporary foreign involvement in the banking sectors of CEE is predominantly controlled by neighbouring countries. Stockholm, Vienna, and Athens, for example, host the headquarters of large investors in the Baltics, CE, and SEE, respectively. Although these financial centres are still considered peripheral, their strategic position in adjacent regions may enhance their competitiveness as financial centres in the future. Vienna, which performs a central role as financial service provider to CE, may especially profit in terms of competitiveness as the heat goes on' in CEE. REFERENCESBEAVERSTOCK, J.V., M. HOYLER, K. PAIN & P.J. TAYLOR (2005), Demystifying the Euro in the European Financial Centre Relations: London and Frankfurt, 2000-2001. Journal of Contemporary European Studies 13, pp. 143-157. BEAVERSTOCK, J.V., R.G. SMITH & P.J. TAYLOR (2000), World City Network: A New Metageography? Annals of the Association of American Geographers 90, pp. 123-134. BERGER, R.A., L.F. KLAPPER & G.F. UDELL (2001), The Ability of Banks to Lend to Informational Opaque Small Businesses. Journal of Banking and Finance 25, pp. 2127-2167. BLOMMESTEIN, H.J. & M.G. SPENCER (1994), The Role of Financial Institutions in the Transition to a Market Economy. In: G. CAPRIO, D. FOLKERTS-LANDAU & T.D. LANE, eds., Building Sound Finance in Emerging Market Economies, pp. 139-189. Washington: IMF. BOSCHMA, R.A. (2005), Proximity and Innovation: A Critical Assessment. Regional Studies 39, pp.61-74. BUDD, L. (1995), Globalisation, Territory and Strategic Alliances in Different Financial Centres. Urban Studies 32, pp. 345-360. CLARK, G.L. (2002), London in the European Financial Services Industry: Locational Advantage and Product Complementarities. Journal of Economic Geography 2, pp. 433-453. DERMINE, J. (2006), European Banking Integration: Don't Put the Cart before the Horse. Financial Markets, Institutions and Instruments 15, pp.57-106. DOW, S.C (1999), The Stages of Banking Development and the Spatial Evolution of Financial Systems. In: MARTIN, R. ed., Money and the Space Economy, pp. 31-48. Chichester: Wiley. ENGELEN, E. (2007), Amsterdamned'? The Uncertain Future of a Financial Centre. Environment and Planning A 39, pp. 1306-1324. FAULCONBRIDGE, J.R. (2004), London and Frankfurt in Europe's Evolving Financial Centre Network. Area 36, pp. 235-244. FAULCONBRIDGE, J.R., E. ENGELEN, M. HOYLER & J. BEAVERSTOCK (2007), Analysing the Changing Landscape of European Financial Centres: The Role of Financial Products and the Case of Amsterdam. Growth and Change 38, pp. 279-303. GROTE, M.H., V. LO & S. HARRSCHAR-EHRNBORG (2002), A Value-Chain Approach to Financial Centres The Case of Frankfurt. Tijdschrift voor Economische en Sociale Geografie 93, pp. 412-423. NAABORG, I., B. SCHOLTENS, J. DE HAAN, H. BOL & R. DE HAAS (2004), How Important are Foreign Banks in the Financial Development of European Transition Countries? Journal of Emerging Market Finance 3, pp. 99-123. PORTEOUS, D.J. (1999), The Development of Financial Centres: Location, Information Externalities and Path Dependence. In: MARTIN, R. ed., Money and the Space Economy, pp. 95-114. Chichester: Wiley. RAIFFEISEN RESEARCH (2007), Raiffeisen Research CEE Banking Sector Report 2007. Vienna: RZB Group. TAYLOR, P.J. (2001), Specification of the World City Network. Geographical Analysis 33, pp.181-194. TAYLOR, P.J. & M. HOYLER (2000), The Spatial Order of European Cities under Conditions of Contemporary Globalisation. Tijdschrift voor Economische en Sociale Geografie 91, pp. 176-189. TAYLOR, P.J., D.R.F. WALKER, G. CATALANO & M. HOYLER (2002), Diversity and Power in the World City Network. Cities 19, pp.231-241. WÓJCIK, D. (2007), Geography and Future of Stock Exchanges: Between Real and Virtual Space. Growth and Change 38, pp. 200-223. NOTES* Bas Karreman, Department of Applied Economics, Erasmus University Rotterdam. Email: karreman@ese.eur.nl 1. In this study, CEE consists of Central Europe (CE), South Eastern Europe (SEE), the Baltics, and the Commonwealth of Independent States (CIS). CE includes Poland, Hungary, Czech Republic, Slovakia and Slovenia. SEE includes Croatia, Romania, Bulgaria, Serbia, Bosnia-Herzegovina, Republic of Macedonia, and Albania. The Baltics include Estonia, Latvia, and Lithuania. And finally, CIS includes Russia, Ukraine, Republic of Moldova, and Belarus.

Table 1: Top-10 largest international banks and their market share in CEE, 2007.

Source: Raiffeisen Research (2007) and local central banks.

Figure 1: Market share of majority foreign-owned banks in CEE, 2007.

Source: Raiffeisen Research (2007) and local central banks.

Figure 2: Degree of financial centre connectivity in Western Europe and CEE, 2007.

Figure 3: Parent-Subsidiary links of West European banks to their subsidiaries in CEE, 2007.

Note: This Research Bulletin has been published in Tijdschrift voor Economische en Sociale Geografie, 100 (2), (2009), 260-266 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||