GaWC Research Bulletin 282 |

|

|

|

This Research Bulletin has been published in Area, 42(1), (2010), 35-46. Winner of the Area Prize 2010 doi:10.1111/j.1475-4762.2009.00894.x Please refer to the published version when quoting the paper.

IntroductionThis paper presents an analysis of the geography of the booming Islamic financial services' (IFS) sector, which provides banking, financial and insurance services based on Islamic religious grounds. The origins of the IFS sector can be traced back to the 1973 energy crisis, after which the oil-producing Gulf States quickly accumulated enormous amounts of capital. As is well known, these excess profits were partly invested through conventional' banks throughout the world (but mainly headquartered in Europe and the United States), but at the same time it laid the basis for a number of new financial institutions and instruments within the region. In the past few years, IFS have also been introduced beyond the Gulf Region, both within the wider Middle East North Africa (MENA) region and in other world regions. This introduction occurred either through product differentiation within conventional' (often Western) banks or through (mainly Gulf-based) Islamic banks that have gone global'. In the latter case, these firms established foreign branches across the world, an evolution that is largely similar to the globalization strategies of the more commonly studied Western banks and business service firms. In this paper, we examine the geography of these globalizing IFS firms with the aim to present an example of a decentred' urban geography of contemporary globalization. To this end, we draw on the methodology developed by Peter Taylor and some of his colleagues of the Globalization and World Cities (GaWC, http://www.lboro.ac.uk/gawc) research group and network. Based on the GaWC methodology, we collected data on the branch locations of the top-ranked IFS firms, and use this information to disclose the main features of the urban geography of this sector. These results are in turn used to shed some light on the conceptual and empirical relations between this IFS-based city network and earlier research on the world city network (WCN) in general and international financial centres in particular. In this respect, the objective of this paper is largely similar to that of Brown et al. (2002). In the latter article, the authors complement recent research on globalized urbanization through an analysis of how cities in Central America, a region beyond' the commonly identified WCN obtain their global business services, and are thereby linked to the wider global economy. It can be said that a focus on IFS results in a related analysis for the Gulf region, in that cities such as Manama and Dubai, which do not commonly feature in conventional world city rankings, are major nodes in the networks of such firms. As a consequence, this paper can be thought of as an analysis of how the Gulf is integrated in the WCN through its provision of a specific type of business services. The remainder of this paper is organized as follows. In the next section, we discuss how a global urban analysis of the IFS sector may help rectifying a number of limitations of previous WCN research. After a brief overview of the major features of IFS, we briefly outline the GaWC methodology that has guided our data collection. Based on information on the location strategies of 28 major transnational IFS firms in 64 cities across the world, we then provide a detailed assessment of the urban geography of the globalizing IFS sector, after which the paper is concluded with a discussion of the main consequences and implications of this analysis. Decentring the world city network (WCN) literatureThe Sassen/GaWC Framework and its LimitationsAlthough relatively young, the literature on world city-formation is now both broad and extensive in conceptual (Brenner and Keil, 2006) and empirical (Derudder, 2006) terms. One of the most widely cited contributions in this literature is Saskia Sassen's The Global City (Sassen, 1991). In her path-breaking book, she analyses the functional centrality of cities in the world economy. Sassen thereby focuses on the attraction of business service firms (such as firms in accountancy, advertising, banking/finance, law, and management consultancy) to major cities that offer knowledge-rich and technology-enabled environments. A commonly identified limitation of the research drawing on Sassen's conceptualization has been the disproportionate concentration on specific types of economic processes and relatively few large metropolitan centres in the Western world to concomitant neglect of other processes and cities. This problem can, for instance, be observed in some of the empirical GaWC research that explicitly draws on Sassen's conceptual framework. A large number of GaWC's empirical analyses after the seminal Beaverstock et al. (1999) piece have been based on the corporate geographies of 100 leading' business service firms, the so-called GaWC 100' (e.g. Taylor et al. 2002a,b; Derudder et al., 2003) or 175 global' firms more recently (Taylor et al 2009). The criterion for selecting the different firms was different for each of the APS sectors, as Taylor et al. (2002a) explain, but a common criterion was that each of the firms should have a presence in what they dub the three prime globalization arenas': northern America (the USA and Canada), Western Europe and Pacific Asia. This criterion has clearly resulted in a dataset with a very large presence of APS firms with Euro-American origins, so that some of the main conclusions in the GaWC studies regarding the perceived dominance of Western and Pacific Asian cities may well have been a self-fulfilling prophecy. This leads us to ponder how major cities in, for instance, the MENA region are being studied in research on globalized urbanization. Considering these cities through the Sassen/GaWC lens, the conclusion would merely be that cities in the Gulf region are not really well-connected in transnational flows. Beaverstock et al. (1999), for instance, suggest that Istanbul is the only world city' in the Greater MENA region, while seven other cities (i.e. Tel Aviv, Abu Dhabi, Cairo, Dubai, Riyadh, Tashkent, and Tehran) show evidence of world city formation' at best. The more recent and more detailed GaWC 100' study by Derudder et al. (2003), in turn, also features information on the (marginal) position of the likes of Doha, Amman, Tunis and Kuwait