GaWC Research Bulletin 124 |

|

|

|

A revised version of this Research Bulletin has been published in Environment and Planning A, 39 (6), (2007), 1325-1345, under the title 'The Role of Location in Knowledge Creation and Diffusion: Evidence of Centripetal and Centrifugal Forces in the City of London Financial Services Agglomeration'. doi:10.1068/a37380 Please refer to the published version when quoting the paper.

1 INTRODUCTIONClusters have been defined in many ways reflecting multidisciplinary interest and their varied form ranging from the weak which do not confer significant advantages to incumbent companies to the strong which enable high and sustained productivity (Markusen, 1996; Gordon and McCann, 2000; McCann et al., 2002). A general definition that captures the essence of the strong sustainable cluster is provided by the UK Department of Trade and Industry (White Paper, 1998):

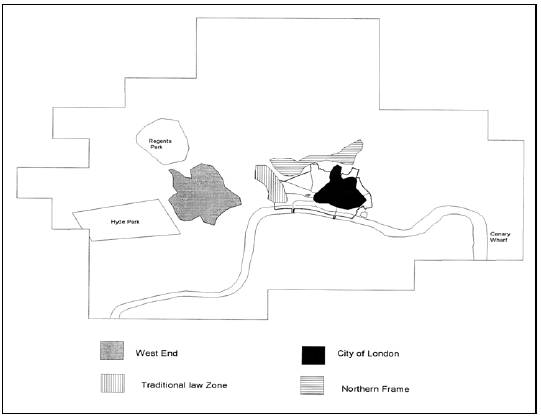

What are the strengths of this definition? Firstly, it does not relate to a single industry; rather it merely requires that companies in a cluster are interdependent in some way. This makes sense. For example, we know from the early work on the Silicon Valley cluster that it includes not only microelectronics firms but also venture capitalists (Saxenian, 1994). Secondly, a cluster is defined not just in terms of companies but also supporting institutions. These institutions can play an important coordinating role in strong clusters (Best, 1990; Piore and Sabel, 1984). Thirdly, in addition to competition, non-market linkages are emphasized. Cooperation, borne out of a common culture and trust, is known to be particularly important with respect to innovation (Camagni, 1991; Capello, 1999). Finally, the definition encourages us to think of clusters as complex systems of industrial organization. It is this very complexity that makes them difficult to copy and therefore sustainable (Maskell and Malmberg, 1999). Recent empirical studies show that companies in strong clusters grow faster than average and that strong clusters attract a disproportionate amount of new entrants (Cook et al. 2001; Cook and Pandit, 2002; Pandit et al. 2001, 2002). Also, that productivity (Henderson, 1986) and innovation (Audretsch and Feldman, 1996; Baptista and Swann, 1998) is higher within strong clusters . In short, clusters can lead to superior economic performance. What is more, cluster benefits are found to accrue in many different types of manufacturing and service industries from aerospace, biotechnology and computing to broadcasting and financial services (Agnes, 2000; Beaudry et al., 1998; Pandit and Cook, 2003; Wrigley et al., 2003). The study reported in this paper contributes to this emerging understanding of the link between clustering and economic performance. It examines the benefits and costs accruing to financial services firms located in London, Europe's largest and most important financial services cluster. The paper is structured as follows. Section 2 details the study's methodology. Next the study's findings are presented and analyzed. A final section concludes and draws key policy implications. 2 METHODOLOGYThe London financial services cluster is depicted in Figure 1. The cluster includes companies and institutions engaged in banking, insurance, securities dealing, fund management, derivatives, maritime services, foreign exchange, bullion markets, legal services, accounting and related services, management consultancy, and other professional and support services (advertising and market research, recruitment, education, financial publishing, software development). There are five distinctive sub-concentrations. First, Canary Wharf to the East which is the home of some of the largest investment banks. Second, the very dense "square mile" that is the City of London ("the City") featuring banks, insurance and law firms. Third, a less dense West End, concentration featuring banks near Mayfair and advertising in Soho. Fourth, an incipient concentration north of the City featuring services such as architecture and business support. Finally, a concentration that lies in-between the City and the West End consisting of law firms located in close proximity to the law courts. Each of these subconcentrations are fundamentally interdependent and make up the general London financial services cluster. Figure 1: The London Financial Services Cluster

