GaWC Research Bulletin 258 |

|

|

IntroductionThe strong economic growth and intense territorial transformation of Madrid in the last years must be associated with globalisation processes and the technological change in the new phase of capitalist development (Castells, 1989; Knox and Taylor, 1995; Scott A J, 1996, Méndez, 2001; Sassen, 2003). Like in the rest of great metropolis, the controversy “global city versus capital city” (political, economic, or cultural) does not end with the discussion about the origin of the observed urban growth, but includes the joining mode of the metropolis with the state, with the national economy, and therefore, within the form and contents of new urban governance (Brenner, 1998; Gordon, 2006). Thus, considering the needs and threats of a big city that acts as a “hinge” between the national economy and the global economy, Madrid demands extraordinary competences and resources; for example, to undertake complex infrastructures that try to avoid the strangulation of that growth. It is evident, from different perspectives, the institutional effort of the last years to convince the country of the leading role of the city of Madrid as a global economic actor. Beyond the institutional positioning, sometimes more influenced by City-marketing, previous case studies published over the last decade mainly in the Spanish geographic publications, have concluded that Madrid would be integrated in the world chain of metropolis, although as a city “of second order” or “emergent global city” (see for example, Molina, 2002; Molina and Martin-Roda, 1998; Cordoba Ordonez and Gago, 2002). Given the ambiguous concepts and methodological criteria in these studies this paper returns to the question of global city status of Madrid, following contributions made by the Globalization and World Cities Study Group and Network (GaWC). Specifically, we are following their approach, based on Sassen’s world city thesis (1991), which proposes the study of geographies of advanced service offices considering that it “provides a strategic insight into world city processes by interpreting intra-firm office networks as inter-city relations. In this argument, world city network formation consists of the aggregate of the global location strategies of major advanced producer service firms” (Beaverstock et al, 2000a, p. 5). From this point of view, the general frame of this paper is the “virtuous circle” established between the contribution of ABS to the international positioning of Madrid and the creation of location advantages that the city offers for these activities, including those derived from the international connection of Madrid1. Methodologically, this implies to analyze the status of translational corporations (TNCs) of the sector through the working definition of “global firm” of GaWC (Beaverstock et al, 1999) and also through the field of “foreign firms” in the SABI database2. The first aim of the paper consists on the characterisation of foreign companies in ABS, which a priori seems to be the main protagonists in those global networks of offices. This “profile” of companies is based upon some unpublished statistical sources: a) the so-called Groups Companies (INE, 2003) whose exploitation for the region of Madrid was carried out specifically for this investigation; b) the SABI database, offering information about economic-financial characteristics of companies according to capital ownership. To the best of the authors’ knowledge, these data allows more precise sectoral and spatial details of the city of Madrid that any previous published report. The second aim is to empirically analyze the relation between the performance of the business services companies, measured by a relative efficiency index (Baldwin, 1992), its degree of international connection and its location in the metropolitan region. Despite the interest of the question, it is beyond the aims of this paper, and the possibilities of the statistical sources, a specific analysis of the efficiency determinants. This article is organised as follows. In the second section we deal with recent debates about the development of TNCs in ABS, especially from the point of view of the changing organizational structures and spatial strategies. The third one summarises the main conclusions about Madrid international positioning reported in the international literature. In the fourth section the concentration of ABS at regional level is described, while in the next one a characterisation of the companies in the city is developed, including the exploratory analysis of performance differences, based on a relative efficiency index crossed with some exploratory variables in an answer tree model. Recent contributions on theorizing development and urban agglomeration of transnational corporations in advanced business servicesA good part of the current debate on internationalization of ABS is centred in the transformation of TNCs towards a more “globalized” corporations (Bartlett and Ghoshal, 1989; Dicken, 2003; Jones, 2005), occurring in two inseparable planes: new systems of information and knowledge management and working practices, as well as the so-called organizational space inside and out of organizations. The increased importance of TNCs as global actors have been related to a series of common factors that provide the context for its development (Jones, 2005), updating the traditional debate on the international expansion of advanced services (for instance, Daniels and Bryson, 2002). Briefly, those factors would be structural processes in the new phase of capitalism development (globalization of economic systems, advance of communication and information technologies-ICTs, or the increase in importance of intangible factors); the rising complexity of the client companies organization (as a result of internationalization strategies, manufacturing outsourcing processes, or the introduction of ICTs); as well as the informational nature of this type of activities. In this sense, given the growing uncertainty in the technical, commercial, and regulatory environment, the big firms of international professional services offer their clients strategic knowledge and experience that they do not possess, or cannot exploit without support (Wood, 2002). In order to put that knowledge at the service of the clients, the companies must face cross-border management, one of the key strategies for the TNCs, as we discuss later. From these initial conditions, it would be necessary to discuss about the rationality of the internationalization process. As it is well known, given the property of "non-tradability" of many of these activities, firms have oriented towards those internationalisation forms based on the direct physical presence, especially through affiliates or branch offices abroad (Bryson et al, 2004). The adaptation of the eclectic ownership-location-internalisation (OLI) paradigm (Dunning, 1979, 1985; Dunning and Norman, 1983), originally centred on internalization preferences of multinational manufacturing companies, offers an initial explanation for entry strategies of services based on the combination of three types of specific advantages (Boddewyn, Halbrich and Perry, 1986; Bagchi-Sen and Sen, 1997).

Nevertheless, the OLI model has been recently improved by incorporating the internationalization vectors, represented by different strategies, i.e. cross-border mergers and acquisitions (AM&A), organic growth, strategic networks and alliances, that may change in time and space (Faulconbridged et al, 2008). The “transnational solution” of Bartlett and Ghoshal (1998), a well-known reference on the matter, describes the new management system and the model organization developed by the TNCs to acquire simultaneously global competitiveness, multinational flexibility, and capability of worldwide learning (Table 1). The result is a complex integrated network of the company, characterized by the distribution and specialization of assets and capacities; the differentiation of roles and responsibilities between branches; as well as a simultaneous management of processes of multiple innovation. Table 1. Organizational characteristics