City, but still starts from the perspective of how conventional' corporate service firms from the West make (a limited number of) connections to these MENA cities. As a consequence, and in spite of the relative geographical detail in such studies, this research fails to make conceptual linkages to other scales, regions and economic processes, which has led Stanley (2003) to the conclusion that there is a structural knowledge hole regarding the importance of MENA cities in terms of their functional role in globalized urbanization processes. Towards Alternative FrameworksA number of researchers have used these kinds of observations to dissect this particular limitation of the WCN literature in more substantive terms. In our reading, three major critiques have emerged in this context. The first, and perhaps most trenchant critique has been formulated succinctly by Robinson (2002, 536), who complains that equating globalized urbanization with APS-driven urbanization processes implies that millions of people and hundreds of cities are dropped off the map. This exclusion is from two maps': (i) the geographical map of world cities wherein most cities located in the Global South' are missing; and (ii) the conceptual map of world cities which focuses on a narrow range of economic processes (i.e. advanced' servicing of globalized production) so that myriad other connections between cities are missing. Second, and related to this first critique, is the observation that the WCN literature at large has largely failed to transcend its prime scale of interest, i.e. the global'. As Brown et al. (2010) have recently put it: studies of globalized urbanisation need to address leading cities in the global economy to be sure, but there is no need to be ghettoized into a one-process and one-scale analysis. In practice, we are dealing with hierarchically nested urban networks that are built upon ramifications of different urban processes across different scales (see Parnreiter, 2003). Thus, although recent GaWC attempts to analyse the WCN in greater geographical detail have most certainly extended our understanding beyond a limited number of leading cities, these studies have continued to equate Western' practices with global economic processes, and have continued to fail explaining the connection to other scales and regions (Robinson, 2005). Third, and perhaps most substantively, some researchers take issue with the fact that cities outside the West are assessed in terms of pre-given standards of (Western) world city-ness (e.g. Robinson 2002, 531-2). Massey has recently taken up this critique, and thereby urges us to consider additional implications of this neglect of an array of economic processes and a number of regions in the Sassen/GaWC research. She suggests that use of the term advanced' when studying the urban geography of these largely Western business services firms implicitly grants these services (and the firms and the cities that provide them) a normative status. She therefore calls for approaches that expose the hegemonic geographical imaginations and even take the further political step of proposing alternatives (Massey 2007, 24). Gulf Cities and the WCN LiteratureMENA cities in general and Gulf cities in particular have been an obvious victim of the hegemonic world city imaginations highlighted by Massey (2007). One way to put the region on the map is to shift our analysis to the IFS sector, which has recently become a highly integrative force for the Gulf in and by itself, but also in terms of the linkages between the region and the rest of the world. When taken at face value, the world city paradigm does seem to have a tremendous impact on current urban policy and planning in major Gulf cities. Indeed, within the region, world cities located in the Western world often serve as benchmark examples of how cities can flourish as post-Fordist sites that concentrate knowledge and technology (Abdulla, 2006). It may therefore seem reasonable to consider urban changes from the perspective of conventional world city-research. First of all, the alleged spirit of Arab entrepreneurialism' (compare with Harvey (1989) on urban entrepreneurialism) within urban policy is greatly inclined towards the attraction of foreign investments, both in corporate and governmental terms (e.g. the importance of USAID in non-oil economies of the MENA, such as Jordan). This pro-active attitude is most often based on the CEO-like leadership of Arab royalty (e.g. Mohammed bin Rashid Al Maktoum in Dubai) who seem to run their emirates and city-states as large corporations. While the postcolonial state remains the vehicle for political action, cities are increasingly identified as urban growth machines. Second, in terms of mainstream APS connectivity, Gulf Cities such as Dubai and Abu Dhabi have gained importance (see Taylor and Aranya, 2008), indicating that economies in the region are increasingly service-based, very much like city-based economies in the West. Third, the shift to services is clearly evident from the urban tissue, where CBD-like evolutions are getting shape. Thanks to the enormous influx of petrodollars in the last few years, booming' Gulf cities are able to invest heavily in gargantuan infrastructure projects, complete with avant-gardist architecture and state-of-the-art technologies, in a clear move to attract foreign investors. Globalization in the Gulf does indeed drive governments to enhance the image of their cities as a way of marketing' them to the world (compare with Wu 2001, 284). Fourth, massive investments in transportation (e.g. the success-story of Dubai Ports World and the major Airbus orders placed by the Abu Dhabi-based Etihad) and telecommunication infrastructure (e.g. Dubai Internet City) show that urban policy in the Gulf are subscribing them to the idea of a networked economy wherein world cities play a crucial role. Finally, drawing on these evolutions, and very much related to the highly symbolic infrastructural developments, Gulf cities are explicitly subscribing to the idea of becoming world cities'. Taking high-tech, knowledge-based urban economies such as London and New York as an example, urban policy makers in the Gulf region aim to create an instant success-story based on massive infrastructural investments and a simultaneous relaxation of the fiscal and juridical environment. This Dubai model' of urban development, emblemized by its Palm Island, the Burj Dubai (the highest tower up to date) and the World' islands