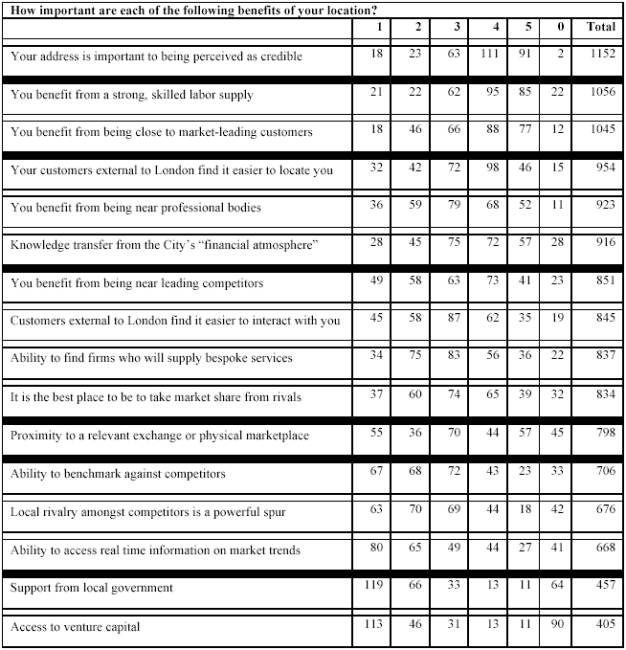

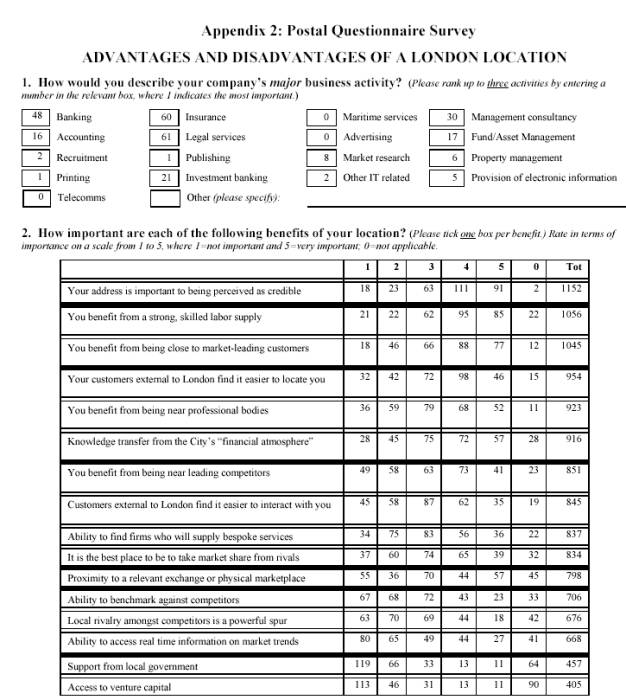

Data on financial services clustering in London were collected via a postal questionnaire survey and via an in-depth face-to-face interview survey. Both survey designs were informed by relevant theory (see Appendix 1 for an overview). For the questionnaire survey, 1,500 questionnaires were posted. The sample was selected using a stratified method. 100% of the largest 350 firms were selected. These were identified primarily from a database supplied by the specialist information provider Market Locations. The remaining 1,150 firms were drawn at random from the rest of the Market Locations database (using a random number generator). The original mailing went out in April 2002 with a follow-up in June 2002. A third mailing was considered but rejected in view of the good response rate to the first two mailings. A total of 310 usable questionnaires were returned, a response rate of just over 20%. The postal questionnaire data are presented in Appendix 2. In almost all cases, respondents were asked to rank the importance of a factor from 1 (not important) to 5 (very important) with an option of 0 if not applicable1. Factors are presented in total score rank order which is simply the sum of recorded scores for a given factor. For example, a factor which received 2 ranks of 1 (not important), 2 of 2 and 2 of 5 (very important) would receive a total score of 2x1+2x2+2x5=16. This method could produce anomalous results (e.g., a factor which receives some 1s and many 5s being ranked above one which has a lot of 4s, no 1s but relatively few fives), but, after close inspection, does not appear to. A useful benchmark for interpreting these total scores is the average (mean) of the total score across all questions (where it was possible to compute a total score) which is 855. This may be thought of as the score you would typically expect a factor to receive. The 95% confidence interval around this average is 808-901. Accordingly, a useful rule of thumb in comparing the relative importance of each factor is that any total score below 808 is relatively unimportant and any total score above 901 is relatively important. The heavy black lines divide factors into groups where there is no statistically significant differences in the total score within groups but there is a statistically significant difference between groups (based on the "conservative" sign test - see Appendix 2). This indicates that factors within two heavy black lines were regarded as being of roughly equal importance by respondents, but either side of a black line there is a difference in the degree of importance attached to a factor. Tests were conducted for the possible existence of statistically significant differences in the scores among different lines of activity (using contingency tables) and for significant differences among firms of different size (using the Kruskal-Wallis analysis of variance). Such differences are commented on by exception where they are particularly strong and interesting. Two sets of analyses for differences by line of activity were performed. The first looked at the three most frequently occurring lines of activity in the sample: banking, legal services and insurance2. These three comprise half the sample and for technical reasons explained in Appendix 2 allowed the most fine-grained analysis to be performed. Other sectors had too few responses to analyze without re-working of the data which would have entailed aggregation and the associated cost of loss of detail about the degree of importance attached to each factor. Firm size is based on the number of employees at the establishment to which the questionnaire was sent. Some firms with very few employees were subsidiaries of substantial firms, the leading example being the London offices of central banks from around the globe. However, perusal of the sample reveals that the majority of firms categorized as small were genuinely small firms and not the small plants of large firms. The interview survey was designed to provide qualitative evidence complementing quantitative data gathered by the postal questionnaire. Whereas the postal survey provides hard, measurable evidence on discrete questions from a large sample of firms of different sizes, the indepth face-to-face meetings elicit "softer" evidence on the processes underlying the data drawing on the experience of senior practitioners in leading London financial services organizations. In order to explore complex functional relationships associated with spatial clustering freely, a semi-structured interview methodology was adopted. The interview schedule (Appendix 3) was used to guide discussion towards the key research themes and a series of prompts and probes were introduced by the interviewer to refine lines of questioning as new insights and understandings emerged. This methodology provided the flexibility to utilize knowledge gained progressively during each interview to inform the dialogue building a rich data base overall on particular circumstances and variables. Importantly, the approach allowed the identification and exploration of issues prioritized by respondents themselves as relevant to the research questions and the development of a sound understanding of causes and effects. The scheduled interview length was 45 minutes but in many cases discussion extended to 60 or 90 minutes. The aim was to interview a selection of senior executives in leading organizations within key sub-sectors. Such organizations, in a series of sub-sectors: banking, auxiliary finance, insurance, legal, accounting/consulting, were identified using 2001/2002 sources, for example The Banker, London Investment Banking Association (LIBA), International Financial Services, London (IFSL) and invited to participate. While most firms were large by international and London standards, prominent small, specialized organizations were included. The sampling stategy was weighted towards banks and auxiliary financial services due to their strong representation, concentration and importance in London. The plan was to conduct 30 interviews - 14 banking, 6 auxiliary financial services, 3 insurance, 3 legal and 4 accounting/consulting, selecting up to 20 firms in the City and up to 10 from elsewhere in the cluster. For practical reasons, interviews were arranged on a first come first served basis regardless of location so, to ensure a reasonable representation geographically, more than 30 interviews was actually conducted. In total, 39 interviews were conducted across seven sectors. The interview results were coded numerically and sorted by both sector and location variables and offer an understanding of the processes that constitute the clustering phenomenon as seen through the eyes of some of the most senior decision-makers in the London cluster. 3 QUESTIONNAIRE AND INTERVIEW SURVEY FINDINGSThis section reports the key findings of the questionnaire and interview surveys. It begins with an overview of the benefits of clustering and then proceeds to investigate four major themes (the labor market, the importance of personal relationships, sources of help with innovation and interdependencies) in more detail. Attention then shifts to the disadvantages of a London location and the nature and extent of declustering. 3.1 An Overview of General BenefitsThere are several important benefits of a London location. The findings are summarized in Table 1 in total score rank order. The importance of a credible address stands apart at the head of these advantages and indeed has the fifth highest total rank of all factors in the questionnaire. It is also among the most consistently mentioned themes in the interview survey. Location can perform a valuable economic role by transmitting a credible signal of a firm's history and quality to its customers. Economic theory suggests that firms that provide the highest quality will have the greatest incentive to acquire the most favorable locations. Accordingly, the occupancy of the most prestigious address is a signal conveying valuable information in the market. Reputation effects are themselves a source of cluster advantages as opinion, good or bad, influencing the reputation of an individual or firm, will flow more easily in a more compact geographical space. The interview survey highlighted the notion of a credible address as a well regarded brand. For example, a City location turns a law firm into a "City law firm". Similarly, insurance companies gain prestige when in close proximity to Lloyds of London. Table 1: General Benefits of a London Location

There are some important differences among firms regarding the importance attached to this advantage. Firms in legal services and management consultancy place significantly more importance on having a credible address. These businesses provide classic "credence services" where it is not only difficult to evaluate the quality of the service provided in advance, but also, to some extent even after the service has been provided. For such services, customers rely heavily on either a long standing relationship or on a projected image (partly created by the right address). This excerpt from an interview with a law firm summarizes very clearly the importance of a "City" address and associated branding:

The second highest rated benefit of a London location is the ability to tap into a strong, skilled labor supply. Section 3.2 discusses labor market benefits in detail. Proximity to customers and being easily located by customers figure highly among the benefits of a London location. Being close to customers and being easily found by external customers tended to be of greater importance to legal firms, but the difference was not statistically significant. Insurance companies place significantly greater emphasis on being near market leading customers and being close to a physical exchange or market place as did property/real estate firms. These comments are representative of firms in the insurance and property/real estate sectors:

Banks place significantly higher importance on knowledge transfer and on being near a strong skilled labor supply. They also rank support from local government more highly than insurance or legal firms. At interview, such factors were mediated through the interdependencies of the market/client interface and inter-firm relationship, couched in both formal and informal networks and social interactions. As one major investment bank suggested, they were in London because of the "sheer intellectual infrastructure" and "the professional suppliers available". But, the bottom line was, if a bank wanted to cut it as a "global bank" they had to be in London. Here are two typical comments from banks:

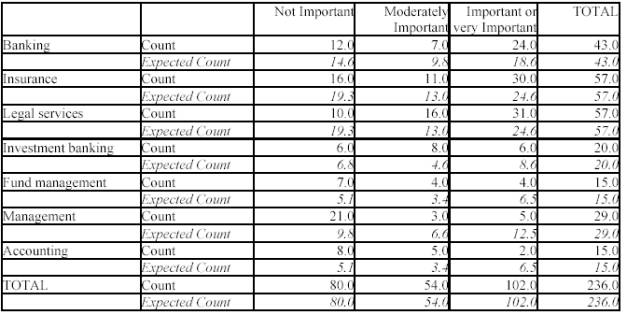

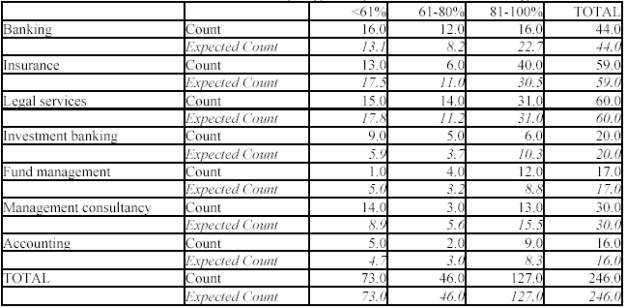

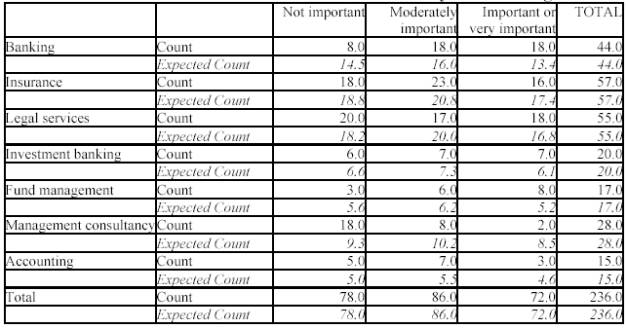

Banks and legal firms were significantly more likely to rate proximity to professional bodies as being an important advantage of their location and management consultancies were significantly more likely to rate it as being unimportant. At interview, banks referred to bodies like the Bank of England or Financial Services Authority, and legal firms the Law Society, and infrastructure of the court system. There is a marked difference between firms in the importance attached to being near leading competitors as a general advantage of locating in London. Banks, insurance and legal firms were much more likely to rate this factor as being important than firms in other lines of activity and management consultancies significantly less so. The results are shown in Table 2. In this table the crucial comparison is between the count, which is the number of firms that gave a response in each category, and the expected count which is the pattern which would be observed if the number of firms in each line of activity had their responses spread over the (three in this case) categories of response in the same proportions as for the total responses added over all firms. Therefore any case where there is a big difference between the count and expected count indicates that firms in a particular sector regard a factor as being unusually important or unimportant. The table shows, for example, that we would expect only 9.8 of the 29 management consultancies to rate proximity to competitors as not important but in fact we see that 21 of them did, which is a very marked difference. Table 2: The Importance of Being Near Leading Competitors

Banks, investment banks and fund management firms were significantly more likely to rate the ability to gain real time information about market trends as an important advantage of a London location than other firms, and accountancy firms and management consultancies are significantly more likely to rate it as unimportant. At interview, these findings from the questionnaire survey were substantiated in more detail. Banks in particular, acknowledged that proximity to the market and organizations which provided real-time data was crucial for their survival in the market, which was mediated in many instances through personal interaction and social relations. The spur of local rivalry was significantly more likely to be viewed as an important benefit by banks and legal firms and significantly more likely to be viewed as unimportant by accounting firms and management consultancies. The ability to benchmark against competitors was of far greater importance to firms in legal services than other lines of activity, whereas not a single management consultancy and only one accounting firm saw this as being either an important or very important advantage. As regards size effects, larger firms place significantly more emphasis on the importance of being near to market leading competitors, the ability to benchmark, being near a strong, skilled labor force and the spur of competition. One feature which was brought out in a number of the interviews was the importance of the wider attraction of London as a major metropolis. As one firm put it, "its history, its appearance, its buildings, its culture, its arts". Interviewees emphasized the need to maintain London's image, as the place people want to live and work with regard to contemporary lifestyle, fashion, choice, and taxation. London's openness, cultural diversity, cosmopolitanism and "buzz" were seen as governing the marginal decision for global companies about where to locate new business. One banker stressed that, "Importantly, as a financial center, London is an open society that is accepting to overseas people and to business".