Source: Bartlett and Ghoshal, 1998 (p.75) Although many authors have emphasized the lack of a sequential scheme between the different phases, i.e. multinationals, TNCs, and global companies (Dicken, 2003), it is commonly assumed that the increased “globality” of the corporations goes beyond a simple expansion of the geographic units of production, sale, or consumption, implying emergent forms of connectivity and spatiality (Amin, 2002; Jones, 2005). Indeed, "corporate globalization involves a transformation not just of internal organizational structures or information management and communications systems, but also a wholesale shift in working practices and interpersonal interactions amongst employees within and beyond the boundaries of the firm" (Jones, 2007, p. 224). To understand this global transformation authors have highlighted the question of knowledge, that “whether explicit and/or tacit, and/or embodied and/or embedded, is the key mechanism of value creation within professional services" (Beaverstock, 2004, p.160). In addition, "the key mechanism for knowledge transfer within/between professional services firms is through "face-to-face-contact" with work colleagues, clients, competitors and other actors in society, whether in the work place or other places" (ibid. p.161). Therefore, from this perspective the network of offices becomes the mechanism which, through interaction-socialization process, allows firms to transfer the tacit knowledge within the organization, by means of local personnel or the “expatriated” (Beaverstock, 2004; Jones, 2005). In that sense, equally or more important than the know-how embodied in the highly qualified personnel is the know-who (Lundvall and Johnson, 1994; Glückler and Armbrüster, 2003). Hence, the debate focuses on the issue of the reputation of TNCs that would facilitate the establishment of quality personal interconnections (Aharoni, 2000). The international reputation favours the interests of both the clients which see an increase in the security and effectiveness of decisions (Morgan, Study and Quack, 2006), and the companies that have a superior status granted to them enabling participation in privileged and restricted knowledge thanks to the global presence and the involvement in trust networks of diverse type (Glückler, 2005, 2007). Last but not least, it is crucial to incorporate in this discussion the critical perspective in economic geography within the studies of organization and international management. As Yeung wrote, "space and locations should not be viewed as a passive source of organizational resources "out there" to be exploited by business organizations. Instead, organizational space should be conceived as an active and integral element in structuring the formation, management, and performance of business organizations" (Yeung, 2005, p.221). It is a proven fact that the use of this decision-making scheme entails the reinforcing of certain metropolitan regions. The spatial concentration of ABS cannot be explained only from the traditional model, which relates the agglomeration advantages with the minimization of the cost of transactions, via the geographic co-location of the industrial activities. First of all, the nature of these activities prevents in many cases that the process of value creation can be organized in a sequential chain of activities that would allow a spatial division of the work (Boddewyn, et al, 1986). Moreover, in the specific case of the TNCs its presence in several locations and the existence of internal ties between affiliates, reduce the significance of vertical forward and backward linkages. Despite their increasing importance, as a result of the externalization and internal reorganization of the TNCs, it does not imply the co-presence of its client or providers companies (Nachum, 2000; Glückler, 2007). On the other side, as to the possible horizontal linkages, the increased autonomy and responsibility of the branches facilitates the interaction and collaboration with affiliates and independent local companies, blurring in many cases the limits of the organizational space of TNCs (Nachum, 2000). Two alternative and complementary explanations emerge about the agglomeration tendencies within the sector, largely justifying the approach of this work: the new configurations of organizational space searching for spatial economies, and the appearance of trans-local network externalities derived from the connection to the world city system. Related to the first explanation, it has been argued that the different possible configurations of the organizational space would allow the TNCs to reach spatial economies, defined as economic efficiency and organizational benefits, by using certain spatial strategies (Table 2). These spatial economies, unlike the agglomeration economies, do not imply geographic co-location (Yeung, 2005). Consequently, as Faulconbridge et al. has emphasized (2008), different organizational architectures emerge within the TNCs, trying to take advantage, and also to create, spatial economies and market-making opportunities. Hence, the valuable typology proposed by these authors for the headhunting sector describes three basic types: (i) the wholly owned firm as transnational form managed by an executive board/partnership that defines strategies for all offices, acting as a branch under the same brand name; (ii) the networked firm, as global network formed by several independent firms brought in a strategic alliance; (iii) and the hybrid firm, as a part of a formalized global alliance bringing independent firms together under one corporate name. Table 2. A typology of spatial economies

Source: Yeung, 2005 (p.230) As the second explanation has pointed out, "the world city hypothesis offers an alternative perspective on the urban agglomeration of knowledge services, by focusing on the nodal function of a city in the global network economy" (Glückler, 2007, p. 951). According to the concept coined by Saskia Sassen (1991), global cities are considered privileged places for the production of the central or command functions, necessary for the implementation and management of global economic systems. These functions include not only those that are developed within the company's headquarters, but also financial, legal, accountancy, management functions, etc., frequently subcontracted to the highly specialised service sector. Although partially integrated into the structure of general management of national economy, this subsector can be conceived as part of a network that connects the global cities throughout the world by means of company's representative branches or other offices (Sassen, 2003). Therefore, the point of view of local externalities is overcome when adopting this approach, introducing the positive effect of network externalities associated with the connection with the international system of cities. These advantages of international connectivity would be limited to the city and do not fully apply to the entire metropolitan region (Glückler, 2007, p. 951). In fact, both explanations are not excluding. Thus, some authors, following Johanisson's approach of "economies of overview" (1990), defend the appearance of agglomeration economies for knowledge-based services in big cities, responding to local externalities of the urban milieu; i.e infrastructures, quality of transportation and communications, concentration of sources of information and knowledge, ease to establish professional relations face-to-face, or availability of qualified personnel. However, along with this, a metropolitan location encourages trans-local network externalities (Moulaert and Djellal, 1995); access to extra-regional business opportunities, like global networks of clients and knowledge flows, are aspects that directly affect the efficiency and competitiveness of the ABS companies (Nachum, 1999; Gluckler, 2007). Madrid in the International Studies on World CitiesMadrid in the Global Networks of Advanced Service OfficesAn international frame of reference for the case of Madrid could be constructed following GaWC studies of global networks of offices in services. These studies present methodological differences but a common scheme of analysis (of the individual companies, sectors, and cities) that has been used to synthesise the main conclusions:

Crossing GaWC-100 and SABI: Preliminary Test of Patterns of InvolvementOne of the most decisive contributions of GaWC is undoubtedly the listing of top-100 global business services companies that, following a global localization strategy, have offices in at least fifteen different cities belonging to North America, Western Europe, and Pacific-Asia (Beaverstock et al, 1999). The listing has been crosschecked with the information of SABI on foreign and national companies, as well as with the regional statistics of existing economic establishments, and the companies Websites. This not only allows the evaluation of the representativeness of data handled in this study, it also implies a preliminary approach to patterns of involvement of advanced services in the city's economy (Gritsai, 2004). As shown in Table 3, 34.25% out of the 73 international corporations of global services present in Madrid, operate through foreign filial companies, elevating significantly this percentage among the Insurance, Management consultancy and Banking/Finance sectors. Another 30.14% operate through permanent establishments, either regional offices or international branches, without legal status and dependent on the main company. These would be especially frequent among the Law, Banking/Finances and, rather less, Insurance. Table 3: Global services companies in the city of Madrid