on its coast, has as such become a powerful idea among other Gulf cities such as Abu Dhabi, Doha, Manama, but also elsewhere in the MENA region. Taken together, this may seem to suggest that the standard world city framework is relevant in the context of Gulf cities. However, the growing importance of the IFS sector within the urban developments in the Gulf shows that although cities are subscribing to the world city rhetoric, the actual urban processes are by no means a mirror-image of western world city-ness. Rather, as Robinson (2002, 539) notes, within the Islamic sphere, cultural globalization and integration within the world economy is increasingly mediated through Islamic forms of economic and political activism. As a consequence, a categorizing geography based on western' actors (e.g. global APS firms) runs the risk of being woefully inaccurate or even worse, of being irrelevant for an analysis of contemporary urban processes in the Gulf altogether. Especially in the domain of city/state relations, Western examples of cityness are too narrow to define globalizing Gulf cities such as Dubai, where city, state and business networks are closely intertwined (Sidaway, 2008). It is also becoming increasingly clear that IFS are becoming crucial in these cities. Economic globalization has not resulted in a simple implementation of Western business ethics, but is increasingly mediated through Islamic culture. For instance, the urban infrastructural footprint of world-city formation dominated by real estate giants such as Emaar and Nakheel (who are active throughout the Arab Peninsula) is increasingly financed through the issuance of sukuk (Islamic bonds). By tracking the trail of IFS firms in an exploratory analysis, this paper therefore aims to show that globalization within the Gulf region follows a unique urban trajectory, thereby creating a network of powerful cities that is distinctively different from and denser than previous WCN-studies have suggested. The remainder of this paper is therefore devoted to revealing this other' geography of contemporary WCN-formation. We begin, however, with an overview of the main features of the IFS sector. Islamic financial services: banking, finance and insuranceThe IFS sector provides a host of financial services based on Islamic religious grounds (see Bassens et al., 2011). The origins of the sector are in is a distinct Islamic interpretation of economic development and societal equality. Islamic economics originated in the Muslim world as an ideological paradigm embedded in a context of regional and national struggles for political power and a search for a distinct Islamic' identity (Kuran, 1995, 1997). In essence, Islamic economics was aimed at freedom from colonial rule, exploitation, and oppression through a return to Islam, which stood for the elimination of poverty and the reduction of unequal distribution of wealth (Siddiqi 2007, 99-100). As a modern, all-encompassing model for social, economic, and political life, Islamic economics claimed to be a Third Way and an alternative to Western economic conceptions. It was thought to avoid the inegalitarian excesses of modern capitalism, while at the same time unleashing the energies of entrepreneurs and merchants (Hefner 2006, 17) Based on the prime sources of Sunni Islam (i.e. the Quran and the sayings of the Prophet, called hadiths), Islamic economics started to promote a distinct rationale which prohibits three aspects of conventional interest-based economics: riba (interest), gharar (uncertainty), and maysir (gambling) (see Bassens et al., 2009; Iqbal and Molyneux, 2005). First, perhaps the most important characteristic and certainly the most widely known is the prohibition of raising interest in all its practices. In Islamic thought, time does not equal money. In other words: there is a strong belief that money should not make money by itself. For instance, in the case of a loan, a money lender has no right to earn money simply by lending it to the borrower. Rather, loans or investments are considered from a profit-and-loss sharing view: a money lender can get an extra return in the form of a pre-agreed part of the profits, or take the loss by ratio of the investment. Second, gharar refers to the exploitation that can arise from contractual ambiguities, and its prohibition therefore aims to eliminate or at least minimise this legal risk. Third, maysir bans all kinds of gambling and games of chance, but equally rejects all forms of speculation (which can be thought of as gambling). In addition, other moral standards, such as the prohibition the consumption and production of certain forbidden (haram) products also regulate the functioning of IFS. More generally, IFS should be halal, meaning that they have to comply with the Shari'a, the highest Muslim Law. In line with these prohibitions, the ideal Islamic banking model is based on profit-and-loss sharing on both the asset and liabilities side of the bank, and deposit holders are in fact treated as the bank's shareholders. While there had been some experiments with Islamic modes of finance in rural areas (e.g. in Mit Ghamr, Egypt) in the 1960s, the real rise of the IFS sector can be traced back to the 1973 energy crisis1, after which the oil-producing Gulf states quickly accumulated enormous amounts of capital (see Tripp 2006, 104). This excess income was partly invested through conventional' banks throughout the world (but mainly headquartered in Europe and the United States), but it also resulted in the emergence of a number of new financial institutions and instruments within the region. Despite rather meagre results in absolute terms in the early years, the IFS sector has been rapidly expanding recently, with annual growth rates around 25%. This success has undoubtedly been fuelled [ sic ] by a general Islamic revival', as Islamic banking and finance increasingly came to be regarded as the appropriate' way to do business for Muslims. The IFS sector now has an estimated worth of 639 billion US$ (The Banker 2008, 3). A large part of this recent growth has been due to the success of IFS beyond the Gulf region. On the one hand, this globalization of the IFS sector has occurred through the emergence of new, full-fledged Islamic banks beyond the Gulf (e.g., the Islamic Bank of Britain') or through the establishment of foreign branches of mainly Gulf Islamic banks (e.g., Faisal Private Bank in Geneva, a subsidiary of the Manama-based Ithmaar Bank). On the other