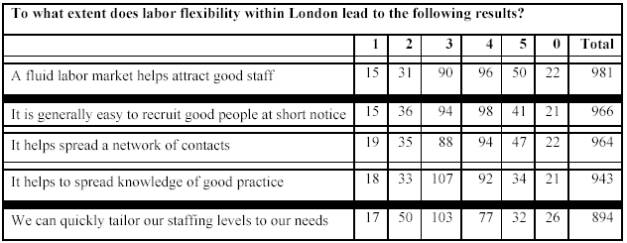

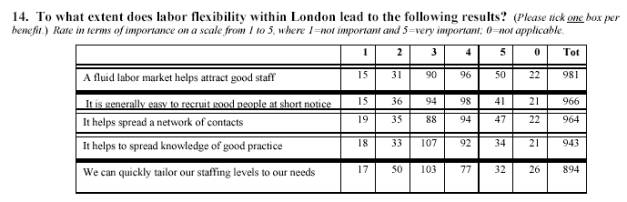

3.2 The Labor MarketThe labor pool from which the London financial services cluster can draw is clearly one of its greatest assets. The questionnaire and interview surveys indicated the extent to which London displays classic cluster advantages in the labor market (see Table 3). Table 3: Labor Market Benefits

The pulling power of London's fluid labor market is one of the most important engines of cluster dynamism. While a small number of respondents did comment on the negative effects of mobility, such as the bidding up salaries and losing key staff to competitors, the advantages of mobility seem to greatly outweigh the disadvantages. There is a general tendency for banks to rate these labor market advantages more highly than insurers or legal firms. The strength of the London labor market was consistently stressed in the interview survey. Many respondents in all sectors remarked that the depth of expertise across the range of the professions is vastly superior to anywhere else in Europe. Several pointed out that the size of the labor force in financial services in London far exceeded the entire population of Frankfurt. Here is a typical response:

The existence of a large labor market in a cluster gives rise to two key advantages. Firstly, labor is attracted into the market, because the size of the market provides a better chance of continuity of employment. Secondly, the sheer size of the market provides an incentive for people to invest in highly specific skills. As Adam Smith so penetratingly observed over 200 years ago, the division of labor is limited by the extent of the market. Size coupled with the status and prestige of London and the fact that the most interesting and most well-rewarded work is to be found there acts as a magnet for talent. London offers a wide array of career opportunities both within large firms and through the ability to move easily between employers. Several firms spoke of the problems of attracting top talent if they were in the regions. This is part of a classic self-sustaining process in clusters. The advantages of the cluster, including the size of the labor pool and other spillovers between firms, mean that the cluster is unusually productive and so more resources flow to the cluster and these re-enforce its advantages. What also emerges as being important about this process in London is that it acts as a magnet not only for national but also international talent. This and the rich ethnic mix which exists in London anyway means that there is access not only to a pool of talent, but one which collectively speaks a vast range of languages. One respondent of a major global non- UK firm rated London's labor market as having the greatest ethnic diversity of any of the locations in which they operated, at least as far as the relevant labor market went. The prestige of the capital, the quality of the experience that can be gained there, the ability to perfect their English and its reputation as a cultural center are all features of the mix which makes London so attractive. An interesting point made by two respondents was that many non-UK employees are keen to work and live in London so that their children will attend English speaking schools and develop strong bilingual skills. Culture alone is not enough, however, and one respondent commented on how low the flow of international talent to Paris is when compared to London. The London labor market was seen to have a number of other important features in the interview survey. The flexibility of the market was regarded as being an advantage compared to other European countries. As one non-UK banking respondent put it, "We're not afraid to put people here". In the face of the natural cyclicality of financial services, the flexibility to contract and expand when necessary is placed at a premium. A banker commented:

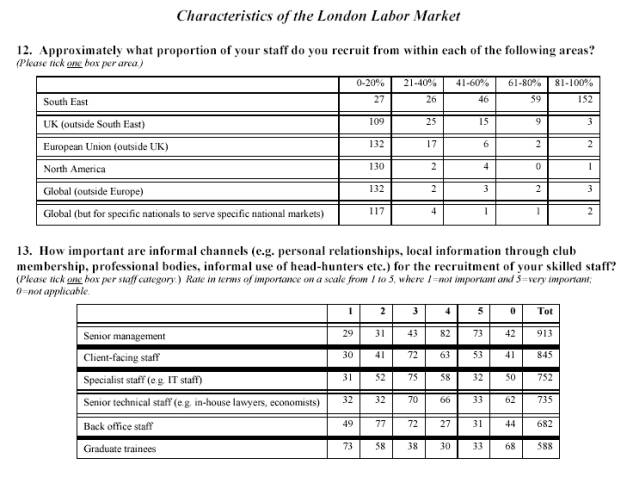

Another feature is the ability of staff to gain experience in London and this acts as a means of transferring best practice internationally. An analysis of the geographical reach of London's labor market in recruitment terms indicated two main trends. Firstly, most labor is recruited from within the South East of England. Secondly, the ability to draw in labor from around the world, not necessarily in great numbers, is important and very important to a small number of firms. For some grades of staff, the recruitment is overwhelmingly of people already in London but the more senior and more specialized labor becomes, the further a-field the relevant labor market extends and for some types of labor the London labor market has global reach. In Table 4, banks and investment banks emerge as recruiting a significantly smaller proportion of their staff from the South East and insurance firms significantly more, one investment banker commented:

Table 4: Recruitment of Staff (all grades) from South East England

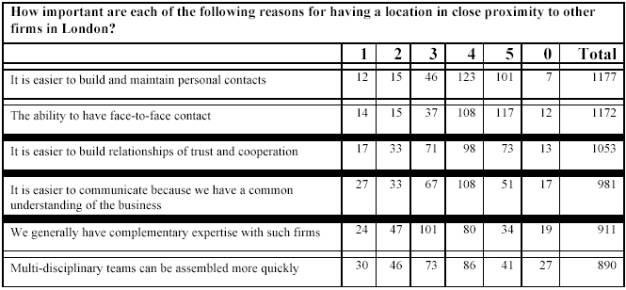

Responses on commuting patterns in the interview survey revealed that in many cases staff tend to come from specific areas in and around London and that ease of access for skilled client facing, secretarial and back office staff to an existing central London office would be a key factor ruling out a significant change of location. The concentration of transport nodes around the City was seen as a major advantage in terms of staff recruitment. In banks and legal firms, high earning skilled staff were said to favor living in the more expensive outer boroughs of London, for example, Richmond-upon-Thames and Wimbledon, or the West End, for example Kensington, or the rural commuter belt. Some senior staff preferred to commute weekly to London and retained central London flats convenient for the office. There was also evidence of some inter-city weekly commuting to London from other UK and European cities by senior staff. Skilled support staff tend to live further from the center of London, either in the suburbs or outside London where housing prices are lower. Distance from central London was related to age, household circumstances, and cost. Younger skilled staff were said to favor living in fashionable and convenient central London districts while older staff of all grades with children were said to move further out from the center in spite of added commuting time and cost. The location of favored schools emerged as an important housing location factor in some interviews. The ability to recruit senior staff via informal channels was signaled as an important advantage of operating in a compact geographical space. Not surprisingly, informal channels are least important for graduate recruitment which tends to be more routinized and where the candidates concerned will have less of a reputation that might be broadcast over informal channels. The informal recruitment of senior staff is particularly important in investment banking and fund management. It is noticeably less likely to be regarded as important by legal firms. Firms in legal services rate informal recruitment of graduates significantly more highly than do banks and insurers. Informal recruitment is also reasonably important for client-facing staff. Insurance companies are significantly more likely to rate informal recruitment of clientfacing and back office staff as important. Finally, the presence of a pool of talented labor with relevant skills was regarded as a highly important factor which contributed to the ability of firms to innovate. There is virtually no difference in the importance attributed to this factor by firms in different lines of activity. Evidence from the interviews suggests that labor market churn/turnover (estimated to be 25% annually) was an important mechanism for all sectors to bring innovation into the firm, whether that be the specificities of particular labor market processes or tacit and formal knowledge brought about via new cultural working practices or management structures. 3.3 The Importance of Personal RelationshipsThe defining characteristic of a cluster is the close proximity of related firms. We asked how this was advantageous (Table 5). Table 5: The Importance of Close Proximity to Other Firms