Source: Author's data. At the same time, 23.29% of the international corporations participate in a no majority form in the national companies’ capital, frequently formally integrated in international associations. The strategies in coalition agreements and alliance with local partners seem to be more frequent in Accounting and Advertising. In some cases the association is established with national firms that, having their headquarters in other regions of Spain, also have offices in Madrid. As in the previous case, this allows the international companies the use of network offices of national character that already exist. Since the data of those companies is not included in the enterprise statistics of the city, they are grouped within a last category of non-identified cases (12.33%). In summary, the leading role of foreign companies located in Madrid in the global network of offices is confirmed, especially in activities like Insurance, Management consultancy, and Banking/Finance. In other activities such as Accounting or Advertising, it is also necessary to be attentive to the group of national companies participating and functionally integrated into the global service international companies. For the Law services, mainly managed through international offices, is evident the small representativeness of the source. The Concentration of Business Services in the Metropolitan Region of MadridTwo features help to situate business services in the context of the economy of Madrid. With almost half million employees in 2006, it represents the first activity with approximately 20% of total employment (Table 4). Besides this elevated weight, since the beginning of the decade the business services have grown 64%, well over the average of all sectors (40.52%). Such dynamism, that makes Madrid one of the most outstanding cases in the continent, should be connected with the decisive arrival of FDI flows to the region. Table 4: Advanced business services in the regional economy

Source: Author’s data. According to the last available data, more than 52% of the total of FDI arrival to the Spain between 2000 and 2006, approximately 95,000 million Euros, were directed to companies with social headquarters in the region of Madrid. Reinforcing the general tendency to the tertiarisation of Madrid’s economy, the sectors that received a greater volume of investment in that period were Transportation and Communications (44.20% of the total sectors), Real estate and business services (14.35%) and Financial Activities (9.52%). The concentration of the investment in these two last sectors went up to around 50% of the national total (Table 5). Table 5: Indicators of business services concentration at regional level

Source: Author's data. The behaviour of the FDI has been shaped by the dynamism of the Telecommunications sector, immersed in a liberalisation process that has favoured the fast attraction of strong foreign investment groups at the beginning of the present decade. The increase in the use of ICTs would have caused the arrival of filial multinational services, in which the use of these technologies constitutes one of the pillars of its operation (Fernandez, 2000). The arrival of these important investment flows (in the more frequent modalities of branch creation, participation in company groups, acquisition of Spanish companies, etc.), is directly related to the second indicator selected: the companies that act in Spain under the strategy of international company groups, according to the definition of the Committee for the Statistical Program of the European Union (INE, 2003). Up to 30% of the 21,654 Groups companies are located in the metropolitan region of Madrid, the same percentage than in Catalonia, region that lodges Barcelona, second metropolis of the country and direct competitor within the Spanish and international urban system. However, the greatest concentration in Madrid is observed in Financial Intermediation (56.96% of the national total), Real estate and business services (40.59%), ahead of the rest of activities. On the contrary, Catalonia attracts a greater percentage of the majority of manufacturing activities, except for a few benefited by the effect of headquarters in Madrid, like extractive industries or refined petroleum products, or those that integrate some industrial clusters more representative of Madrid in the last decade, such as Graphic Arts and Electronic equipment (Sanchez Moral, 2008). In addition, the differences in territorial structure of both metropolitan regions have to be considered; in the case of Madrid, company groups located in the central city, whereas in Barcelona they are located outside the city. Similarly, the concentration of foreign companies in the region of Madrid represents 37.14% out of 10,081 firms located in Spain in 2006, growing this percentage significantly up to 60.63% in services of financial intermediation, and 55.56% in business services. At the same time, it is confirmed that almost a quarter of foreign companies of the region are dedicated to the business services, being the sector with greater weight (23.97% of the regional total) over the financial services (5.06%). This initial approach at regional level concludes with some ideas about the final markets of these services. According to Madrid’s input-output system (2002), the percentage of sales within the region fluctuates around 39% in business activities and 45% in financial services. The exportation of business services in general raises up to 60% of sales, concentrating mainly in the rest of national market (51,1%), over the European market (6,8%). In some specialized services, like Business and Management consultancy activities, the national sales decreases notably (42,6%) in favour of the European ones (11,3%). The Foreign Companies of Advanced Business Services in the City of MadridBasic Firms CharacteristicsAccording to Table 6, 566 foreign companies located in the city of Madrid, belong to the three types of advanced producer services (Computer and related activities, Research and Development and Other business activities), thus considered by its major technological intensity and requirements of worker formation (Martinez and Rubiera, 2006). These firms represent more than 75% of all the producer services of the city. As observed at a regional scale, the number of financial intermediation companies (166) is lower than business services firms. This low figure relates to the singularity of the Spanish financial system, adapted during decades to the “protected economy”, limiting the openings of foreign banking; although nowadays in transformation, given the general tendencies of liberalisation, concentration, and internationalisation (Garcia Delgado (Ed.), 2007). Regardless, the vast majority of the foreign banking businesses and other financial intermediation services of the country are located in Madrid, which along with other indicators such as the trading volume of the stock market, make Madrid a financial place at a European scale, only behind those of London, Paris, and Frankfurt. Hence, the increasing frequency of references to the Madrilenian financial clusters (OECD, 2007). Table 6: Advanced business services in the city of Madrid, 2006