hand, product differentiation also occurred within (mostly) Western financial institutions that were already active in Muslim countries, either through branches or through the activities of affiliates. One obvious example includes conventional banks that have decided to offer Islamic products in Muslim markets through so-called Islamic windows' (e.g. HSBC through its subsidiary HSBC Amanah, headquartered in London). Another example relates to Western banks such as Fortis Bank, Barclays, and Deutsche Bank that gained knowledge on Islamic banking and finance in Muslim countries, and started to introduce these gradually in non-Muslim countries. Fortis, for instance, relied on the IFS familiarity of its Malaysian affiliate Maybank for the introduction of its Shari'a compliant fund into the Belgian market in December 2007. In this paper, however, we are interested in the globalization of service provision from the Gulf, and we therefore only focus on full-fledged IFS firms. Methodology and data collectionIn this paper, we draw on the methodology developed by Peter Taylor (2001, 2004) in conjunction with some of his GaWC colleagues for examining city network formation under conditions of contemporary globalization. The basic observation underlying Taylor's interlocking world city network' (IWCN) model is that cities are connected through partner offices of firms. Through the linkages generated by affiliated offices, vital strategic information/knowledge needed for the coordination of its clients' business flows between cities. Connections between cities are thus conceived as the aggregate of such corporate links, and WCN dynamics is therefore primarily an outcome of corporate location decisions by business service firms. Because this IWCN model is central to the research reported in this paper, we briefly summarize its main features. As it is very difficult to measure the actual flows (e-mail traffic and telephone calls, mobility of employees, common projects among offices, reports, etc.) between offices located in different cities, Taylor (2001) starts from the measurement of the institutional structure in which those flows are created and travel around as a proxy for determining the connectivity among the constituent parts. In a first step, this implies recording the presence of a firm in a city, but also estimating the importance of this presence through a standardized service value' vij measuring the importance of a city i to the transnational network of a service firm j. The connectivity measures in the IWCN model are based on various usages of the latter value. The first measure is the site service status Ca of a city, which is simply the aggregation of the service value across all firms: Ca = Σ vaj (1) The actual evaluation of a city's connectivity is based on the calculation of a series of inter-lock relations' rab,j between two cities a and b in terms of firm j. This relation can be computed based on the service values va,jand vb,j for firm j in both cities: rab,j = vaj . vbj (2) The conjecture behind conceiving this product as a surrogate for actual flows of inter-firm information and knowledge is that, drawing on the core ideas of spatial interaction modelling, it simply assumes that the more important the office, the more connections there will be with other offices in a firm's network (Derudder and Taylor 2005, 72-73). The total connectivity Na of a city can be computed through aggregating these inter-city links rab,j across all firms and all cities in the dataset: Na = Σ rab,j a ≠ b (3) For reasons of clarity, and to make this measure independent of the number of cities/firms in the dataset, Na is expressed as the proportion of the highest connectivity in the dataset (i.e., the city with the highest connectivity has a Na of 1). Note that although the Ca and Na rankings will obviously be interrelated (they are both based on the same input data), they are not necessarily the same. This is because they are based on different interpretations of the meaning of the presence of an office in a city. A city assuming a higher position in the Na ranking than in the Ca ranking is relatively more connected to other cities, because firms with a presence in this city tend on average to be part of more extensive office networks. As a consequence, such a city may not boast a lot of offices, but tends to have offices of firms that have a substantial global presence. Following this specification data were required on the office networks of IFS firms that have gone global'. Data was collected in three steps. First, we gathered information on which firms are the main transnational players in the IFS sector. Second, we gained insight in the location strategies of these firms. And third, we standardized the multifarious information on these location strategies by summarizing it in a simple three-point scale. In a first step, we identified the main transnational IFS firms in terms of asset value using The Banker's Top 500 Islamic Financial Institutions' publication (The Banker, 2007). From this list, we selected the top 100 full-fledged Islamic financial firms 2, thus discarding conventional banks with Islamic windows such as Citibank and HSBC as this would bias the results because of their extensive conventional branch network. The Shari'a compliant asset values of the selected IFS firms vary greatly. For example, number one ranked Melli, an Iranian bank, had an asset value of 35 billion US$ in 2007. Second, we collected information on the city-based location strategies of the top IFS firms. The data in The Banker's list only contains information on the country where the firms' headquarters are located. Following the data gathering strategy set in Taylor et al. (2002a), we searched the websites of each of the firms to get a hold of all relevant information regarding their city-centred location strategies, including information on the location of the head office, branches, subsidiaries, affiliates and representative offices (see Figure 1)3.This analysis revealed that 28 out of the 100 leading IFS firms have established one or more offices in a city in another country, whereby a total of 64 cities are connected in the IFS city network in that they host one or more office of these 28 firms. It is the information on these 28 firms and 64 cities that we use in our ensuing analyses (see Table 1). Figure 1: Website searches of IFS firms are used to get hold of all relevant information regarding their city-centred location strategies.