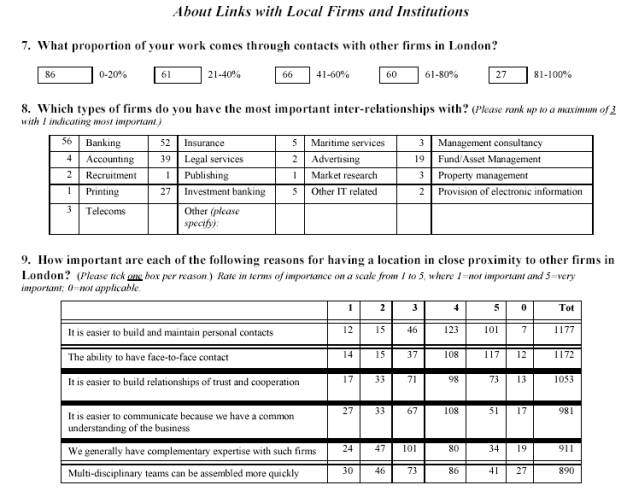

The supreme importance of maintaining personal contact and being able to interact face-toface is clear. In the questionnaire survey as a whole, the importance of maintaining personal contact and being able to interface face-to-face were the second and third most highly ranked factors. The compactness of the City also aids the ability to establish relationships of trust. There are no significant differences between lines of activity regarding the importance of trust. The existence of common understanding and complementary expertise are classic characteristics of dynamic clusters and are much in evidence here. Larger firms are significantly more likely to rate trust and ease of communication as being important and have a distinct, though not quite significant, tendency to rate personal and face-to-face contact as being highly important. The importance of face-to-face contact was underscored by the interview survey, which cast light on why it is important. Several firms emphasized the importance of a face-to-face meeting for conducting complex transactions where it is important to fashion agreement while reducing the chances of misunderstandings or creating antagonism. A face-to-face meeting has the advantage that more information is conveyed, including important non-verbal signals which are important, for example in trying to judge whether someone is honest and trustworthy or in gauging whether someone is unhappy or becoming upset. At the stage where deals are being transacted, a crisis can emerge at any time and there may be a need for a meeting to sort the matter out quickly and satisfactorily. In comparison, e-mail is a poor substitute. One firm suggested that this requirement meant that it was important for senior staff to be based in London. Similarly, several firms cited the need to be close to regulators, including the Bank of England, in order to have the ability to meet face-to-face to resolve important issues and to cement an ongoing relationship. The overall impression gained in the interviews is that there is a deep rooted need to conduct certain business face-to-face. One firm stated explicitly that simply the knowledge that it would be possible to call a snap meeting is important, even if such a meeting is eventually unnecessary. The importance of being able to meet people before doing business with them, to establish relationships and trust, to provide a customized service and conduct negotiations was also widely emphasized. Proximity is an advantage in terms of the ability to have face-to-face meetings because it allows meetings to be called at short notice and it is possible to have a greater frequency of meeting because time and money costs are less than if some people have to travel long distances. Being able to meet more frequently helps build a team. A number of firms in banking and legal services commented on the need to have adequate space for large meetings because the size of meetings had grown as transactions had become larger and more complex, leading to larger numbers of professionals being involved in negotiations. Several firms emphasized that while there has been a burgeoning use of e-mail and video conferencing for intra and inter-firm communication, neither of these media would ever replace the need for physical face-to-face meetings. One respondent reported on the vastly increased use of video-conferencing and e-mail within his own firm, but also on the simultaneous immense pressure on the firm's meeting room space. Several respondents commented that e-mail and video-conferencing work much better with people you know, so face-to-face meeting will continue to be important in forming relationships that can subsequently rely on more remote media of communication. As one respondent remarked:

It is important for firms to be able to meet, especially with their top-level clients who require, and are prepared to pay for, a premium service. This may include receiving visits from back office as well as client-facing staff. One insurance firm emphasized their clients' need to meet the person who will be dealing with their claim in the event of mishap. Several interviewees emphasized the importance of trust:

The compactness of the City also means that it is possible to have a greater density of interaction. This has a number of benefits. Important among them is the ability to build a relationship and allied to it the ability to build a reputation.

The compactness of the City is an advantage in terms of serving overseas customers, since it affords them the chance to come to London and have meetings with all their advisers and perhaps also meet a range of different banks, for example. Talking about international clients, one firm stated:

An important benefit of the density of information which physical propinquity allows is that knowledge flows more easily. One respondent bemoaned the demise of the "City lunch" which was seen as a powerful way of ensuring people knew what the key developments in the market were. Another respondent explained:

Another benefit of dense interaction is that people become socialized in the sense that they absorb norms of doing business as well as the language in which business is done. There is a significant tendency for accounting, and to a lesser extent legal firms, to rate their complementary expertise as being important. Somewhat surprisingly, no fund management firm rated this factor as being important or very important. There are also significant differences in the frequency with which firms rate ease of communications due to a common understanding of the business as being important, with banks and to a lesser extent insurance and legal firms rating this factor as being important more frequently and investment banks and fund management firms rating it as being less important. There is some tendency for the ability to build and maintain personal contacts to be rated as very important more frequently by banks and legal firms. The ability to have face-to-face contact tends to be rated as very important most frequently by insurance firms as indicated by the following remarks:

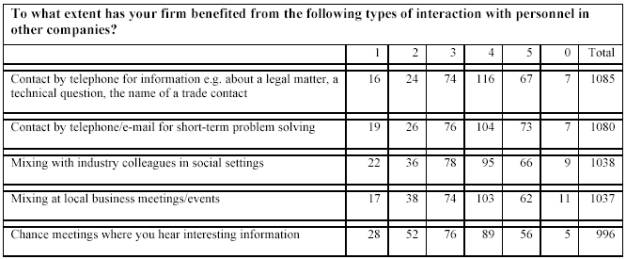

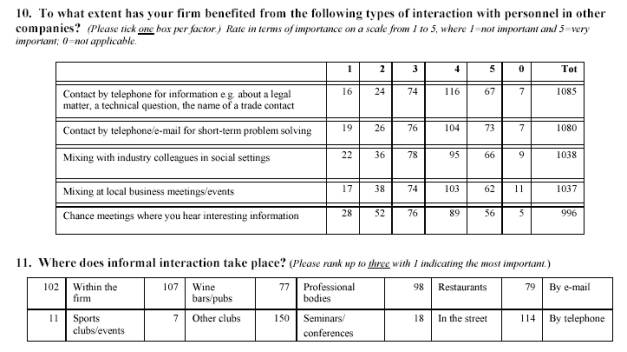

The importance of personal relationships is reflected in Table 6 which contains the most highly ranked group of factors. It might appear at first blush that the fact that telephone and email are the most highly scored ways of having important interaction with staff in other companies belies the need for physical proximity. However, taking these responses together with those in Table 5 casts doubt on this conclusion, since important interaction is likely to hinge on common understanding, trust and complementarity of expertise. Moreover, one is likely to interact more frequently with those with whom one has a more intense personal relationship. Meeting socially, whether by chance or design, is palpably of great importance. Mixing at business events and telephone contact for information is significantly more likely to be rated as important by banks and larger firms. Contact for short-term problem solving tends to be emphasized by management consultancies who have a disproportionate tendency to rate this as very important, however the difference is not significant. Banks and investment banks also have a tendency to rate contact for problem solving as important more frequently than other types of activity. The interview survey revealed that while chance meetings were not emphasized as a key driver of location decisions, they were an important benefit of proximity. The kind of things discussed in chance meetings tend to be industry gossip about what particular firms or people were doing, what key developments are taking place and sometimes bouncing ideas for new products or services. Table 6: Methods of Interaction between Firms

Results from the interview survey entirely corroborate the questionnaire survey regarding the importance of social relationships in sustaining the cluster and the significance of specific meeting places where interaction occurs. These interview excerpts demonstrate the existence of both "old" and "new" practices of interaction in the cluster and articulate the importance of both tacit and formal knowledge transfer in the cluster via business and social interaction amongst all sub-sectors:

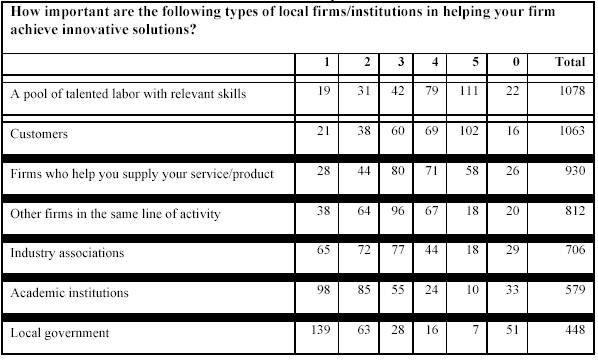

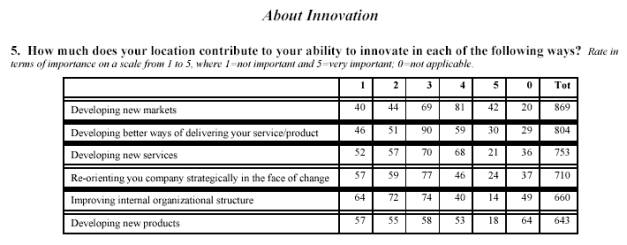

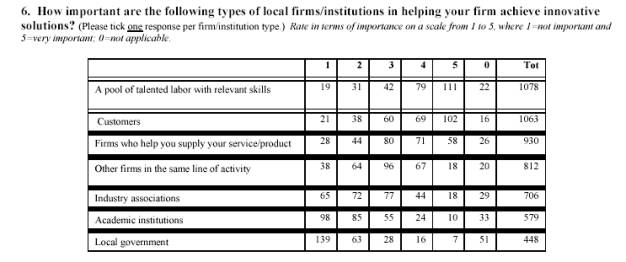

Finally, the interview survey highlighted that being able to physically walk between firms, institutions, professional bodies, bars, gyms etc. was of great significance in sustaining both face-to-face contact especially in the compact geographical area of the City. As one bank emphasized, "physical walking distance is still important in the City", and the over-riding view of the interviewees was that being able to walk to clients, suppliers, markets etc. remained one of the immeasurable locational advantages of the cluster, with anything up to 15 minutes walking time being considered as acceptable for traveling to an appointment with ease. 3.4 Sources of Help with InnovationTable 7 sheds light on the types of local relationships that help innovation in the cluster. A pool of skilled labor and customers are the two most important factors, and both are very highly ranked. Larger firms are significantly more likely to rate the labor pool as being important while legal firms have a tendency to rate help from customers as important, but not significantly so. Banks and insurance firms have a tendency not to rate customer proximity as important so frequently. Local suppliers and firms that provide complementary activities are also important in helping firms innovate. Both banks and insurance firms are more likely to rate the presence of such firms as important than firms in legal services. Firms in the same line of activity also assist to an appreciable degree in innovation, a phenomenon well documented in the case of manufacturing and it is interesting to find evidence of it in the service sector. As revealed in Table 8, banks are significantly more likely to rate the presence of other banks as making an important contribution to innovation. The same tendency is evident for fund management, but not for management consultancies. Larger firms are significantly more likely to rate the presence of other firms in the same line of activity as being important. Banks are also significantly more likely to rate the presence of firms who supply complementary goods and services as being important to innovation. The same tendency is more weakly evident for investment banks. Table 7: Local Relationships and Innovation

Table 8: Presence of other Firms in the Same Line of Activity in Promoting Innovation

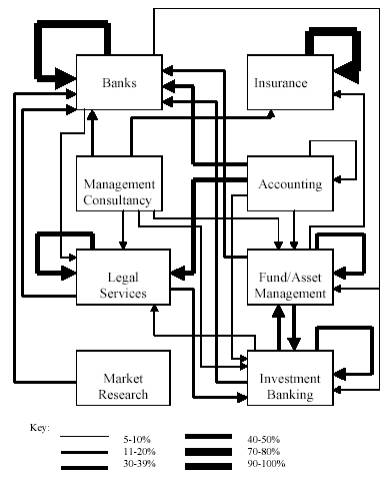

3.5 InterdependenciesFigure 2 gives an impression of sub-sector interdependencies. The figure was constructed by first classifying each firm to a sector on the basis of what it classed as its most important line of activity (question 1 in the questionnaire - see Appendix 2). The next step was to examine which sub-sectors those firms needed to have a relationship with (question 8 in the questionnaire). 74 firms did not provide a ranking, but rather ticked three or more boxes. These were excluded from the analysis which focused only those ranked 1. The arrowheads show the direction of the relationship with the arrowhead entering the sector rated as the most important to have a relationship with. The thickness of the lines indicates the percentage of number 1 rankings for each sector as per the key provided. It is important to bear in mind that the diagram conveys no information about the number of rankings, for example there were only five valid rankings made by market research firms, one of which went to banking (20%). The figure should be viewed in conjunction with Table 9 which gives the absolute number of number 1 rankings. Figure 2: Sub-Sector Interdependencies

Table 9: Very Important to Have a Relationship With

Taking the table and the figure together a number of features stand out. Firstly, banks, including investment banks, appear to be at the hub of the cluster. This is true to a lesser extent of legal services and fund management. Secondly, there is a very high incidence of sub-sectors ranking relationships with firms in their own sector as most important, especially in banking and insurance. Thirdly, some sectors, most starkly accounting, appear to depend more on other sectors than other sectors depend on them. The interview survey revealed further insights into which firms are most valued as neighbors. One general feature of the interview evidence is that being close to customers is the most important factor. The question then arises of who the customer is. For many firms it is a question of derived demand, they get work from other firms in London who are themselves servicing a corporate or private customer. For many firms, access to IT specialists is a crucial issue. Law firms need to be near banks, including investment banks, and insurance companies from which they draw much of their work. Insurance lawyers are heavily concentrated around Lloyds. For law firms there is an added factor that they also need to be close to the courts.

Where international customers are concerned, "closeness" relates to the fact that being in the center of London puts a firm on their beaten track, so while not close comparing HQ to HQ, they are close in the sense that they are regarded as easy to access. Another advantage which works to the benefit of the cluster is that having a range of firms in the same line of activity in close proximity means that there is a strong competitive spur driving firms to innovate, drive up service quality and to keep down costs. As financial services become more standardized and novel products or services are easy for rivals to copy, so firms are competing on service differentiation. There is a need to be close to the client in order to work out bespoke solutions and to provide a high level of personal service. One firm put great importance on being able to get their clients to visit their premises so that they could get a rich experience of the nature of the firm with whom they were dealing. In some businesses it is important to be near clients in order to cut down on the time and money costs of visiting clients. This factor was above all stressed by accounting firms, where staff spend a particularly large proportion of their time with clients. One advantage of being close to other firms in the same line of business is the ability to work out solutions and share risk:

Being close to other types of firm which provide complementary services is important because it enables multi-disciplinary teams to assemble quickly to meet client needs. It is also convenient for clients, particularly those who travel some distance to London, to be able to see a range of their advisers quickly and efficiently. Several respondents pointed to the need to draw together complementary expertise to work out novel and bespoke services for clients. It was judged to be less likely the case that a client would have a pure financing or pure legal requirement. Another benefit of being able to draw in complementary expertise quickly and build and maintain relationships with those who provide complementary expertise is that firms will recommend each other to clients. It is therefore important to be in the loop in London in order to tap into this source of demand: I think it was the case that you had to be in the City because of the need to physically interact. There were certain financial transactions which had to take place because of the time criticality - discount market members and messengers used to carry pieces of paper from one bank to another and they had to be in before 10 o'clock. With electronic banking that doesn't happen but there are other reasons why people still need to be in the City . Proximity and face-to-face contact are essential in the investment banking business. There are those that argue against it because clearly the very successful global investment banks - xx and others - they've all got huge places down at Canary Wharf and they don't feel that necessity [to be in the City]. But we feel comfortable here - we're close to the Bank of England, lawyers and accountants, the regulators who advise us. It's inconceivable to me . that we would do anything other than stay in the City. The above quotation illustrates an important point made by several respondents, that the historical reasons for being in their current location are different from the reasons they continue to stay in their current location. Two respondents put it this way: There's one thing I think we covered by implication is that it's not only where your clients are, it's where your suppliers are. And that's suppliers across a broad range from the professional suppliers like lawyers and consultants and accountants through to all the other suppliers.

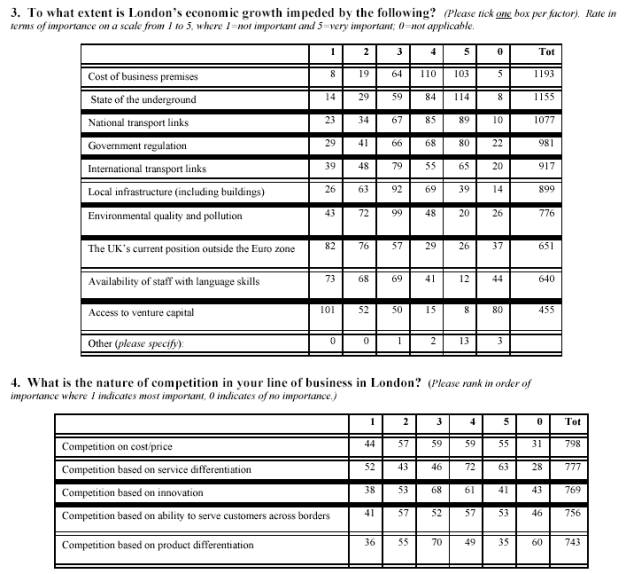

3.6 Disadvantages of a London LocationThe two most pressing problems for firms in the London financial services cluster are the cost of premises and transport difficulties, local, national and international (Table 10). The cost of premises is the single most highly ranked factor across the whole questionnaire. However, this finding needs to be interpreted with care. To an extent, a cluster's success can be measured by increasing rents. The key question is: does this lead to the movement of valuable activity out of the cluster? As discussed in the next section, we found the answer to this question to be "no". If activity does move out, it tends to be less valuable activity. Table 10: Disadvantages of a London Location

The inadequacies of the transport system was born out by the interview survey, with almost every respondent mentioning it and a number wanting to dwell on this single issue. While the cost of office premises was considered a disadvantage, it was not prioritized as a threat to the cluster. Transport however was widely seen as "a massive all-encompassing problem". This respondent's comment illustrates the strength of feeling expressed by many on this subject:

There is a crucial issue regarding the ability to cross London especially for business trips. Some respondents pointed to the example of the investment bank Lazards moving to the West End, where most of its major corporate clients are, to avoid the inconvenience of traveling between the City and the West End for meetings. Conversely, one respondent in a fringe location spoke of the intention to move to an office in the City in order to overcome the difficulty of traveling to clients there. In terms of travel to work patterns, being located to any degree North, South, East or West of the center was perceived to limit the geographic scope of where staff would travel from. To some extent this was more limiting at lower levels in the organization as the senior staff had the wherewithal to pick a more favorable residential area with a view to travel to work. Many respondents expressed their concern about the impact of vexing and lengthy commutes on their staff, sapping energy and enthusiasm. In addition to over-crowding and unreliability there were adverse comments on the sheer shabbiness of the underground, and concern was expressed regarding the safety of the electrical installations. As the following quotations illustrate, while the cost of housing in London was not seen as a key issue threatening the cluster, transportation difficulties were.