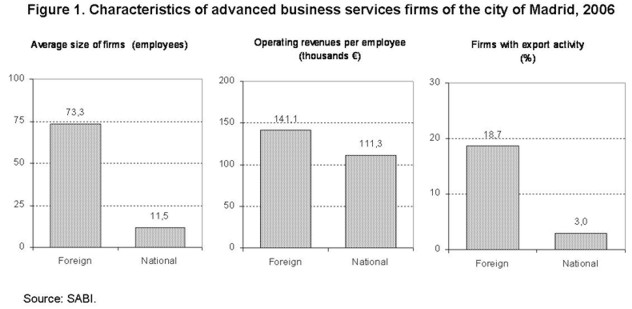

Source: SABI. Nevertheless, the concentration of command functions in Madrid goes beyond these 732 foreign companies. It would be necessary to add certain national firms, as well as the advanced functions developed within the companies’ central headquarters. According to the estimates of the Autonomous Government of Madrid, the region would concentrate 144,265 workers in central business services of direction and administration (68.46% of the national total). The contribution of these central services to the regional Gross Value Added is about 13,149 million of Euros, 77.21% of the value generated in the whole country (Ayet and Sanz, 2004). The comparative study of foreign companies and national companies, excluding financial activities due to statistical difficulties with SABI data (i.e. high percentage of companies without workers, as in the case of non-monetary financial organizations, or the questionable meaning of the export propensity variable, etc.), reveals the existence of marked differences (see Figure 1). Beginning with a bigger average size of the former (73.3 vs. 11.5 workers per firm), as well as the operating revenues per employee (141.07 vs. 111.3 thousands Euros), or the companies with export activity (18.7% vs. 3%). Foreign companies, as well as the national ones, are similarly young, with an average age of about 13 years; more than 40% of the companies were created during the Nineties and another 37% after the year 2000. All the mentioned differences allude to the important presence in the city of big premises of foreign companies of computer or business consultancy (i.e. IBM Global Services, Atos Origin, Accenture, GTronics, Ernst & Young or Price Waterhouse). In this sense, the more numerous group of foreign companies corresponds to Other computer activities (14.34%), followed by Advertising (11.75%), Management of Holding companies (11.07%), and Consultation of computer applications (11.07%). There are many national companies dedicated to the same activities, although in this case with greater numbers in activities of Architecture and Engineering (12.99%), Accountancy (12.97%), Advertising (12.77%), and Management Consultancy (10.28%). The weight of the financial activities, both in foreign companies and national, are placed around 20-23% of the total. In short, the presence of foreign firms approaches 4% of the total companies, with a increasing percentages in Computer services and in the Management of Holding companies, and reducing it in others activities like Accountancy, Legal services, or Architectural and engineering.

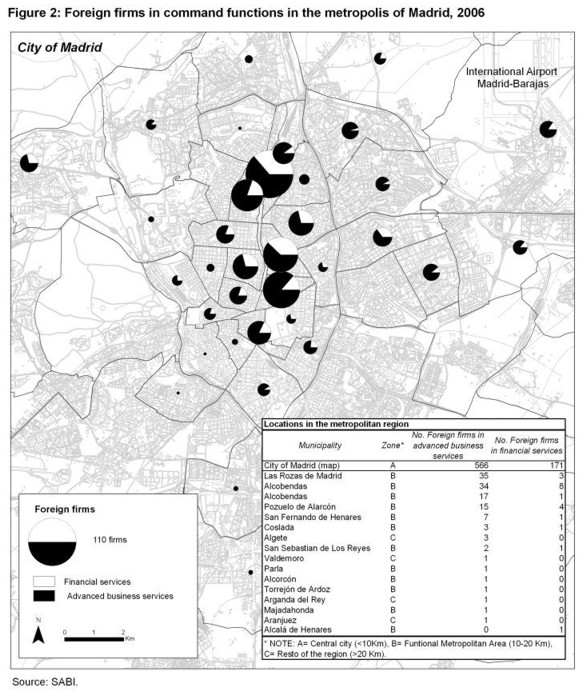

Geography of Command Functions in the Madrilenian MetropolisThe strong spatial concentration of command functions is confirmed. If 70.89% of all the foreign companies in the region have their social address in the city of Madrid, that percentage rises to 82.14% in the case of the ABS, and to 89.52% in the financial services (Table 7). In this sense, the foreign industrial companies present a polarisation degree noticeable lower, as a consequence of the decentralization of productive processes and spatial diffusion that has occurred for decades in the metropolitan region of Madrid (Molina and Martin-Roda, 1998). Hence, the value of the Gini index of the foreign companies in all sectors is inferior to the one obtained for the ABS (GI=0.9936) and financial (GI=0.9967), both above its equivalents within the national companies. Table 7: Concentration of the advanced services in the city of Madrid, 2006

*NOTE: The metropolitan region is formed by 179 municipalities, including the City of Madrid. Source: SABI. The map of regional distribution reflects the acute concentration in the central city (see Figure 2), where companies find the maximum advantages of location associated to the centrality, the existence of a business environment of high density that favours face-to-face contacts and urban spaces of high quality and representativeness. In the rest of the region, the significance of some municipalities in the northern metropolitan area (Tres Cantos and Alcobendas) and in the west (Pozuelo de Alarcón and Las Rozas) stands out. Both dynamic metropolitan zones are benefited by a relative centrality within the metropolis, a high environmental and infrastructure quality, and a very attractive supply of spaces for economic activities under constant renovation, which includes modern business and office parks, technological parks, etc. Inside the central city, the same pattern of spatial concentration is observed, in such a way that only seven postal districts of the capital concentrate almost 55% of all the companies. The major concentrations are observed along the central avenue of the city (Paseo de la Castellana), especially in the northern section where the two main Madrilenian business centres (AZCA and Cuzco) are located. In this Northern axis, there are important new urban projects planned to receive a good part of the city's tertiary command functions, i.e. the business zone of Cuatro Torres Business Area (CTBA), the new corporative city of the multinational Telefonica (District C) and the future financial city of the Bilbao Vizcaya Argentaria Bank.

In the central area of the Paseo de la Castellana, the concentration extends towards some of the residential distrits of higher status, descending progressively towards the south until arriving at the surroundings of the Madrid stock market. Outside of this area, stands the axis that in the eastern direction connects Downtown with the Madrid-Barajas International Airport area, which logically acquires an enormous importance from the perspective of the attraction process for these types of companies. As far as the distribution among financial services and ABS (22% against 78% in the whole region), a significant increase is observed of the former in the capital and some adjacent municipalities. Proving the extreme spatial selectivity within the central city is the fact that only in the axis of La Castellana and the zone of connection with the Airport are concentrated practically 40% of the foreign companies in financial services for the region. International Connection, Metropolitan Location and Economic Efficiency of the Advanced ServicesTo tests the hypothesis about the greater dynamism of ABS that reach a greater international connectivity and, therefore, of those located in world cities, such as Madrid, an analysis in two phases has been developed: (i) Measuring of firms’ efficiency; (ii) Exploring interaction patterns in a set of independent variables. Farrel (1957) is mention as the first to propose comparing the performance of an individual firm with respect to a technical “efficiency frontier”, that could be estimated by means of parametric or non-parametric techniques (Heshmati, 2003). This is the case of the selected relative efficiency index (Ei), based on the partial productivity of the labour factor. Thus, according to SABI data possibilities, this has been calculated as the ratio of the actual output of a specific firm (measured by Operating revenues) and the potential output (estimated by the number of employees in that firm and the Operating revenues by number of employees in the 10% most productive firms within the sector):