Table 1: Leading IFS firms in terms of asset value (based on The Banker, 2007). Only firms with a transnational presence are listed.

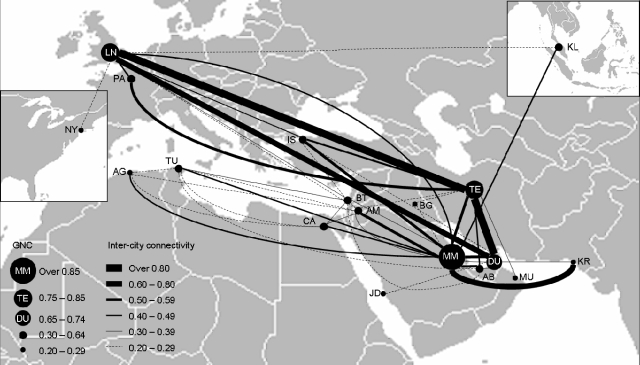

The third and last step involved compiling data on the importance of a given city to a firm's service provision, i.e. assigning the service values vij for each city/firm-pair. We therefore employed a simple, three-point scoring range: a service value of 0 obviously means that there was no office in a given city, a service value of 2 was given to the headquarter city, while a service value of 1 was given to all other offices (i.e. branches, subsidiaries, representative offices and affiliates) in the office network. The end result is obviously less than perfect, but it is the most credible way to describing the office networks of leading globalized IFS firms in 2007 in the absence of large-scale, readily available information on their location strategies. ResultsApplying the GaWC methodology summarized in equations (1) through (3), we derived measures of the cities' site service status Ca and drawing on the aggregated interlock links rab,j across all firms their total connectivity Na. Table 2 presents an overview of the top-ranked cities in terms of total connectivity and site service status in the networks of the 28 transnational IFS firms, in addition to the number of headquarters of the 100 leading firms in terms of asset value. Figure 2, in turn, depicts an overview of the chief inter-city connections in the IFS city network. In this figure, the size of the nodes varies with the total connectivity Na of a city, while the size of the edges varies with the aggregated inter-lock relations rab. For reasons of clarity, only the most important nodes (Na > 0,20) and links (rab > 0,20) are shown. Figure 2: Major inter-city relations in the IFS city network. The size of the nodes varies with the total connectivity Na of a city, while the size of the edges varies with the aggregated inter-lock relations rab. For reasons of clarity, only the most important nodes (Na > 0,20) and links (rab> 0,20) are shown.

Table 2 and Figure 2 provide one of many possible decentred' pictures of contemporary WCN-formation. The basic outline of this IFS city network obviously differs from the WCN identified in GaWC research (which is summarized at length in Taylor, 2004): a lot of traditional' world cities are missing in this network, while new cities have appeared on the map. It is hereby clear that the Gulf region forms the core of the IFS city network. The Gulf States, which are the cradle of the contemporary IFS sector, host the best connected cities with Manama, Dubai and Abu Dhabi in the top 10 in terms of total connectivity. Manama is the undisputed Mecca of the IFS sector: 7 out of 28 globalized IFS firms have their headquarters in Bahrain's capital. Bahrain was the first country where oil was discovered (1932) and it will be the first to run out of oil. The diversification away from oil has been focused on the encouragement of foreign investment, which was considered a means to transform into a financial centre (Hamouche 2004, 530). As such, Bahrain's competitiveness was based on its strategic geographic location, its tax-free environment, its skilled workforce and its overall liberal environment. Perhaps even more important was the quality of its regulatory system: Bahrain was one of the first countries outside the G10 to impose the Basle capital ratios (Warde 2000, 128). The rise of Bahrain as an international financial centre was boosted when international investors left Beirut due to the civil war in Lebanon in 1975. In addition, Bahrain has a long history as Saudi-Arabia's main offshore centre, a relation which is illustrated by the enormous causeway connecting Bahrain to the Saudi mainland. While Bahrain's attractiveness is generally understood in terms of its role as an offshore centre for mainstream' financial services, the fact that Manama is a crucial location for IFS firms can be explained through the presence of an array of organizations central to the development of Islamic finance, including the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), the Liquidity Management Centre (LMC), the International Islamic Financial Market (IIFM), and the Islamic International Rating Agency (IIRA) (Central Bank of Bahrain, 2008). Their presence gives Manama a competitive edge as innovation is crucial in this relatively new and quickly expanding sector. Especially the Bahrain Monetary Agency (BMA) is spearheading IFS: it has Shari'a advisors to help with the auditing of banks and it is developing a new regulatory regime to take in account the special characteristics of IFS (Warde 2000, 129). Dubai is also well-connected in IFS office networks, albeit perhaps less so than could be expected based on its prominent role in other production networks. Since Dubai's oil reserves are almost depleted and while Manama is hoping to become the region's financial centre, the Dubai government has been focused on attracting FDI flows in a wider range of sectors. Still, since the real estate market has been opened up for foreign investment in 2002, the government has encouraged Islamic home financing through its participation in the real estate giants Nakheel and Emaar Properties. Their respective subsidiaries Tamweel and Amlak Finance offer schemes based on Shari'a-compliant finance (Zubairi 2005, 89-91). The enormous demand for assets-based investments has however led to an inflation of real estate prices. Now that the Gulf real estate bubble is bursting the consequences for IFS firms could be dear as well. In addition, IFS firms are still confronted