Within the "square mile" of the City there is less of an issue regarding transport, since people can walk to appointments. However, the problems of traversing the center of London, particularly East-West, were identified by many respondents as a key concern. The following quotation illustrates the nature of the concern, which turns on the unpredictability of travel and the cost in terms of wasted time and energy:

The major concern regarding international travel is access to airports, especially the City-Heathrow link and to a lesser extent the reliability of transport once the airport has been reached. One respondent based in Canary Wharf reported leaving three hours before a Heathrow flight, and clearly regarded this as being unreasonable. One respondent who expressed an opinion on whether the problems of international travel stopped people coming to London expressed doubt that it would. Nevertheless, there were references to meetings being delayed or cancelled because people arriving on international flights had difficulty getting from the airport to the meeting. One thing which to some extent overcomes the problems of getting, for example, from Heathrow to the center of London is that, once there, it is possible to efficiently arrange a series of meetings with firms in close proximity.

The poor state of the transport infrastructure is something which is perceived to create a negative impression of the City for international clients.

Considerable dismay was expressed by a number of respondents regarding the failure to develop a coherent policy to improve public transport in London. Anger was expressed by several at the attempts by the Mayor of London to cajole people into using cars less and public transport more when the public transport system was already inadequate. Furthermore, unfavorable comparisons were made between the public transport system in London and the systems in Paris and Frankfurt. Only Tokyo received a mention as being worse than London. One respondent who had worked 35 years in the City judged the decline in the standard of public transport over that period to have been "enormous". Another stated that he had abandoned the District Line after 30 years in favor of his car because of a continual decline in standards. A number of respondents made the point that they had to be located in the cluster and were therefore forced to put up with declining transport conditions but that others may have a choice. One banking respondent said that until the firm's confidence in transport infrastructure increased, no new business activities were being brought to London. The view of an auxiliary financial services respondent summarized a common perspective,

While transport was singled out as a key problem by almost all respondents, many also commented on regulation and legislation as being an even more serious potential threat to the London financial services cluster. A principal concern related to European legislation which, crudely stated, was seen as likely to lead to a leveling down of London particularly in relation to the erosion of flexibility, damaging the ability of firms in London to "get the job done". One respondent referred to the threat as, "death by a thousand cuts". Shedding light on questionnaire responses on the Eurozone, the UK's failure to adopt the Euro was not regarded as an issue but UK involvement in European policy and the promotion of a single market was seen as highly important. Another issue was the risk posed by "over-burdensome" and complex UK regulation leading to increasing amounts of working time having to be diverted in trying to keep abreast of requirements. One respondent described the nature of the problem thus:

On the other hand there was a clear recognition that effective regulation is essential to maintain the credibility of the financial services sector. The main message that came across was the need for balance. The following quotations illustrate regulatory concerns:

A current concern that was commented on frequently in the interviews was the vulnerability of London to terrorist attack. Some firms emphasized the importance of adequate contingency plans to cope with a major disaster. Nevertheless the concerns in themselves were not discussed as a serious threat to the cluster. The comment, "I think people have short memories with that sort of thing" summed up the general feeling. However, one respondent believed that, were a major attack on London to take place, this could provoke a movement out of London. A number of other issues were occasionally mentioned as being negative aspects of London, such as street crime, untidiness and restrictive City planning regulations however these disadvantages appeared to be second order. 3.7 DeclusteringIn addition to exploring the advantages and disadvantages of London clustering, the interview survey specifically addressed the factors that push firms to consider relocating part or all of their activity away from the cluster. In general, a location outside London in the South East or elsewhere in the UK was considered viable only for non-client facing staff. Firms involved in dealing felt that they still needed to be in the London cluster because these activities had been "much less dematerialized" than other types of activity. However, several firms sounded a note of caution about the extent to which even back office functions could be spun out from the City. Some back office functions are purely routine and these lend themselves to declustering. Many such activities have indeed already been relocated. Other back office functions are specialized and depend upon knowledge of City practices and knowledge of the client. These operations are not candidates for declustering. More fundamental perhaps than the front office/back office or client facing/nonclient facing distinctions is whether or not the particular activity if routinized or commoditized as opposed to being bespoke or complex. If business activity is commoditized or routine it is amenable to declustering. But even then, it is not straightforward:

Even when relocation made sense, it also made sense to maintain some presence in the center of the cluster. As one insurance respondent put it "The City still has the connotation of - good address, got to be there at the center". An auxiliary financial services respondent took the view, "Every firm worth its salt operates with headquarters here in the City". Some firms made the point that in order to get a substantial benefit in terms of lower costs they would now need to move quite some distance from London, probably outside the South East but as the following quotations illustrate finding a move which is truly cost-effective is not always easy:

Several firms expressed an opinion on whether the promotion of financial services clusters elsewhere in the UK would be viable. Most were skeptical, pointing to the business reasons for continued concentration in London. One firm stated that the City is made up of mini-clusters anyway, of insurers and lawyers for example. It would therefore be impossible to transplant the mini clusters and maintain their important juxtapositions. A range of other comments suggested the need for careful consideration of plans to establish any new clusters that are not in close proximity to existing concentration as illustrated by the following interview extracts:

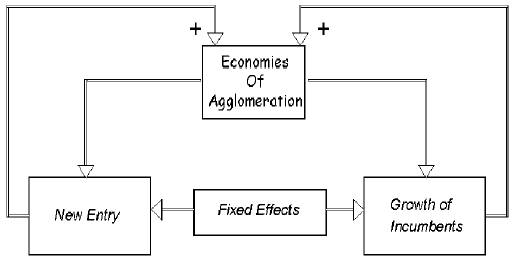

4 CONCLUSIONS AND POLICY RECOMMENDATIONSThe principal conclusion of this study is that London has a dynamic and successful financial services cluster which works in line with extant knowledge of the clustering phenomenon. Clustering continues to be important in spite of the costs associated with demand for a limited supply of highly centralized space. The market drivers and interdependencies associated with the geography of clustering in London are complex. This suggests that public policy to promote the benefits of the financial services concentration will be better directed at facilitating the operation of established clusters rather than master planning new clusters. Banks and to a lesser extent law and fund management are at the hub of the London cluster, therefore particular weight needs to be placed on the requirements of these sub-sectors as many others in the cluster depend on them. Access to the concentration of labor, customers and professional and government institutions is a critical advantage of proximity within the cluster. Maintaining London's attractiveness as a location for these activities should be a key policy priority. The labor market is of fundamental importance to the cluster, therefore making the labor market attractive and fluid is a top priority. The ability to walk to appointments in the City is seen as being highly important due to a combination of the need to establish and build trust, the need to meet face-to-face to thrash out complex problems quickly and the sheer convenience of being able to meet quickly without undue loss of time. Transport and regulation are the key policy areas where businesses see a threat to London and are urgent policy issues. In the following, conclusions and policy recommendations specific to the main themes of the paper are presented. 4.1 The Labor MarketThe scale and depth of the labor market is a crucial advantage. The attraction of London as a major metropolis and cultural center is important in drawing in labor, especially international labor, hence there is a premium on keeping London's amenity and reputation in these areas up to scratch for the good of its commercial success. The labor pool is embedded in the cluster and is the place where the knowledge and expertise which give London its supreme position in financial services reside. Being near a strong, skilled labor supply is particularly emphasized by key hub firms. A further advantage of the labor pool which draws firms to have operations in the cluster is the flexibility of the labor market by international standards. The policy implication is that a watch needs to be kept that this advantage of labor flexibility is not eroded by over burdensome regulation. The relevant labor market for many staff is heavily circumscribed by the choice of the firm's location and the feasibility of commuting there. This is an argument for a review of transport priorities as the labor market will function in a more integrated way if people can travel more easily across the city. This consideration also has implications for the provision of new housing in London and the South East (where most staff live) - where it is built will bear upon which parts of the city have easy access to the labor force that will be housed there. 4.2 Personal Relationships4.2.1 Face-to-Face Interaction Almost all the perceived advantages of being in the cluster turn on the fact that being physically close enables face-to-face contact and relationship building to take place. E-mail, telephone and video conferencing, while extensively used, are seen as complementing prior face-to-face interaction. Both formal and informal interaction is of great importance. It is notable that some respondents indicated that certain business might not take place at all if face-to-face contact were not possible. This is a powerful argument for keeping the cluster as compact as possible (possibly envisaged in terms of time and ease of travel rather than physical distance). 4.2.2 Knowledge Transfer Proximity within the cluster produces a density of interaction and information that promote knowledge transfer. This is important for the dynamism and the ability of firms in the cluster to serve clients in high value added complex activities. Notably it is particularly emphasized by banks which occupy a central place in the cluster. Such knowledge transfer is effected by a variety of mechanisms all of which are promoted by compact space. Examples include: formal and informal meetings, labor mobility and chance meetings. The policy implication again is that it is important to maintain as far as possible the geographic compactness of the cluster. In terms of transport policy it implies that it is important that plans to develop locations near the cluster eed to take into account ease of movement within the cluster. 4.2.3 Inter-firm Linkages There is clear evidence of close and important inter-firm linkages among local firms, particularly those with complementary expertise, which above-all translate into the ability to provide high level services to clients e.g., by the ability to form multidisciplinary teams which can work well together quickly. The ability to form inter-disciplinary teams is particularly important in respect of client meetings and again a particular advantage of location in the cluster. The policy implication is that it is very important that the cluster remains multifunctional and diverse. Proximity to the customer is highly important, perhaps more so than has been revealed in the existing clusters literature. This relates to major clients based themselves in or near the cluster, to firms who rely on other firms in the cluster for a derived demand for their services and also to the ease for international clients of doing business, perhaps with a range of firms based in the cluster. All three of these have the policy implication that it is important to maintain a compact cluster. It also has implications for transport policy. The convenience and efficiency of geographical propinquity are being undermined by problems of traversing the city. In terms of international clients there is the added issue of getting to London from airports. 4.3 Sources of Help with InnovationLocation appears to be most important in helping to develop new markets and better ways to deliver. The co-location of a pool of skilled labor and customers is an important stimulus to innovation. The link with innovation is particularly strong for banks. The implication for policy is that physical clustering of service firms and customers should be sustained and promoted to support innovation. 4.3.1 Institutional Thickness Many firms in London benefit from being close to a relevant exchange and/or other important institutions such as a regulator or trade association. The policy implication is that the benefits derived from this source would be weakened by dispersing the cluster. 4.3.2 Role of Local Government Banks more than other lines of activity find help from the local authority beneficial. This implies an opportunity for co-operative working between the banks and local government and it merits review whether ways can be found to reinforce this link. 4.4 InterdependenciesThe balance of co-operation and competition between sub-sectors is manifested in the cluster as in the classic clusters literature. Large firms and banks place particular importance on being near other leading competitors as a feature of being in the cluster which helps maintain their competitiveness. This finding has policy implications relating to the benefits of the cluster specifically as a hub-and-spoke spatial form (Markusen, 1996). 4.5 Disadvantages of a London Location4.5.1 Transport Transport has already been commented on under other headings. This is highlighted as an extremely important concern of business with clear evidence that it is acting as a drag on the efficiency of London and possibly beginning to deter visiting international clients. While not imminently threatening the cluster it appears to be a high policy priority to ease the problems identified, in particular travel to work, travel East-West across central London and travel between Heathrow (and other airports) and the London cluster. 4.5.2 Regulation Here the evidence was equivocal in so far as firms indicated that rigorous regulation was important in giving quality assurance to work done in London but many also expressed the view that regulation was becoming burdensome, indeed unmanageable. Regulation emerges as a particularly important concern for banks. The policy implication is that the regulatory burden needs to be reviewed and monitored in relation to rival financial centers. There is also a need for co-operation across agencies to ensure that contradictory effects on London's attractiveness as a place to do business are not created. 4.5.3 Cost of Premises While the most highly ranked disadvantage in the questionnaire survey, the interview evidence implies it is more an annoyance to firms than a fundamental threat to the viability of the cluster. It is not clear there is a policy recommendation here except to monitor property prices in relation to other financial centers. 4.6 De-clusteringIt appears that it is the more routine/low revenue types of work that are the ones being spun out of London (and, to some extent now, the South East) due to high space and labor costs. Accessibility for skilled staff is a key reason for an office location in the cluster together with the need to have a credible address. Policy will need to take account of the fact that these are decisive reasons for firms not moving high order office functions away from the cluster and in particular from the City. Movement of certain activities out of the cluster should not necessarily be seen as damaging to the cluster overall. The research suggests that locational centralizing and decentralizing movements of, for example, back-office activities, are part of an ongoing evolutionary process that is important to the global competitiveness of the cluster. While Canary Wharf has provided much needed additional space for expansion, planned high-rise development and provision of flexible space, in relation to functional use, size and age/cost of office accommodation in the City were deemed to be important to meet future anticipated needs for dense clustering. This research suggests that successful clustering can be facilitated or eroded by public policy. Government administrative and organizational boundaries, lack of policy co-ordination and focused management relating to regulation and transport were perceived by respondents to be a barrier to effective decision-making and investment. Co-ordination across policy and departmental as well geographical boundaries will therefore be essential to support sustainable financial services clustering in London. REFERENCESAgnes, P. 2000. The "end of geography" in financial services? Local Embeddedness and territorialization in the interest rate swaps industry. Economic Geography 76: 347-366. Audretsch, D. B. and Feldman, M. P. 1996. R&D spillovers and the geography of innovation. American Economic Review 86: 630-640. Baptista, R. M. L. N. and Swann, G. M. P. 1998. Do firms in clusters innovate more? Research Policy 27: 527-542. Beaudry, C., Cook, G. A. S., Pandit, N. R. and Swann, G. M. P. 1998. Industrial districts and localized technological knowledge: The dynamics of clustered SME networking. Research Report 3.3 (Clusters, growth and the age of firms; A study of three industries: Aerospace, Broadcasting and Financial Services) for the European Community DG XII. Best, M. 1990. The new competition. Massachusetts: Harvard University Press. Camagni, R. 1991. Local 'milieu', uncertainty and innovation networks: Towards a new dynamic theory of economic space. In Innovation networks: Spatial perspective, ed. R. Camagni. London: Belhaven. Capello, R. 1999. Spatial transfer of knowledge in high technology milieux: Learning versus collective learning processes. Regional Studies 33: 353-365. Cook, G. A. S., Pandit, N. R. and Swann, G. M. P. 2001. The dynamics of industrial clustering in British broadcasting. Information Economics and Policy 13: 351-375. Cook, G. A. S. and Pandit, N. R. 2002. Innovation, small firms and clustering: Insights from the British broadcasting industry. In New technology-based firms in the new millennium, Vol II. ed. R. P. Oakey et al. Oxford: Elsevier. Department of Trade and Industry 1998. Our competitive future: Building the knowledge driven economy, Cm 4176. London: HMSO. Gordon, I. R. and McCann, P. 2000. Industrial clusters, complexes, agglomeration and/or social networks? Urban Studies 37: 513-532. Henderson, J. V. 1986. Efficiency of resource usage and city size, Journal of Urban Economics 19: 47-70. Markusen, A. 1996. Sticky places in slippery space: A typology of industrial districts. Economic Geography 72: 293-313. Maskell, P. and Malmberg, A. 1999. Localized learning and industrial competitiveness. Cambridge Journal of Economics 23: 167-185. McCann, P., Arita, T. and Gordon, I. R. 2002. Industrial clusters, transactions costs and the determinants of MNE location behavior. International Business Review 11: 647-663. Pandit, N. R. and Cook, G. A. S. 2003. The benefits industrial clustering: Insights from the British financial services industry at three locations. Journal of Financial Services Marketing 7: 230-245. Pandit, N. R., Cook, G. A. S. and Swann, G. M. P. 2001. The dynamics of industrial clustering in British financial services. The Service Industries Journal 21: 33-61. Pandit, N. R., Cook, G. A. S. and Swann, G. M. P. 2002. A comparison of clustering dynamics in the British broadcasting and financial services industries. International Journal of the Economics of Business 9: 195-224. Piore, M. and Sabel, C. 1984. The second industrial divide: Possibilities for prosperity. New York: Basic Books. Porter, M. E. 1990. The competitive advantage of nations. London: Macmillan. Porter, M. E. 1998. Clusters and competition: New agendas for companies, governments, and institutions. In On competition ed. M. E. Porter. Massachusetts: HBS Press. Roberts J. et al. 2000. Knowledge and innovation in the new service economy. In Andersen, B., Howells, J., Hull, R., Miles, I. and Roberts, J. Knowledge and innovation in the new service economy. Cheltenham: Edward Elgar. Saxenian, A. 1994. Regional advantage: Culture and competition in Silicon Valley and Route 128. Massachusetts: Harvard University Press. Swann G. M. P., Prevezer M. and Stout, D. (eds.) 1998. The dynamics of industrial clustering: International comparisons in computing and biotechnology. Oxford: Oxford University Press. von Hippel, E. 1988. The sources of innovation. Oxford: Oxford University Press. Wrigley, N., Currah, A. and Wood, S. 2003. Investment bank analysts and knowledge in economic geography. Environment and Planning A 35: 381-387. NOTES^ This research was partly funded by the UK Economic and Social Research Council and partly funded by the Corporation of London. We would like to thank all our interviewees and to acknowledge input from Malcolm Cooper, Helen Greenwood, Peter Hall, Michael Hoyler, Robert Kloosterman, Nick Owen, Kathy Pain and David Walker. Thanks also to the participants of the 9th annual High Technology Small Firms Conference (Manchester Business School, UK, May-June, 2001), the 9th Biennial International J. A. Schumpeter Society Congress (Florida, USA, 28-30 March 2002), the Special One-Day Clusters Conference (Manchester Business School, UK, 18 April 2002), the 1st Business Innovation in the Knowledge Economy Conference (IBM Warwick, UK, 12 June, 2002), the Uddevalla Symposium on Entrepreneurship, Spatial Industrial Clusters and Inter-Firm Networks (Uddevalla, Sweden, 12 -14 June 2003) and the 30th European Association for Research in Industrial Economics (EARIE) Annual Conference (Helsinki, Finland, 24-26 September 2003). None of these are responsible for any remaining errors. * Business School, Loughborough University, UK ** Manchester Business School, Manchester University, UK. Corresponding author. n.pandit@mbs.ac.uk *** Department of Geography, Loughborough University, UK **** Institute of Community Studies, London, UK 1. The number of responses to many questions does not add up to 310 (the total number of questionnaires returned), for the simple reason that some respondents did not answer every question. 2. In the questionnaire, each firm was allowed to rank up to three lines of activity in order of importance. The analysis of the influence of line of activity is based only on number 1 rankings (see the figures in the boxes in question 1 in Appendix 2). There were very few overlaps between the largest categories with, for example, very few banks indicating they also had insurance operations and vice versa. Appendix 1: An Overview of the Theoretical Basis of the Survey Designs Cluster theory maintains that a firm may be attracted to a cluster because of "fixed effects" (Swann et al., 1998). These are benefits that exist at a location that are not a function of the copresence of related firms and institutions and include, for example, climate, time-zone and cultural capital. These lead to cluster growth - new firms are formed and incumbent firms grow. Beyond fixed effects, there are benefits that are directly related the co-presence that exists within a cluster and these can be referred to as economies of agglomeration. These lead to further cluster growth and can be dynamic in that they increase as agglomeration increases. Hence the feedback loops in Figure A1. Figure A1: Cluster Dynamics