This efficiency measure has been defended by Baldwin (1992), as a method more direct although less elegant than those that estimate efficiency from the residuals derived from a production functions. In this sense, the main criticism relates to the reduction from several dimensions of the firms’ performance to only two dimensions, while others procedures, namely the Data Envelopment Analysis (DEA), work with multiple outputs e inputs (Chaners, Cooper and Rodhes, 1978). However, the greater complexity of DEA seems to be justified mainly in those cases where the efficiency differences could be hidden by aggregated sectoral data, which is not our case. There are other reasons for choosing the described method. In the first place, a previous report with the same methodology applied to analyze the efficiency differences of national and foreign manufacturing firms in Spain (Merino de Lucas and Salas Fumás, 1996). Secondly, it is necessary to keep in mind the insufficient number of SABI variables to approach the different inputs of the productivity. This does not represent a problem, since our analysis does not pretend the study of the efficiency determinants but the differences observed according to types of firms. To study these differences is the main goal of the second part of the analysis. The exploring of interaction patterns of independent variable has been solve by means of a Classification Tree model, one of the most popular Data mining techniques. This procedure has been highly recommended when the data does not satisfy the restrictions of traditional parametric methods and/or when the relations between variables are not well known, because it allows hypothesising about these relations (Breiman, et al, 1984). Both circumstances concur in our case. Specifically, the classification tree was constructed here through the CHAID algorithm (Chi-square Automatic Iterated Detection) (Kass 1980), that permits to select the best predicting variables or “predictors” (i.e. employment, activity, operating revenues, exports and location) for the dependent variable (i.e. efficiency index), by means of a sequential cross-tabulation based on Chi-squared test (Table 8). Additional specifications of the model need to be explained. Concerning the so-called stopping-rules, necessary for producing a smaller tree than the exhaustive one, the preset critical level of the chi-squared test (P-value <0.05) is used as principal criterion, but combining it with the number of cases at each terminal node. On the other hand, given the short size of the sample to predict the error through a training sample, the cross-validation of the model is done by observing the improvement of the explanatory capacity with respect to the initial node. Table 8: Sequential merge and split procedure of CHAID algorithm.

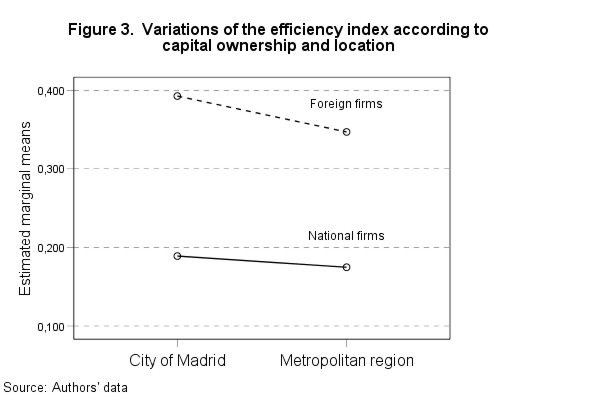

Source: Adapted from Wilkinson1992. The first results relate to the efficiency differences between national and foreign firms, the latter supposedly benefited by synergies originated by their international activity (for instance, experience in external markets, access to different sources of knowledge, networks of clients, etc.). The test of the Student's t for independent samples as well as the non-parametric test5 (Table 9 and 10) allow rejection of the hypothesis that both samples of foreign and national companies have been taken from populations with the same average of efficiency (P-value <0,000). In addition, the existing difference between the marginal means of foreign companies located in the city and in the rest of the metropolitan region, bigger than in the case of national companies (as shown in Figure 3), are not statistically significant. Table 9: Student' s test for mean differences in the efficiency index (Ei)

Source: Author's data. Table 10: Non-parametric test for mean differences in the efficiency index (Ei)