with issues concerning the incompatibility between the Shari'a and the legal environment based on British common law (Caballo, 2007). Among the non-Gulf cities in the MENA, Tehran takes an important position. Similar to Pakistan and Sudan, Iran has a fully Islamic economy', which was abruptly introduced between 1979 and 1982 after the Islamic revolution (Khan and Mirakhor 1990, 358-9). At this time, the entire Iranian banking system was nationalized and an unambiguous model of Islamic banking was adopted and implemented4. Out of the 20 biggest firms in this sector, 8 are headquartered in Tehran. In general, the Tehran-based firms have an extensive network both in Iran and abroad, with offices in the Middle East and Europe. This suggests that although the Iranian IFS were originally embedded in a strong national context, contemporary Tehran-based firms have an extensive border-crossing networked activity, particularly with London and Dubai. Conflicting with the secular character of the Turkish state and its aim to become a member of the Christian' European Union, Istanbul is relatively well-connected, but much less so than could be expected based on it status in conventional' world city rankings. This confirms the observation that the Islamic financial sector is relatively small in Turkey as a whole (personal communication by Eric De Maeyer, Fortis Bank Project Manager on January 23 2008). Although Karachi appears well connected to the Gulf, the Pakistani financial centre, scores surprisingly low in terms of overall connectivity. This is because the intended islamization of the Pakistani banking and insurance sectors (and the economy as a whole) has been postponed. In practice, recent government action has been aimed at the development of a parallel Islamic banking and insurance (takaful) sector alongside conventional banks and insurance companies (Bekkin 2007, 123-4). In Africa, in spite of the fully Islamic character of the Sudanese economy, the latter city is surprisingly weakly connected: Khartoum is only linked in transnational IFS networks through the Al Baraka Banking Group. It should be noted, though, that 4 of the top 100 IFS firms have a headquarter presence in Khartoum, albeit they only have a national office network. In Somalia, in turn, the Al-Barakaat bank has been closed under the pressure of the Bush administration for their suspected financing of terrorist movements (see de Goede, 2003)5. In general, the African part of the IFS network closely follows Muslim presence. Outside the MENA, the American cities, except for New York, are absent from the transnational IFS network. In Europe, cities are relatively well-connected. This is especially the case for London and Paris. Apart from being a major centre for conventional' financial services, London is the major hub for IFS firms outside the Gulf. Although it has only two IFS headquarters of the top 100 firms (i.e. the headquarters of the European Islamic Investment Bank and HSBC Amanah), the city ranks third in terms of site service status and total connectivity. This observation is in line with the intentions of the British government and Islamic finance stakeholders to make London the international centre of Islamic finance. As the chairman of the European Islamic Investment Bank (EIIB, 3, 7) recently declared: I am confident that we are uniquely positioned to benefit from London's position as the leading financial centre in the world as the city positions itself as the global gateway for Islamic finance [ ] We believe that the Bank's competitive positioning is significantly enhanced by its position in London, which is the pre-eminent global financial centre with a robust and highly respected regulatory environment. This observation is in tune with the observations of Faulconbridge (2004), who discusses why financial services remain embedded within International Financial Centres' (IFCs) when technology and myriad globalization processes would seem to facilitate de-concentration and geographical dispersion. As a leading IFC, London is accustomed to its dominant role in Europe, and its dominant position in IFS networks suggest some sort of anchoring of different types of financial services in the same location. Clearly, c ities beyond the Gulf and even beyond the MENA, such as London, are looking to attract and recycle petrodollars by developing opportunities for a sector that is becoming a major force in the oil-exporting economies in the Gulf. East Asian cities are also far less represented in the new archipelago. Kuala Lumpur appears to be the most-connected city, which can in part be traced back to some policies pursued by the Malaysian state, which provides substantial support to the IFS sector. Particularly in the field of insurance it has raised protective policies, such as tax breaks and other legal measures such as the Takaful Act of 1984 (Bekkin 2007, 127). Consequently, Kuala Lumpur has become a hot spot for IFS, acting as a basing point for Middle Eastern IFS firms in the region. Tokyo hosts at present no offices of transnational IFS firms. This can perhaps be traced back to the fact that participation in the Japanese economy still means going through a lot of government channels given a fairly regulated economy (Sassen, 1991). ConclusionsThe overall objective of this paper can be cast in two different forms. First, from the perspective of cities as providers of (corporate) services, we investigated the specific ways in which IFS are being provided throughout the world. Second, from the perspective of WCN research, we have investigated the way in which some poorly connected regions such as the Gulf nonetheless produce/obtain