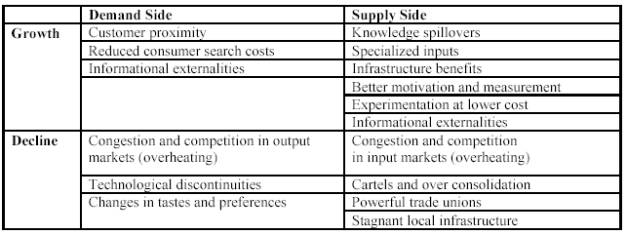

From the perspective of the clustered company, cluster benefits can emanate on the demand or supply side. Also, costs associated with clustering can emanate on the demand or supply side. Generally, when benefits are greater than costs, the cluster grows (incumbent companies grow and new companies are formed); when costs are greater than the benefits, a cluster declines (Table A1). Table A1: Cluster Growth and Decline Factors

Cluster benefits on the demand side include customer proximity. The idea is that the company may reduce transactions costs by locating close to its customers. However, benefits may go beyond cost. Sophisticated buyers are more likely to exist in a cluster and these can encourage innovation by being demanding and by alerting suppliers of new trends and innovations (von Hippel, 1988). Such knowledge exchange between customers and suppliers can be problematic because the value of knowledge is difficult for users to gauge before they have acquired or absorbed it. Accordingly, it is difficult for a market for the exchange of knowledge to arise (Roberts et al., 2000). Clusters allow for the development of reputation and of networks of trust between the parties involved and so provide a solution to this problem. The clustered company may also benefit from reduced consumer search costs. The idea here is that the firm is more likely to be found by customers when it is located in a cluster. This is particularly important when consumers have specific requirements (and so explains why antique shops tend to cluster). Information externalities on the demand side may also exist, that is, a clusters reputation rubs off on the company that is located in it. On the supply side a major benefit is that knowledge spills over in strong clusters and this is particularly important when valuable industry knowledge is tacit and informally communicated (Howells, 2002). The effective spilling of tacit knowledge can lead to more prolific innovation. A second supply side benefit is access to specialized inputs. As a result, the company benefits from lower search costs because it can easily recruit from a pool of specialized labor and can tap into a specialized supplier base. Infrastructure benefits can go beyond access to a good transport network to include institutions that coordinate activities across companies in order to maximize collective productivity, for example, trade associations which set standards and/or conduct marketing for the cluster as a whole (Porter, 1990). Better motivation and measurement can also exist within a cluster as local rivalry can act as a powerful spur (Porter, 1998). Also, it can be easier to measure performance against local rivals as they share a similar context leading to lower monitoring costs. Another important supply side benefit is that it can be easier to try out new ideas in a cluster since it is possible to gain instant feedback and all of the inputs (including sympathetic venture capital) required for experimentation are likely to be present in the cluster. Finally, a clustered company may benefit from informational externalities on the supply side: The firm enjoys lower risk by observing successful production at a location. Cluster costs on the demand side are as follows. Other things equal, as the number of competitors increases, we would expect prices and so profits to fall. Also, a cluster specialized in a particular technology can go into decline if that technology is substituted. Finally, changes in tastes and preferences can lead to cluster decline. On the supply side, congestion and competition in input markets can lead to higher wages and rents which in turn could lead to movement out of the center of a cluster. Cartels and over-consolidation, powerful trade unions and stagnant local infrastructure are all potential decline factors as they can restrain competition and innovation and slow down productivity improvements. These potential supply side decline factors provide an agenda for government industrial policy. Appendix 2: Postal Questionnaire Survey

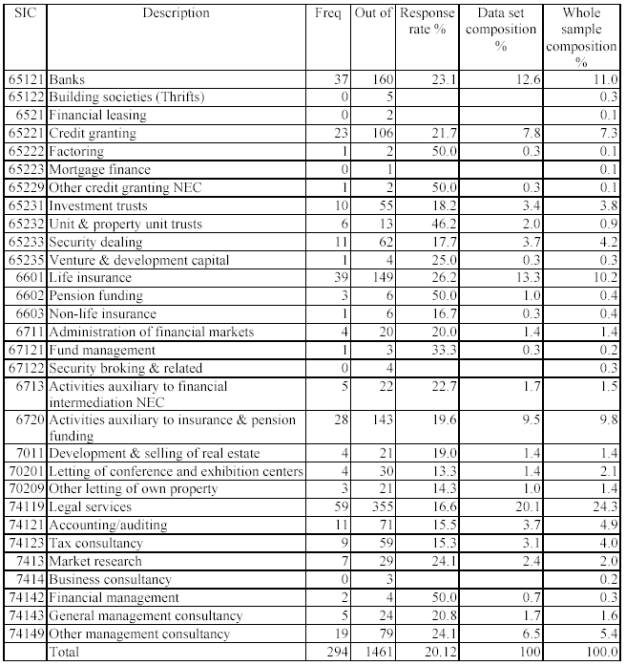

Table A2 shows the composition of the sample obtained, giving details for the 294 cases where it was possible to classify the case to a specific line of activity (a small number of questionnaires were returned anonymously and could not be assigned to a particular line of activity). What can be seen is that the 294 returns are distributed across the lines of activity in very much the same proportions as the 1,500 firms to whom the questionnaire was issued (the table shows slightly less than 1,500 firms because it was not possible in every case to identify the line of activity to which the firm should be classified). We are therefore confident that we have a random and representative sample from the population of interest. Table A2: Characteristics of the Questionnaire Sample

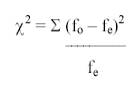

The extent to which firms in different lines of activity rated the various factors in the questionnaire differently was tested using a contingency table method. The method compares the actual number of cases appearing in each cell with the expected count. The ÷2 statistic tests whether the differences between observed and expected counts in each cell are significantly different to what one would expect. The precise formula is given by:

Where fo if the actual count in each cell and fe is the expected count. A rule of thumb with contingency tables is that no more than 20% of all cells should have an expected count less than 5. In order to achieve this, categories are sometimes aggregated. The The second major means of analysis was to compare outcomes using tests based on comparison of the median. Here the responses to each question were compared by size of employment. The basis of the test is to rank all cases by size from smallest (given a rank of 1) to the largest. The sum of the ranks is calculated for each category of response and divided by the number of cases to compute the mean rank. Where there is no difference between the categories in terms of size, the mean ranks will be the same. The appropriate test statistic, the Kruskal-Wallis, was computed and again where the calculated statistic exceeds some critical value we reject the working hypothesis that firms giving each category of response had the same median size. Appendix 3: Interview Schedule1a) Why did your firm originally choose this London office location? 1b)What are the current advantages of this location for your line of business / which of these advantages are specifically associated with proximity to the City's critical mass? 2a) What is the nature of your relationships with other firms and institutions in the City (City Fringe) / what are the benefits of these relationships for innovation and competitiveness in your business? 2b) How do you communicate with nearby firms/ how important is close proximity and face-to-face contact? 3a) What is the nature of your business relationships elsewhere in London, the South-East, UK, Europe and globally / is there a functional or geographical 'City Fringe'? 3b) How do you communicate with people and firms located at a distance / how important is travel and face-to-face contact? 4a) What is the nature of your labor market - within London, the South-East, the UK, globally? 4b) In what ways, if any, are living and travel to work patterns changing in your business / what are the implications for the cluster? 5a) Has your firm recently considered moving to a different location, if so where? 5b) What factors are likely to enhance or threaten business concentration in the City / what action is required and by whom? 6a) Finally, what do you see as the benefits of business concentration in the cluster for London, the South-East, UK, Europe and other parts of the world? 6b) What could be done to enhance these benefits? Positions of Personnel InterviewedCompany specific titles of individual interviewees are withheld for confidentiality. More than one individual was interviewed within some organizations. Chairman