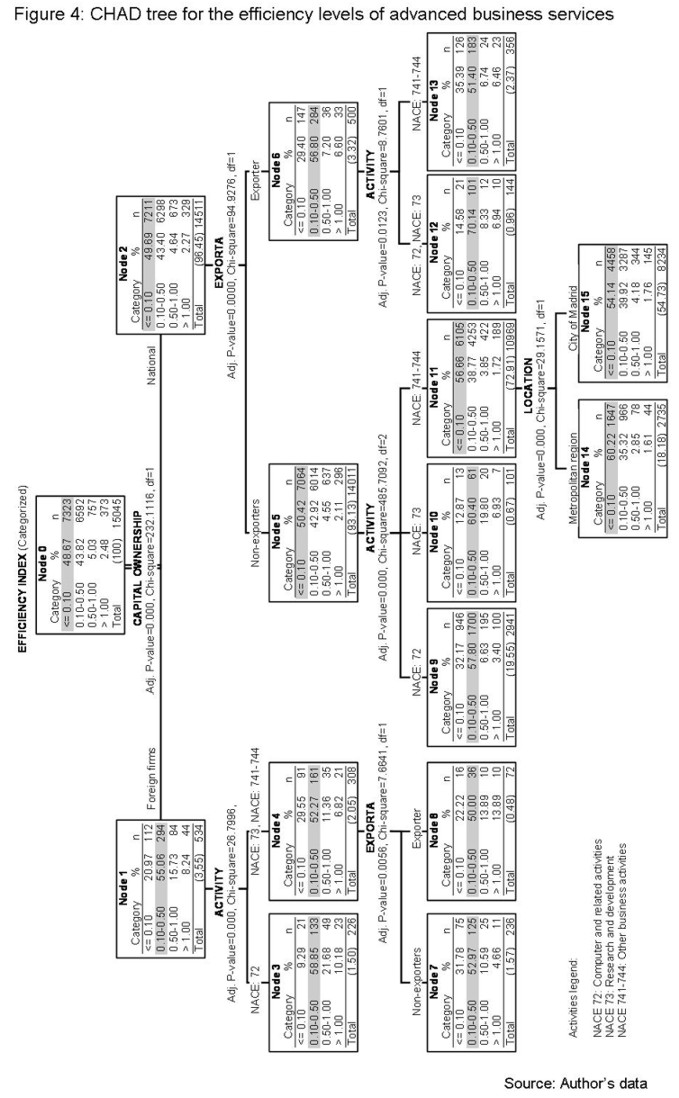

Source: Author's data. The interactions of these variables could be more precisely described by the CHAID tree model previously explained. After several tests two important conclusions are drawn. Firstly, there is an increase of the residual variance of different models obtained because of the strong asymmetry of the dependent variable (Ei index). In order to solve this, the variable has been categorized according to levels of “low” efficiency, between 0 and 0.1 (48.67% of the companies of the sample), “moderate high”, between 0.1 and 0.5 (43.82%), “very high”, between 0.5 and 1 (5.03%) and “extreme”, more than 1 (2.48%). Secondly, the introduction as predictors of the variables “operating revenues” and “employment” used to compute Ei index, improve the predicting capacity of the model, although at the cost of generating trees of a more complex structure. Given the strictly descriptive and exploratory character of this analysis, it is proposed a tree that maintains a relative balance between the increase of the explanatory capacity with respect to the initial node (over 10%), and a relatively simply structure that allows statistical validation of some of the most interesting interactions. The most significant aspect of the CHAID tree in Figure 4 is the explanatory capacity of the variable capital ownership, revealing the highest differences in the distribution of the 534 foreign companies with respect to the 14,511 national companies. Thus, the percentage of foreign companies in the category of low efficiency is 30 points lower than in the national group; it is 10 points higher in the high efficiency category, and it multiplies by more than three and almost four times those of very high and extreme efficiency respectively. In addition, considering the saturation degree of the “criterion category” in the terminal nodes, there are five especially significant segmentations. First, node 3, formed by 226 foreign Computer Services firms (1.5% of the companies), presents the smaller percentage in the category of low efficiency, and the greatest in the very high. Therefore it is confirmed the existing relationship between the dynamism of companies and its international connection, explained initially by the capital ownership. As described below, other evidences point out that the international connection effect can also be benefiting those companies with highest export propensity. The exporting activity is the key criterion in the segmentation of 144 exporting national companies in Computer Services or Research and Development in node 12 (0.96% of the companies). Despite the unequal grouping of sectors, it is evident that the efficiency in national exporters companies grows remarkably, assimilating their behaviour to that of foreign companies. This conclusion, in line with the results obtained in the case of the Spanish industry (Merino de Lucas and Salas Fumás, 1996), confirms the advantages linked with having a greater international connection. Accordingly, there is a general a decrease of the average efficiency in the group of non-exporter national firms. However, in the case of the 101 companies of Research and Development in node 10 (0.67% of the companies), there is a reduction of almost 40 percentage points in the lower efficiency category, and significant increases in the rest of categories. Similar results are obtained in the 2,941 companies in Computer Activities of node 9 (19.55% of the companies). Despite this, the weight in the very high or extreme efficiency categories within this group represents three times less with respect to the equivalent foreign companies. In summary, the relationship between the greater dynamism of ABS and its location in the central city would be statistically significant in the case of those national companies dedicated to activities of more traditional character; initially oriented to the local market (i.e. Architectural and Engineering services, Accounting, Legal, Advertising….). The externalities associated to the urban milieu (market size, geographic proximity to clients, face- to-face contacts, etc.) seem to influence the development of this type of activities. However, in the remainder of activities, either the differences in efficiency found are not as evident, or the shortage in number of cases prevents a statistically significant conclusion.