specific, but increasingly substantial amounts of globalized financial services. By putting agency into the hands of non-Western financial agents, we hope to have aided in decentering' some of the overriding geographic imaginations (see Pollard and Samers, 2007), and move away from the problematic dominance of a limited number of economic processes and cities in this research domain (see Robinson, 2002, 2005; McCann, 2004; Massey, 2007). Although our research draws on the methodology of mainstream' world city research, we have shown that a thorough study of IFS firm networks may counter a number of its central limitations. This paper has therefore aimed to i) put the previously understudied Gulf region on the map of urban studies, both geographically and conceptually, ii) shift the focus away from Western' practices in order to provide a more adequate picture of economic globalization processes in the Gulf, and iii) use a mapping of the IFS sector to avoid pre-given standards of (western) world city-ness. The major findings of this analysis can be summarized as follows. First, while cities in the Islamic world are in general well-connected by IFS firms, it is Middle Eastern cities such as Manama, Tehran, Dubai, Beirut, Amman, and Abu Dhabi that are leading the way. Manama is the major IFS hub within the MENA region, but Tehran and Dubai also play an instrumental role in the integration of the MENA region into the global economy, and this mainly through their strong links with London. Second, some key cities outside the Muslim world appear to becoming hot spots for the provision of IFS. London and albeit to a lesser extent Paris are the major examples here, which leads to the more general suggestion that the globalizing IFS sector is becoming anchored in the more conventional world cities and IFCs (cf. also the connectivity of Georgetown on the Cayman Islands and the importance of Manama as an IFC in more general terms). In this context, it seems likely that IFS institutions equally benefit from the agglomeration economies identified by Sassen (1991), so that positive spill-over effects between the Islamic and the conventional financial sector are likely. However, more research is needed to understand why IFS presence in these traditional IFCs is becoming crucial. However, and third, this gradual anchoring of the IFS sector in major world cities does not result in a carbon copy of the traditional IFC-system and the WCN identified in Taylor (2004). Indeed, a number of usual suspects' in the global financial system are only marginally connected (e.g., New York , Frankfurt, and Singapore) or even missing (e.g. Tokyo) in the transnational city networks generated by IFS firms. Finally, this analysis has hinted that although Gulf economies are becoming more integrated in the world economy, the emerging capitalist form is by no means a mirror-image of its western counterparts. Moreover, economics are increasingly being interpreted through the lens of Islam, thereby boosting the tremendous growth of IFS in the Gulf and beyond. At the same time, the dynamics of oil economy and globalization processes have induced highly unique trajectories of world city formation that have largely escaped conventional' world city analysis up-to-date. REFERENCESAbdulla A 2006 The impact of globalization on Arab Gulf States in Fox J W, Mourtada-Sabbah N and al-Mutawa M eds Globalization and the Gulf Routledge, New York 180-188 Bassens D, Derudder B and Witlox F 2011 Oiling global capital accumulation: analyzing the principles, practices and geographical distribution of Islamic financial services Service Industries Journal Forthcoming Beaverstock J V, Smith R G and Taylor P J 1999 A roster of world cities Cities 16 (6) 445-458 Bekkin R I 2007 Islamic insurance: National features and legal regulation Arab Law Quarterly 21 (2) 109-134 Borgatti S P, Everett M G and Freeman L C 2002 Ucinet for Windows: Software for social network analysis Analytic Technologies, Harvard Brenner N and Keil R eds 2006 The Global Cities Reader Routledge, London Brown E, Catalano G and Taylor P J 2002 Beyond world cities: Central America in a global space of flows Area 34 (2) 139-148 Brown E, Derudder B, Parnreiter C, Pelupessy W, Taylor P J and Witlox F 2010 World city networks and global commodity chains: Towards a world-systems' integration Global Networks accepted for publication Caballo A 2007 The law of the Dubai International Financial Centre: Common law oasis or mirage within the UAE? Arab Law Quarterly 21 (1) 91-104 Central Bank of Bahrain 2008 Islamic finance (http://www.cbb.gov.bh) Accessed 1 September de Goede M 2003 Hawala discourses and the war on terrorist finance Environment and Planning D: Society and Space 21 513-532 Derudder B, Taylor P J, Witlox F and Catalano G 2003 Hierarchical tendencies and regional patterns in the world city network: A global urban analysis of 234 cities Regional Studies 37 (9) 875-886 Derudder B and Taylor P J 2005 The cliquishness of world cities Global Networks A journal of transnational affairs 5(1) 71-91 Derudder B 2006 On conceptual confusion in empirical analyses of a transnational urban network Urban Studies 43 (11) 2027-2046 European Islamic Investment Bank 2008 Annual report & Accounts 2006 (http://www.eiib.co.uk/html/index.asp) Accessed 7 April Faulconbridge J R 2004 London and Frankfurt in Europe's evolving financial centre network Area 36 (3) 235-244 Hamouche M B 2004 The changing morphology of the Gulf cities in the age of globalisation: the case of Bahrain Habitat International 28 (4), 521-540 Harvey D 1989 From managerialism to entrepreneurialism: The transformation in urban governance in late