CONCLUDING REMARKSThe ABS companies are contributing to the improvement of the of the city's international positioning, especially the global TNCs present in the region6. It coincides with a definitive political action to increase the influence of Madrid as global actor, in many cases under the leadership of the City Council of Madrid. This favourable trajectory of the city generates strong expectations at local level, indicating the determined will of the city's government to make Madrid "the most important metropolis in Europe after Paris and London" (OECD, 2007). This paper has looked first for evidence of that ABS contribution in those international published works, in which the networks of global companies’ offices are interpreted as an indicator of the world city process. The condition of Madrid, although in a second level, stands out as one of the major global centres of services with net gains of connectivity through these office networks, well over neighbour cities. Beyond this position in the world urban hierarchy, it is confirmed the role of Madrid as a connecting node between European cities and main capitals of Latin America, manly due to the financial services. From these evidences a profile has been built for ABS foreign companies located in the city of Madrid. The comparison carried out between SABI's data and the top-100 global business service companies elaborated by GaWC (despite the necessary update), confirms that the presence in the city of Madrid through foreign companies is the main vector of entrance of global services in the city. In other cases, the TNCs settle in the region through the participation in national companies that also are included in SABI source. However, two major doubts have appeared about the representativeness of the used source (and perhaps also of the GaWC approach). First, there is no case in the SABI’s listing of dependent international offices belonging to a company located abroad. Secondly, the proliferation of interconnecting forms that do not imply physical presence through offices. Both facts represent a problem, given the explained complexity of the why, how, and where of the internationalization and also the different ways in which spatial economies are created as firms intermediate in geographical marketplaces (Faulconbridge et al, 2008). The conclusion in summary is the necessity to add alternative information sources for the study of the question. In an effort to close the described “virtuous cycle”, this work has also focussed in the location advantages that the city of Madrid offers for the ABS. For this, the paper describes a new model to verify the hypothesis of the greater dynamism of companies located in world cities with greater international connectivity, presenting methodological differences with respect to the analysis raised by Glückler (2007), one of the most interesting contributions in this field. Namely, the model used (CHAID answer tree, against multiple linear regression analysis); the measurement of firm performance selected as dependent variable (relative index of efficiency, against annual growth rate of employment); or the explanatory variables (indirect approach of international connectivity through capital ownership or export propensity, against direct variables like operations volume or international clients). As far as the results, considering that both cases are models that can only explain a limited portion of the variance, we considered that CHAID offers at least two advantages; a greater flexibility opposite to theoretical restrictions of the traditional models (i.e neither non-uniform nor constant effects throughout the independent variable), and a hierarchic character of the reached solution. Thanks to this, the model have identified substantial differences of efficiency in favour of foreign companies, which are supposed to be internationally more connected, and therefore, more benefited from economies of overview, including trans-local network externalities (business opportunities, global networks of clients, flows of knowledge, etc.). The same positive effect is also observed in the case of national export companies. At the same time, although the effect of metropolitan location on the company's performance is in general weak, the results suggest positive differences in favour of national companies located in the city of Madrid, and dedicated to more traditional business services oriented towards the local market. Therefore, once the effects associated with the international connectivity are discarded, the local externalities are revealed especially important for this group, as stressed in the previously described theoretical debate. On the other hand, as it was hypothesized by Glückler (2007), in the case of monocentric urban structures, like those in Madrid, the gap between the central city and the rest of the metropolitan region is quite important. Finally, it is necessary to point out the need for further comparative research with other Spanish and European competitor cities to confirm some of the tendencies suggested by the analysis of the SABI data. Also, as previously mentioned, forthcoming studies should incorporate a qualitative approach, based upon surveys and interviews to companies in the city of Madrid (already in progress by our research team), in order to answer some important questions, for instance the integration forms of these global companies in the local economy, the relations with other TNCs as well as SMEs, or the location of their main clients. In short, it is crucial to improve our knowledge about the motivations of companies that have contributed to the position and competitiveness of Madrid as the principal location for financial intermediation and business services in Spain. BIBLIOGRAPHYAharoni, Y. (2000) The role of reputation in global professional business services, in: Y. Aharoni and L Nachum (Ed.) Globalization of Services: Some Implications for Theory and Practice, pp. 125-141. London: Rutledge. Amin, A. (2002) Spatialities of globalisation, Environment and Planning A, 34, pp. 385- 399. Ayet, G.C. and Sanz, B. (2004) Las sedes centrales en la economía madrileña. Madrid: Comunidad de Madrid. Bagchi-Sen, S. and Sen, J. (1997) The current state of knowledge in internacional business in producer services, Environment and Planning A, 29, pp. 1153-1174. Baldwin, J. (1992) industrial efficiency and plant turnover in the canadian manufacturing sector, in: Industrial efficiency in Six Nations, pp. 273-309. London: The MIT Press. Bartlett, C.A. and Ghoshal, S. (1989) Managing across Borders: The Transnational Solution. London: Century Business. Beaverstock, J. (2004) ‘Managing across borders’: knowledge management and expatriation in professional legal service firms, Journal of Economic Geography, 4, pp. 1-25. Beaverstock J. V., Simth R. G. and Taylor, P. J (1999) A roster of world cities, Cities, 16 (6), pp. 445-458. Beaverstock, J. V., Simth, R. G. and Taylor, P. J. (2000a) World City Nerwork: A new Metageography?, Annals of the Association of American Geographers, 90 (1), pp. 123-134. Beaverstock J. V., Simth, R. G., Taylor, P. J., Walker, D. R. F., Lorimer, H. (2000b) Globalization and world cities: some measurement methodologies, Applied Geography, 20, pp. 43-63. Boddewyn, J. J., Halbrich, M. B. and Perry, A. C. (1986) Service Multinationals: Conceptualization, Measurement and Theory, Journal of International Business Studies, 17 (3), pp. 41-57. Breiman, L., Friedman, J., Olshen, R. and Stone, C. (1984) Classification and Regression Tress. Belmont, California: Wadsworth. Brenner, N. (1998) Global cities, local states: global territorial City formation and state restructuring in contemporary Europe, Review of International Political Economy, 5 (1), pp. 1-37. Bryson, J. R., Daniels, P. W. and Warf, B. (2004) Service Worlds: People, Organizations, Technologies. London: Routledge. Castells, M. (1989) The Informational City. London: Blackwell. Córdoba Ordóñez, J. and Gago C. (2002) Madrid en el escenario de un sistema mundial de ciudades, Anales de Geografía de la Universidad Complutense, Vol. Extraordinario 2002-1, pp. 203-209. Charnes, A., Cooper, W. Y. and Rhodes, E. (1978) Measuring the Efficiency of Decision Making Units, European Journal of Operational Research, 2, pp. 429-444. Daniels, P. W. and Bryson, J. R. (2002) Manufacturing services and servicing manufacturing: Knowledge-based cities and changing forms of production, Urban Studies, 39 (5-6), pp. 977-991. Dicken, P. (2003) ‘Placing’ firms: grounding the debate on the ‘global’ corporation, in: J. Peck and H.W.C. Yeung (Eds.) Remaking the Global Economy: Economic-Geographical Perspectives, pp. 27-44. London: Sage. Dunning, J. H. (1979) Explaining changing patterns of international production: in defence of the eclectic theory, Oxford Bulletin of Economics and Statistic, 41 (4), pp. 269-295. Dunning, J. H. (1985) Multinational Enterprises, Economic Structure and International. Competitiveness. Chichester: John Willey & Sons. Dunning, J. H. and Norman, G. (1983) The theory of the multinational enterprise: an application of multinational office location, Environment and Planning A, 15, pp. 675-692. Farrel, M. J. (1957) The Measurement of Productive Efficiency, Journal of the Royal Statistical Society. Series A (General), 120 (3), pp. 253-290. Faulconbridge, J. R., Hall S. J. E. and Beaverstock, J. V. (2008) New insights into the internationalization of producer services: organizational strategies and spatial economies for global headhunting firms, Environment and Planning A, 40, pp. 210-234. Fernandez, M.T. (2000) Presencia y efectos de arrastre de las filiales extranjeras de servicios a empresas en España, Documento de Trabajo 1/2000. Madrid: SERVILAB-Universidad de Alcalá. García Delgado, J. L. (Ed.) (2007) Estructura económica de Madrid. Madrid: Civitas. Glückler, J. and Armbrüster, T. (2003) Bridging uncertainty in management consulting: the mechanisms of trust and networked reputation, Organization Studies, 24, pp. 269-297. Glückler, J. (2005) Making embeddedness work: social practice institutions in foreign consulting markets, Environment and Planning A, 37, pp. 1727-1750. Glückler, J. (2007) Geography of Reputation: The City as the Locus of Business Opportunity, Regional Studies, 41 (7), pp. 949-961. Gordon, I. (2003) Capital needs, Capital Growth and Global City Rhetoric in Mayor Livingstone´s London Plan, paper presented to the 99th Annual Meeting of the Association of American Geographers, 7 March, New Orleans Gritsai, O. (2004) Global Business Services in Moscow: Patterns of Involvement, Urban Studies, 41 (10), pp. 2001-2024. Heshmati, A. (2003) Productivity Growth, Efficiency and Outsourcing in Manufacturing and Service Industries, Journal of Economic Surveys, 17 (1), pp. 79-112. INE (2003) Los grupos de empresas del DIRCE; Análisis de la globalización bajo la óptica de los registros de empresas. Resultados Estadísticos 2002. Madrid: Instituto Nacional de Estadística. Johannisson, B. (1990) Organizing for local economic development: on firm and context dynamics, paper presented to the 30th European Conference RAS, 28-31 August, Istanbul Jones, A. (2005) Truly global corporations? Theorising `organizational' globalization in advanced business services', Journal of Economic Geography, 5, pp. 177-200. Jones, A. (2007) More than ‘managing across borders?’ the complex role of face-to-face interaction in globalizing law firms, Journal of Economic Geography, 7, pp. 223–246. Kass, G. V. (1980) An exploratory technique for investigating large quantities of categorical data, Applied Statistics (Royal Statistical Society), 29 (2), pp. 119–127. Knox, P. and Taylor, P. J. (1995) World cities in a world system. Cambridge: Cambridge University Press. Lundvall, B. A. and Johnson, B. (1994) The learning economy, Journal of Industry Studies, 1 (2), pp. 23-42 Wilkinson, L. (1992) Tree Structured Data Analysis: AID, CHAID and CART. Chicago: SPSS Inc., Northwestern University. Martinez, S. R. and Rubiera, F. (2006) Outsourcing of advanced business services in the Spanish economy: Explanation and estimation of the regional effects, Service Industries Journal, 26 (3), pp. 267-285. Méndez, R. (2001) Transformaciones económicas y reorganización territorial en la región metropolitana de Madrid, EURE (Santiago), 27 (80), pp. 141-161. Merino de Lucas, F. and Salas Fumás, V. (1996) Diferencias de eficiencia entre empresas nacionales y extranjeras en el sector manufacturero, Papeles de Economía Española, 66, pp. 91-208. Molina, M. and Martín-Roda, E. (1998) La empresa multinacional en la Comunidad de Madrid. Serie Estudios Regionales BBVA. Madrid: BBVA. Molina, M. (2002) Madrid, metrópolis global, Anales de Geografía de la Universidad Complutense, Vol. Extraordinario 2002- 1, pp. 349-356. Morgan, G., Study, A. and Quack, S. (2006) The globalización of Management Consultancy Firms: Constraints and limitations, CSGR Working Paper No 168/05. Coventry: University of Warwick. Moulaert, F. and Djellal, F. (1995) Information Technology Consultancy Firms: Economies of Agglomeration from a Wide-area Perspective, Urban Studies, 32 (1), pp. 105-122. Nachum, L. (1999) The Origin of the International Competitiveness of Firms: The Impact of Location and Ownership in Professional Service Industries. Cheltenham, Glos: Edward Elgar. Nachum, L. (2000) Economic geography and the location of TNCs: Financial and professional service FDI to the US, Journal of International Business Studies, 31 (3), pp. 367-385 OCDE (2007): OECD Territorial Reviews: Madrid, Spain. Paris: OECD. Rodriguez-Pose, A. and Zademach, H. M. (2003) Rising Metropolis: The Geography of Mergers and Acquisitions in Germany, Urban Studies, 40 (10), pp. 1895–1923. Rubalcaba Bermejo, L. (2006) Ferias y congresos en una economía de servicios avanzados, Economistas, 24 (108), pp. 350-354. Sánchez Moral, S. (2008) Industrial clusters and new firm creation in the manufacturing sector of Madrid’s metropolitan region, Regional Studies (in press) Sassen, S. (1991) The global city. Princeton: NJ Princeton University Press. Sassen, S. (2003) Localizando ciudades en circuitos globales, EURE (Santiago), 29 (88), pp. 5-27. Scott, A. J. (1996) Regional motors of the global economy, Futures (Cambridge), 28 (5), pp. 391-411. Taylor, P.J. and Derudder, B. (2004) Porous Europe: European cities in global urban arenas, Tijdschrift voor Economische en Sociales Geografie, 95 (5), pp. 527-538. Taylor, P. J., Walker, D. R. F. and Beaverstock J V (2002a) Firms and their Global Service Networks, in: S. Sassen (Ed.) Global Networks, Linked Cities, pp. 93-115. London: Routledge. Taylor, P. J., Catalano, G. and Walker, D. R. F. (2002b) Measurement of the Wolrd City Network, Urban Studies, 39 (13), pp. 2367-2376. Taylor, P. J., Catalano, G. and Gane, N. (2003) A geography of global change: cities and services, 2000-2001, Urban Geography, 24 (5), pp. 431-441. Taylor, P. J. and Walker, D. R. F. (2001) World cities: A First Multivariate Analysis of their Service Complexes, Urban Studies, 38 (1), pp. 23-47. Wilkinson, L. (1992) Tree Structured Data Analysis: AID, CHAID and CART, paper presented at the 1992 Sun Valley, ID, Sawtooth/SYSTAT Joint Software Conference. Wood, P. A. (2002) Knowledge-intensive services and urban innovativeness, Urban Studies, 39, pp. 993-1002. Yeung, H.W.C. (2005) Organizational space: a new frontier in international business strategy?, Critical Perspectives on International Business, 1, pp. 219-240.