capitalism Geografiska Annaler. Series B, Human Geography 71 (1), 3-17 Hefner R W 2006 Symposium: visible hands, religion and the market. Islamic economics and Global Capitalism Society 44 (1) 16-22 Iqbal M and Molyneux P 2005 Thirty years of Islamic banking: History, performance and prospects Palgrave Macmillan, New York Khan M S and Mirakhor A 1990 Islamic Banking: Experiences in the Islamic Republic of Iran and Pakistan. Economic Development and Cultural Change 38 (2) 353-375 Kuran T 1995 Islamic economics and the Islamic subeconomy Journal of Economic Perspectives 9 (4) 155-173 Kuran T 1997 The genesis of Islamic economics: A chapter in the politics of Muslim identity. Social Research 64 (2) 301-338 McCann E 2004 Urban political economy beyond the global' city Urban Studies 41 (12) 2315-2333 Massey D 2007 World City Polity Press, Cambridge Parnreiter C 2003 Global City Formation in Latin America: Socioeconomic and Spatial Transformations in Mexico City and Santiago de Chile GaWC Research Bulletin 103 (http://www.lboro.ac.uk/gawc/rb/rb103.html) Pollard J and Samers M 2007 Islamic banking and finance: postcolonial political economy and the decentring of economic geography Transactions of the Institute of British Geographers 32 (3) 313-330 Robinson J 2002 Global and World Cities: A View from off the Map International Journal of Urban and Regional Research 26 (3) 531-554 Robinson J 2005 Urban geography: world cities, or a world of cities Progress in Human Geography 29 (6) 757-765 Sassen S 1991 The global city: New York, London, Tokyo Princeton University Press, Princeton Siddiqi N 2007 Shari'a, Economics, and the progress of Islamic finance: The role of Shari'a experts in Nazim Ali S ed Integrating Islamic finance into the mainstream: Regulation, standardization and transparency Harvard Law School, Cambridge Massachusetts, 99-107 Stanley B 2003 Going global' and wannabe world cities: (Re)conceptualizing regionalism in the Middle East in Dunaway WA ed Emerging issues in the 21st century world-system Vol I Crisis and resistance in the 21st century world-system Praeger, Westport 151-70 Sidaway J D 2008 Globalising the geohistory of city/state relations: on Problematizing city/state relations: towards a geohistorical understanding of contemporary globalization' by Peter Taylor Transactions of the Institute of British Geographers 33 (1) 149-151 Taylor P J 2001 Specification of the world city network Geographical Analysis 33(2) 181-194 Taylor P J, Catalano G and Walker D R F 2002a Measurement of the world city network Urban Studies 39 2367-2376 Taylor P J, Catalano G and Walker D R F 2002b Exploratory analysis of the world city network Urban Studies 39 2377-2394 Taylor P J 2004 World city network: A global urban analysis Routledge, London and New York Taylor P J and Aranya R 2008 A global urban roller coaster'? Connectivity changes in the world city network, 2000-2004 Regional Studies 42 (1) 1-16 Taylor P J, Ni P, Derudder B, Hoyler M, Huang J, Lv F, Pain K, Witlox F, Yang X, Bassens D and Shen W 2009 The way we were: command and control centres in the global space-economy on the eve of the 2008 geoeconomic transition Environment and Planning A 41 (1) 7-12 The Banker 2007 Top 500 Islamic Financial Institutions November supplement The Banker 2008 Top 500 Islamic Financial Institutions October supplement Tripp C 2006 Islam and the moral economy: The challenge of capitalism Cambridge University Press, Cambridge Warde I 2000 Islamic finance in the global economy Edinburgh University Press, Edinburgh Wu F 2001 China's recent development in the process of land and housing marketisation and economic globalisation Habitat International 25 (3), 273-289 Zaher T S and Hassan M K 2001 A comparative literature survey of Islamic finance and banking Financial Markets, Institutions & Instruments 5 (4) 155-199 Zubairi S 2005 Home finance schemes in the UAE: A case study in Jaffer S ed Islamic retail banking and finance Euromoney Books, London, 88-97

NOTES* David Bassens, Department of Geography, Ghent University, Belgium. Email: David.Bassens@Ugent.be ** Ben Derudder, Department of Geography, Ghent University, Belgium. Email: Ben.Derudder@Ugent.be *** Frank Witlox, Department of Geography, Ghent University, Belgium. Email: Frank.Witlox@Ugent.be 1. The Dubai Islamic bank, the first private interest-free bank, was set up in 1975 (Zaher and Hassan 2001, 169). 2. The nature of the selected IFS firms is very diverse, and includes commercial and investment banks, government-owned banks and development banks, credit and finance institutions and insurance companies. Similar to the more commonly studies conventional financial sector, IFS such as deposits, credit, finance, investment and insurance are increasingly interwoven and provided by one and the same financial institution. We therefore decided to map IFS firms without distinguishing between these specific activities. 3. In the home country no other offices than the head office were considered, because we considered it as normal if e.g. an Iranian bank had 25 branch offices within the Iranian borders. We considered it to be far more important to map the presence of these institutions abroad to get insights in the transnational location behavior of these financial firms. 4. However, as Bekkin (2007, 124) has pointed out, the Iranian economy is not perfectly Islamic as it uses interest-based modes of finance (e.g. Eurobonds) as well. 5. The impact on the Somalian economy has been quite dramatic, given the fact that the bank was a major channel of remittances from ex-pat Somalis.

Note: This Research Bulletin has been published in Area, 42(1), (2010), 35-46 |

|||||||||||||||