NOTES* Simón Sánchez Moral, Institute of Economics, Geography and Demography. Spanish Council for Scientific Research (CSIC), Madrid, Email: ssanchez@ieg.csic.es 1. This paper covers an initial stage in the research carried out in the context of the project of the Industrial Observatory of Madrid (City Council of Madrid). 2. SABI contains information of more than 200,000 Spanish companies with a turnover off superior to the 360,000 Euros. For this paper we considered foreign companies those in which more of 50% of the property of the capital it is in foreign hands. 3. From 2004, PricewaterhouseCoopers, Ernst & Young, KPMG and Deloitte. 4. Alpha cities: London, Paris, New York, Tokyo, Chicago, Frankfurt, Hong Kong, Los Angeles, Milan and Singapore. Beta cities: San Francisco, Sydney, Toronto, Zurich, Brussels, Mexico, Sao Paulo, Moscow and Seoul. 5. Although 5,040 companies declare not to have any worker and/or revenues, the efficiency index displays a mark positive asymmetry as a result of the presence of extreme cases. All the observations with a null value of efficiency and those over three standard deviations were eliminated. 6. Another form of contribution to the international positioning of Madrid, outside the reach of this work, relates with the activity abroad of Spanish multinationals in ABS, as well as the banks Santander Central Hispano (BSCH) and Bilbao Vizcaya Argentaría (BBVA), which already in 2003 headed the ranking for major banks in Latin America by consolidated assets (OECD, 2007). Also receives an increasing attention the trade fair activity of Madrid, with 71 events in 2005 and almost 11% of visitors of the total in European centers (Rubalcaba Bermejo, 2006).

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||